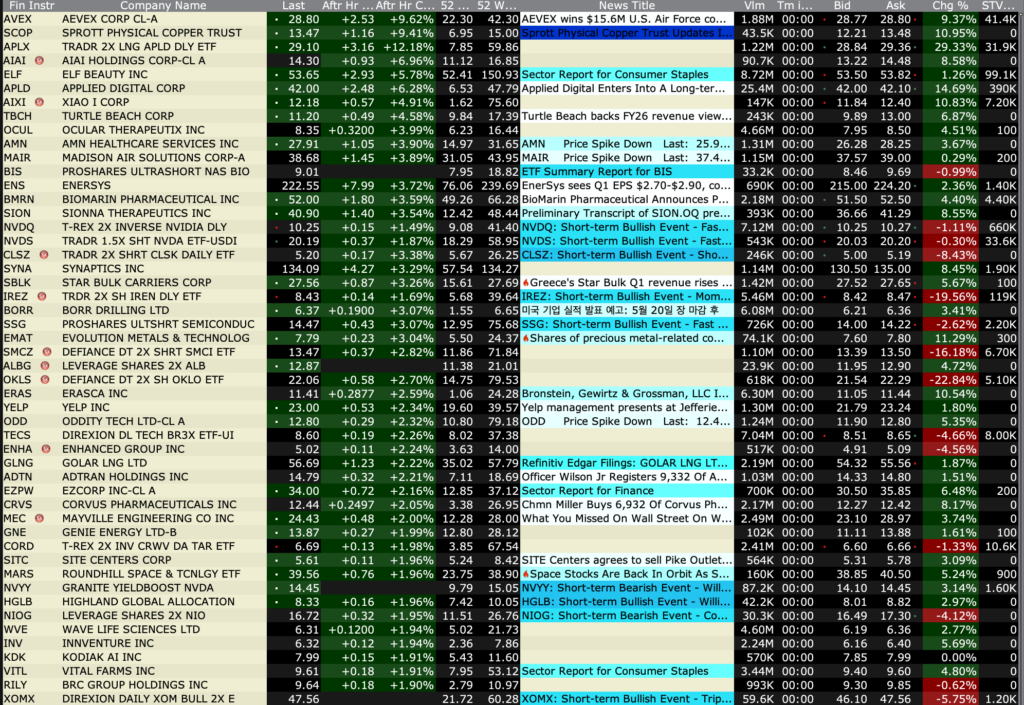

Wednesday’s After-Hours Advancers and Decliners

As of 4:23 PM:

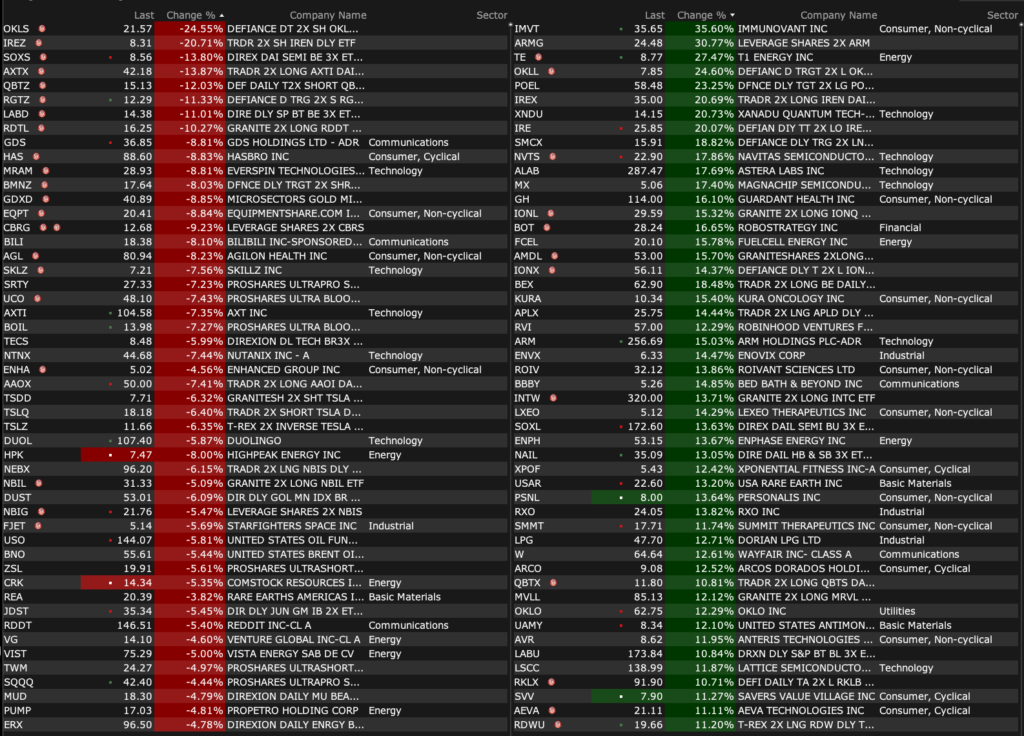

After-Hours % Advancers

After-Hours % Decliners

Position: None

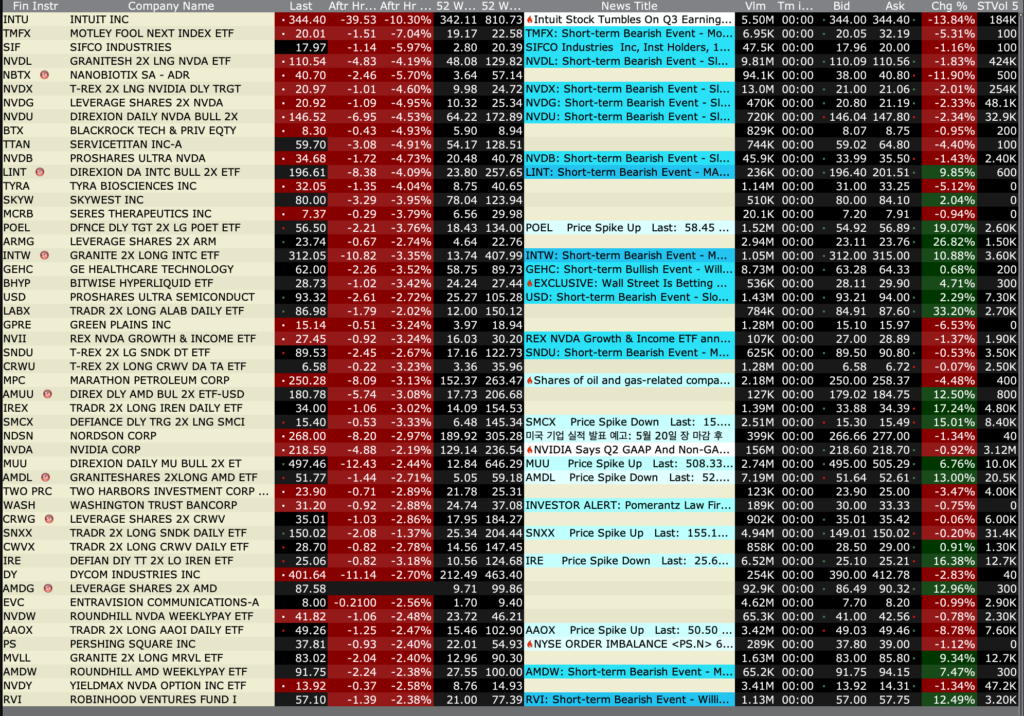

BY Doug Kass · May 20, 2026, 4:52 PM EDT

As of 4:23 PM:

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · May 20, 2026, 4:52 PM EDT

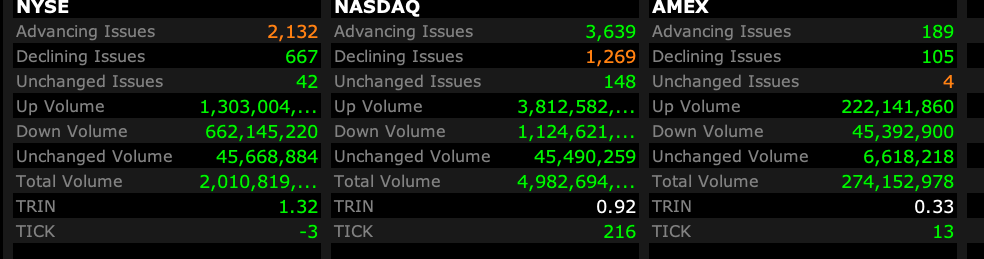

Closing Volume

– NYSE volume 3% above its one-month average

– NASDAQ volume 4% above its one-month average

– VIX index: down 3.82% to 17.37

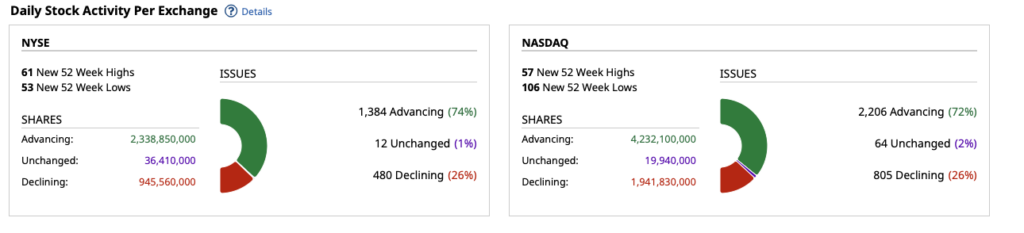

Breadth

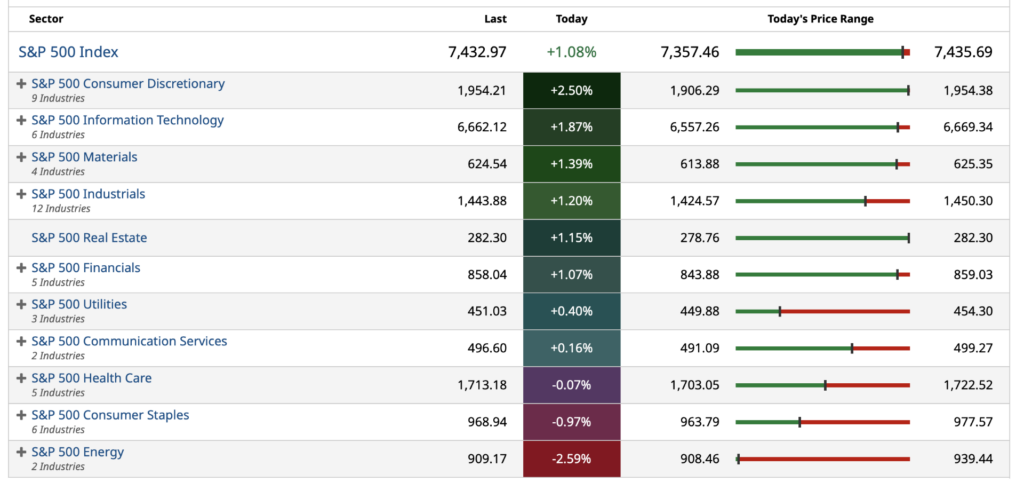

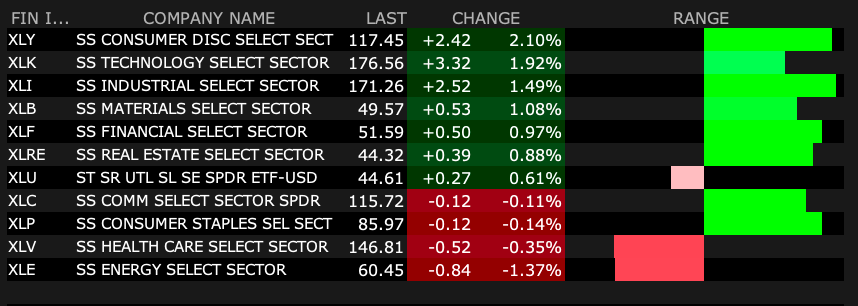

S&P 500 Sectors

% Movers

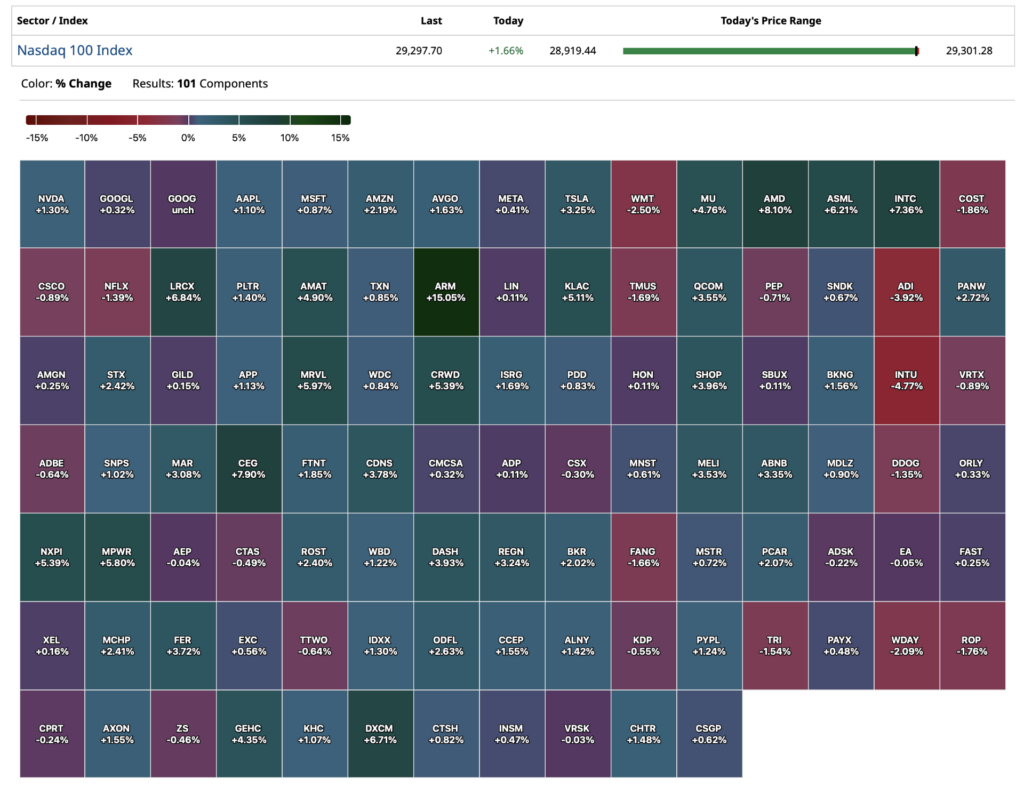

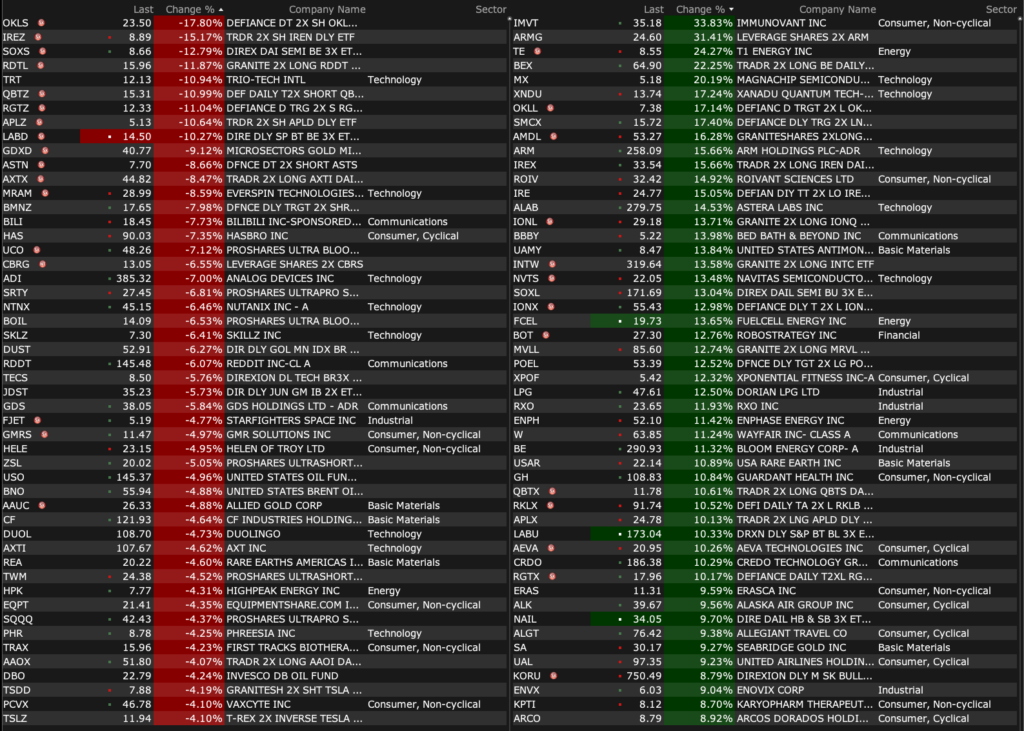

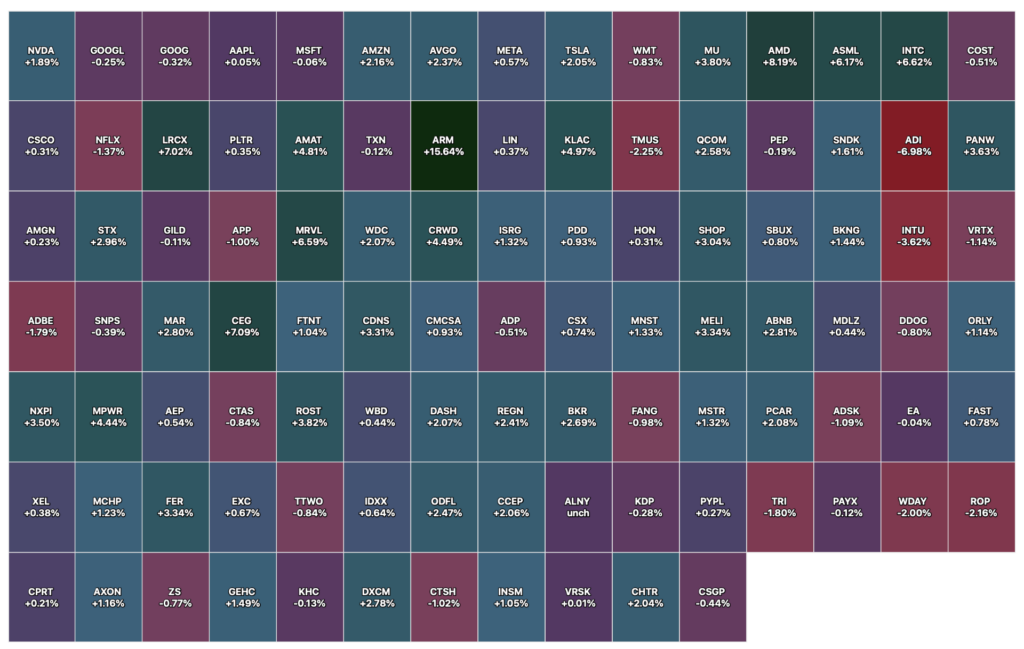

Nasdaq 100 Heat Map

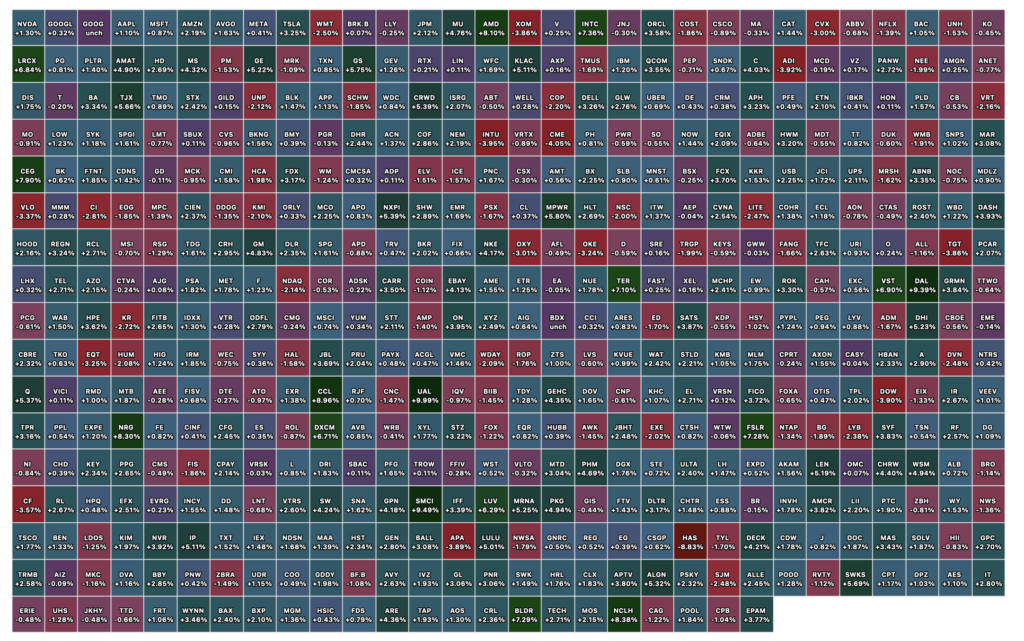

Closing S&P 500 Heat Map

Position: None

BY Doug Kass · May 20, 2026, 4:44 PM EDT

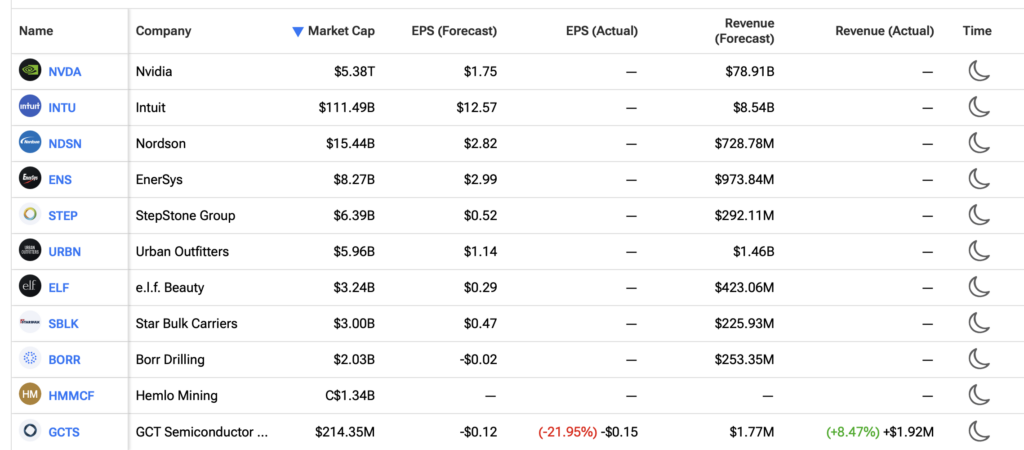

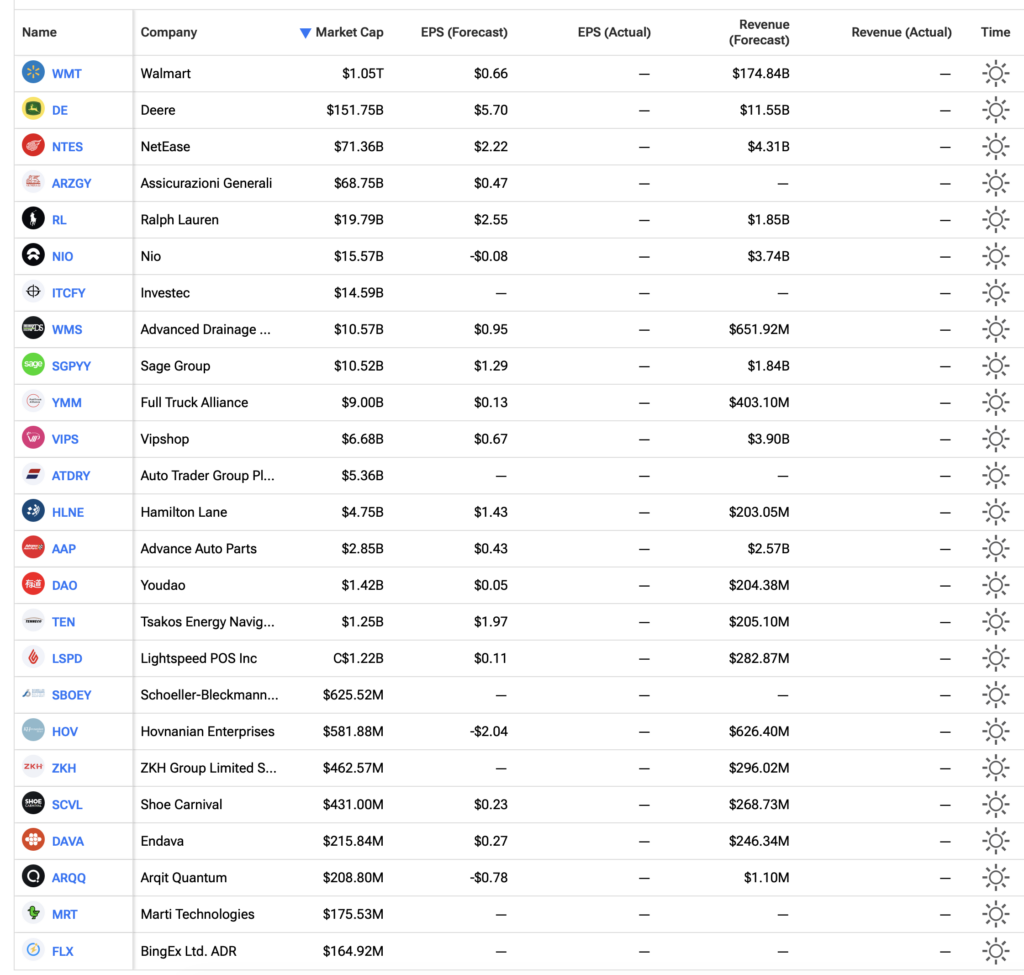

Earnings Reporters After Close Wednesday

Earnings Reporters Before Open Thursday

Position: None

BY Doug Kass · May 20, 2026, 1:58 PM EDT

Position: Short JOET (VS)

BY Doug Kass · May 20, 2026, 12:47 PM EDT

BY Doug Kass · May 20, 2026, 12:29 PM EDT

Volume

– NYSE volume flat to its one-month average

– NASDAQ volume 12% above its one-month average;

– VIX index: down 2.27% to 17.65

Breadth

S&P 500 Sector ETFs

% Movers

Nasdaq 100 Heat Map

Position: None

BY Doug Kass · May 20, 2026, 12:15 PM EDT

From Gary Marcus:

Position: None

BY Doug Kass · May 20, 2026, 11:50 AM EDT

I have taken a short trading rental in (MS) at $195.76.

Position: Short MS VS

BY Doug Kass · May 20, 2026, 11:10 AM EDT

With S&P cash + 58 handles I am expanding my index shorts (but I still remain VS):

* (SPY) $739.43

* (QQQ) $710.07

Positions: Short SPY VS QQQ VS

BY Doug Kass · May 20, 2026, 11:05 AM EDT

From Peter Boockvar:

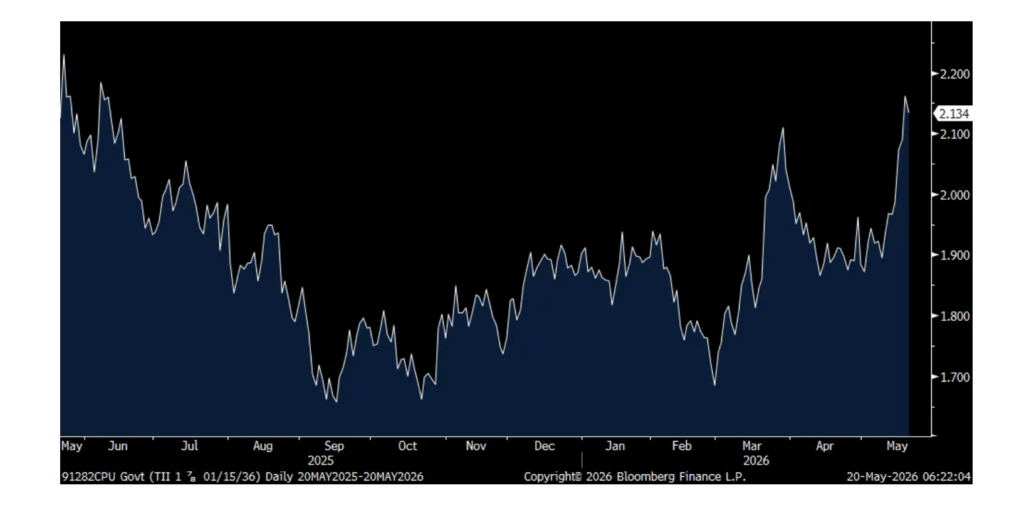

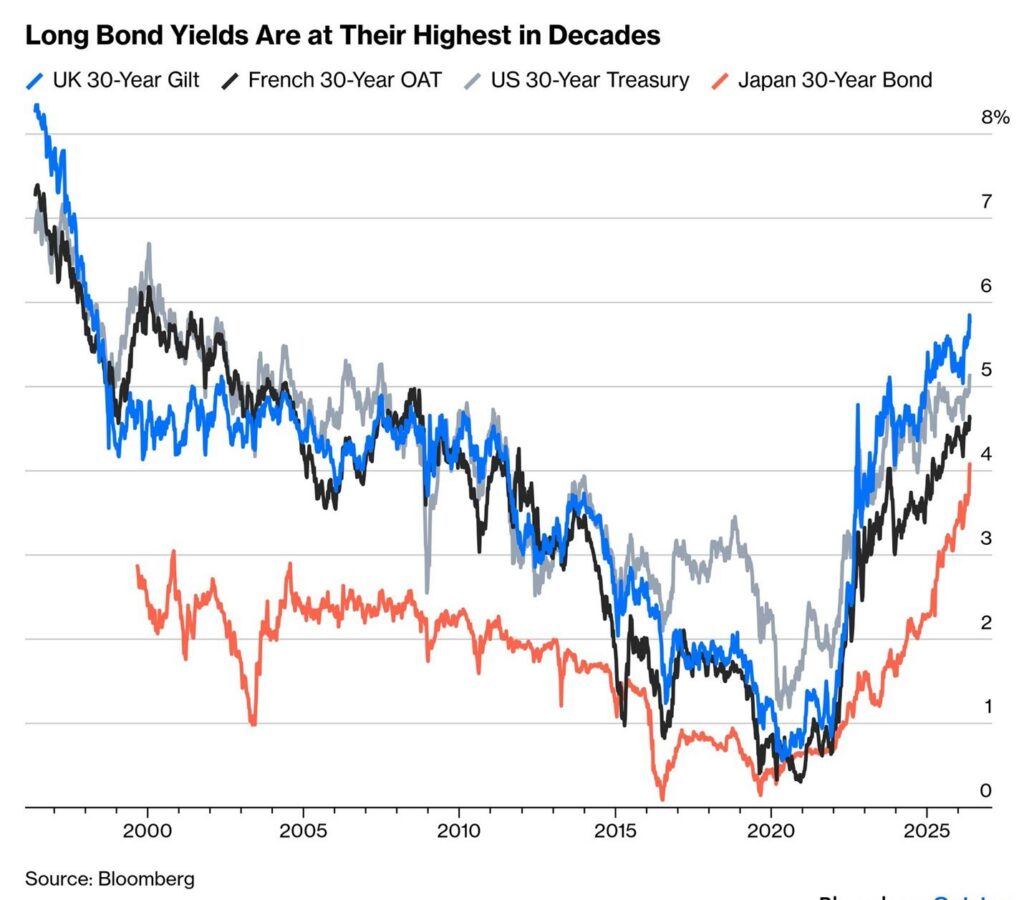

There is a common belief that the only reason why bond yields are rising is because of growing inflation worries. While that is true in part for sure, the big jump in REAL yields over the past few weeks says that it is something more. The 10 yr REAL rate is up 25 bps just over the past week and a half and I’ll argue again that global debts and deficits now matter in the eyes of lenders. Also, those bond markets like in the UK, Germany, France and the US that have large foreign ownership have been a source of funds for those countries that need to bring money home to help with rising energy imports and the subsidization that’s taking place for consumers. With Japan as the BoJ and domestic savings have mostly financed its deficits, it’s more excessive financing worries and the lack of BoJ rate hikes that plague that market where the long end of their curve is tightening policy for the BoJ.

REAL 10 yr yield

Inflation of course is still a big concern and FreightWaves reminded us of that yesterday by saying that truck spot rates reached $3.55 per mile and now approaching the record high of $3.68. Capacity that continues to leave the market is the main factor and that’s happening for a variety of reasons, including the recent crackdown on safety with respect to ridding the market of non-domiciled commercial drivers license’s, the recent SCOTUS 9-0 decision that puts safety legal liability on freight brokers and the freight recession that is now about 3 years.

On to some important earnings calls.

From Home Depot:

“In the US, our Northern and Western divisions had positive comps, as customers engaged in outdoor projects when weather was favorable In local currency, Mexico had positive comps, while Canada was negative.”

“Big ticket comp transactions, or those over $1,000, were positive .8% compared to the first quarter of last year. We were pleased with the performance we saw in portable power and patio; however, larger discretionary projects remained under pressure.”

“During the first quarter, Pro posted positive comps and outperformed DIY.”

“And you look at our core customer, they’re probably amongst the healthiest of all consumers, so they tend to own their homes, they did have that 50% value pop in the value of their homes over the past several years. And their portfolios in equities have also improved. So our customer seems to be in reasonably good shape…And again, the main thing is just this uncertainty that’s holding them back from taking on large projects. And then you add to that, with higher rates housing turnovers remain low.”

Cava is bouncing pre market and they said this on their call:

“Despite today’s broader macroeconomic environment and geopolitical uncertainty, we sustained strong momentum and delivered exceptional results, including positive traffic of 6.8%.”

“While many peers have responded to short-term cyclical pressures with discounting and promotional activity, we have remained unwavering on our long term strategy.” In January they “took an approximate 1.4% price increase, holding base bowl and pita pricing flat. Over the longer-term, we have priced well below inflation, with price adjustments representing only slightly more than half of cumulative CPI since the end of 2019.” That value of course is what customers are looking for.

But the consumer is still circumspect with their spend as we know. This was from Chewy yesterday that was speaking at a JPMorgan conference:

“so while pet remains resilient, it is not immune to the macro changes that we are seeing. In the last couple of months, we are continuing to see and interpret the consumer as being more stretched than we were when we entered the year. There’s no shortage of data points that supports that.”

Target beat comp estimates and said in its release “First quarter financial results were stronger than expected, providing encouraging early signs that our clarified strategy is resonating with our guests and driving broad based growth across our business.”

Amer Sports, the owner of Arc’teryx, Salomon, Wilson, and Louisville Slugger among others, was up 2% yesterday and said this on their quarter:

“All segments, geographies, and channels performed extremely well in the quarter, led by exceptional Salomon softgoods growth, a strong Arc’teryx omni-comp, and solid Wilson Tennis 360 growth.”

Red Robin Gourmet Burgers is rising pre-market after better than expected numbers and had a similar strategy to Cava. From them of note:

“Our Big Yummm value platform continues to resonate with guests with high satisfaction scores and we’re seeing strong results across the system.” That program by the way, according to Gemini, is “a full meal – an entree, bottomless side (unlimited refills on fries, side salads or steamed broccoli), and a bottomless beverage (free refills) – starting at just $9.99.”

“The current economic environment requires that we remain deliberate in highlighting value and discipline in our approach to average check. Q1 was our third consecutive quarter where our check average increases were below the industry. Our prudent approach to menu pricing, complemented by the expansion of our Big Yummm platform, has positioned us for success and is reflected in our traffic momentum.”

That upper income consumer helped Toll Brothers with its quarter and its stock is rising pre-market. From their earnings release ahead of today’s call:

“Our strong results continue to reflect our unique position as the nation’s leading builder of luxury homes, with operations spanning more than 60 markets across the country. The strength of our brand, broad geographic footprint, and wide variety of home offerings and price points, combined with our long history serving the luxury market and its affluent customers, continues to set us apart.” I bolded to emphasize.

In the housing market, James Hardie also reported last night, the maker of building products for new homes and remodeling, particularly its decking product that replaces wood. From them:

“We delivered a solid fiscal fourth quarter and full year, despite a challenging construction market, the result of staying focused on what we can control: execution, cost, and serving our customers.”

“Demand held up across our core categories, despite weather related softness early in the quarter in the United States.”

The macro though is still tough. “The market has shifted substantially in the last few months. At the start of the year, we planned for broadly flat market demand in fiscal 2027. Since then, key variables have changed. 30 yr mortgage rates, below 6% late February, moved meaningfully higher after the Middle East escalation. Builder confidence and consumer sentiment have softened. Across our dealers and contractors, nearly half cite economic uncertainty as their biggest challenge.”

“New construction will remain under pressure. R&R activity (renovation/remodel) is compressed. Our base case assumes the addressable market declines approximately 3% in fiscal 2027.”

With respect to housing activity, according to the MBA, purchase applications to buy a home fell 4.1% w/o/w after rising by 3.9% last week as the average 30 yr mortgage rate jumped by 10 bps to 6.56%. Refi’s though were flattish.

On the commercial construction side, the April US Architecture Billings Index fell to 48.3 from 49.8 and thus remaining below the breakeven of 50. Commercial/industrial fell back under 50 while institutional (could be schools, government buildings and healthcare facilities, among others) and multi family are above. The ‘mixed practice’ category is the weakest at 42.5. That is those with a diversified client base.

The AIA chief economist said this on their survey, “April’s economic picture was mixed as employers continued to add jobs, but inflation accelerated as higher energy prices tied to the conflict in Iran drove up costs.”

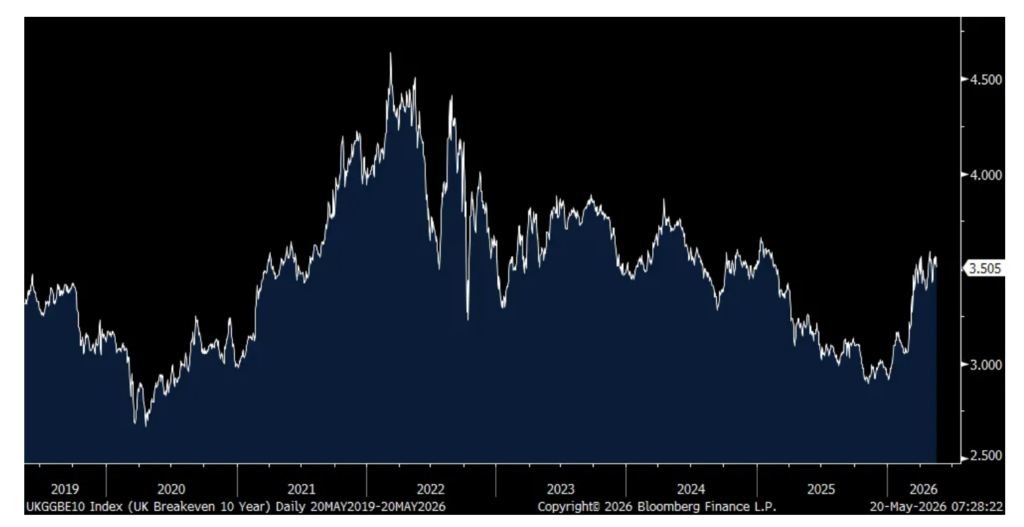

The key data point overseas was the April UK CPI which rose 2.8% y/o/y as expected and the same pace seen in March. Helping from making this worse were energy bill subsidies. The core rate was up by 2.5% y/o/y, one tenth below the forecast and why gilt yields are falling with the 10 yr yield down by 9 bps in response. Services inflation in particular slowed to 3.2% from 4.5% and was 3 tenths below expectations. The 10 yr inflation breakeven is falling by almost 4 bps to 3.51%

Price pressures though are still building as PPI input prices jumped 2.4% m/o/m, well more than the estimate of up 1% and output PPI was higher by 1.4% m/o/m vs the estimate of 1% and March was revised up by 5 tenths to a gain of 1.4% also.

10 yr UK Inflation Breakeven

Positions: None.

BY Doug Kass · May 20, 2026, 10:54 AM EDT

11:00 a.m.: Treasury buyback announcement (liq support);

11:30 a.m.: Treasury hosts a $69B 17-Week Bill Auction;

1:00 p.m.: Treasury hosts a $16B 20-Year Bond Auction;

9:15 a.m.: Fed Board Governor Barr (Voter) speaks on “Consumer Financial Health Metrics” before the Financial Health Network (FHN) EMERGE Financial Health 2026 Conference, Atlanta, GA (Text available. No Q&A. No webcast)

BY Doug Kass · May 20, 2026, 10:44 AM EDT

There are reports from Middle East press sources (Saudi’s Al Hadath) that a new round of Iranian-U.S. negotiations will be held in Islamabad after the Haji Season (which ends May 30).

According to the sources, Pakistani officials are visiting Iran tomorrow to announce a final draft of a potential agreement.

Positions: None.

BY Doug Kass · May 20, 2026, 10:38 AM EDT

Equities ripping on reports that more negotiations with Iran have been scheduled.

Shorting more indexes into it.

Positions: None.

BY Doug Kass · May 20, 2026, 10:33 AM EDT

Adding meaningfully to cannabis holdings.

Long MSOS M and individual weed companies

BY Doug Kass · May 20, 2026, 10:01 AM EDT

Adding to index shorts with S&P cash +30 handles:

* SPY (SPY) $736.91

* QQQ (QQQ) $707.94

Positions: Short SPY VS QQQ VS

BY Doug Kass · May 20, 2026, 9:52 AM EDT

Evidence of a consumer-led slowdown appearing today in the share prices of Lowes (LOWE) (-$9), Home Depot (HD) (-$5), Walmart (WMT) (-$2) and Costco (COST) (-$11).

Positions: None.

BY Doug Kass · May 20, 2026, 9:50 AM EDT

I have to travel this afternoon for a business dinner.

I will be leaving at around 2 p.m. and I won’t be around for the Nvidia (NVDA) fireworks.

Positions: None.

BY Doug Kass · May 20, 2026, 9:46 AM EDT

-IMVT +23% (earnings, color)

-POET +15% (Marex Securities Products builds 6% stake in POET)

-TATT +14% (earnings, color)

-EGHT +12% (earnings, guidance)

-RRGB +10% (earnings, guidance)

-IBRX +8.3% (US FDA Accepts sBLA for ANKTIVA Plus BCG in BCG-Unresponsive Non-Muscle Invasive Bladder Cancer with Papillary Disease)

-CAVA +7.7% (earnings, guidance)

-AMC +5.1% (CEO Adam Aron bought 250K shares at $1.377/shr)

-MRVL +4.9% (multiple broker price target raises)

-STM +4.5% (Euro semi name strength)

-LPG +3.9% (earnings, color)

-MU +3.9% (momentum amid potential memory chip shortage)

-TJX +3.8% (earnings, guidance)

-VFC +3.4% (earnings, guidance)

-PSNL +3.3% (Centers for Medicare & Medicaid Services’ (CMS) Molecular Diagnostic Services Program (MolDX) has expanded coverage for the company’s NeXT Personal minimal residual disease (MRD) test)

-TOL +3.3% (earnings, guidance)

-ASML +2.9% (Euro semi name strength)

-SNDK +2.4% (memory stock strength with rising memory price concerns)

-DMAC +2.3% (announces 75% Enrollment Milestone in ReMEDy2 Phase 2/3 Acute Ischemic Stroke Trial)

-VIAV -8.7% (prices 11.1M shares at $45.00/shr)

-NWL -2.6% (Morgan Stanley Cuts NWL to Underweight from Equal Weight, price target: $3.50)

-HAS -2.2% (earnings, guidance)

-LOW -2.1% (earnings, guidance)

Positions: None.

BY Doug Kass · May 20, 2026, 9:07 AM EDT

Positions: None.

BY Doug Kass · May 20, 2026, 8:38 AM EDT

Position: None.

BY Doug Kass · May 20, 2026, 8:18 AM EDT

Position: None

BY Doug Kass · May 20, 2026, 8:00 AM EDT

Position: None

BY Doug Kass · May 20, 2026, 7:35 AM EDT

What many market participants are missing is that the non-AI economy is faring poorly as growth decelerates.

Should the rate of growth in AI capital spending moderate… Katie Bar the Doors.

Slugflation (sluggish growth and persistently high inflation) is here and is not market friendly.

Position: None

BY Doug Kass · May 20, 2026, 7:15 AM EDT

Position: None

BY Doug Kass · May 20, 2026, 7:05 AM EDT

“The AI Boom will become a story of one of the largest destructions of shareholder value in history.”

– Financial Times

Position: None

BY Doug Kass · May 20, 2026, 6:55 AM EDT

Position: None

BY Doug Kass · May 20, 2026, 6:45 AM EDT

Position: None

BY Doug Kass · May 20, 2026, 6:35 AM EDT

Position: None

BY Doug Kass · May 20, 2026, 6:25 AM EDT

Position: None

BY Doug Kass · May 20, 2026, 6:15 AM EDT

Wolf Street howls about a trifecta of headwinds.

Position: None

BY Doug Kass · May 20, 2026, 6:05 AM EDT

With S&P Futures +24 handles and the Nasdaq futures +196 handles, I have added to my very small index shorts:

* SPY $736.12

* QQQ $706.38

Position: Short SPY (VS), QQQ (VS)

BY Doug Kass · May 20, 2026, 5:55 AM EDT

The S&P Short Range Oscillator is back into oversold at -2.08% vs. 0.04%.

Position: Short SPY (VS), QQQ (VS)

BY Doug Kass · May 20, 2026, 5:45 AM EDT

The consensus of analysts is that AI capital investments will rise by 20% a year for five years while revenues are expected to grow 15% resulting in negative returns. "The AI boom will become a story of one of the largest destructions of shareholder value in history."

How expensive is the S&P 500 right now? Four ways to count. - Price/Sales: 3.5x (all-time high, higher than 2000) - Price/Book: 5.5x (all-time high) - Forward P/E: 26x (at the 2000 dotcom peak) - Dividend Yield: 1% (near a record low) Three of these are at levels last seen at Show more

⚠️THIS IS ABSOLUTELY INSANE: ~24% of the S&P 500's top 100 stocks now have an inverted 3-month call skew, approaching the 25% peak seen during the 2021 meme stock frenzy. An inverted call skew occurs when out-of-the-money call options are more expensive than at-the-money Show more

Today I learned on @HalftimeReport that valuations no longer matter. CAPE, Buffett Indicator, Price to Sales... fuhgetaboutit! The absence of discourse, debate and dissension is deafening. The bullish herd of "first level thinkers" and consensus views are growing ever moreShow more

BREAKING: Japan's 10Y Government Bond Yield surges above 2.80% for the first time in history. This truly is one of the most insane charts ever seen.

Bond markets are flashing red. Today, the US 30Y Note Yield officially hit its highest level since July 2007, at 5.19%. This will soon become Americans’ biggest problem, yet the vast majority do not even know it is happening. What is happening? Let us explain. (a thread)

S&P 500 dumps from May to October every midterm election year: 1962: -22.16% 1966: -21.22% 1970: -0.15% 1974: -33.11% 1978: -7.91% 1982: +16.86% 1986: -8.14% 1990: -19.57% 1994: -2.05% 1998: -17.66% 2002: -31.34% 2006: -4.64% 2010: -6.03% 2014: -4.89% 2018: -5.15% 2022: -18.9% Show more

🚨 This is very, very bad Last time, this divergence appeared in early 2022 Following it, SPX dropped 28.7%

The embedded tweet could not be found…

PIMCO: Hyperscaler spreads over Treasuries have widened, and they’ve widened compared to other investment grade companies as well. While they were about 15% cheaper in early 2025, they’re now 25% more expensive, showing the market is pricing in more risk. Here’s a look at Show more