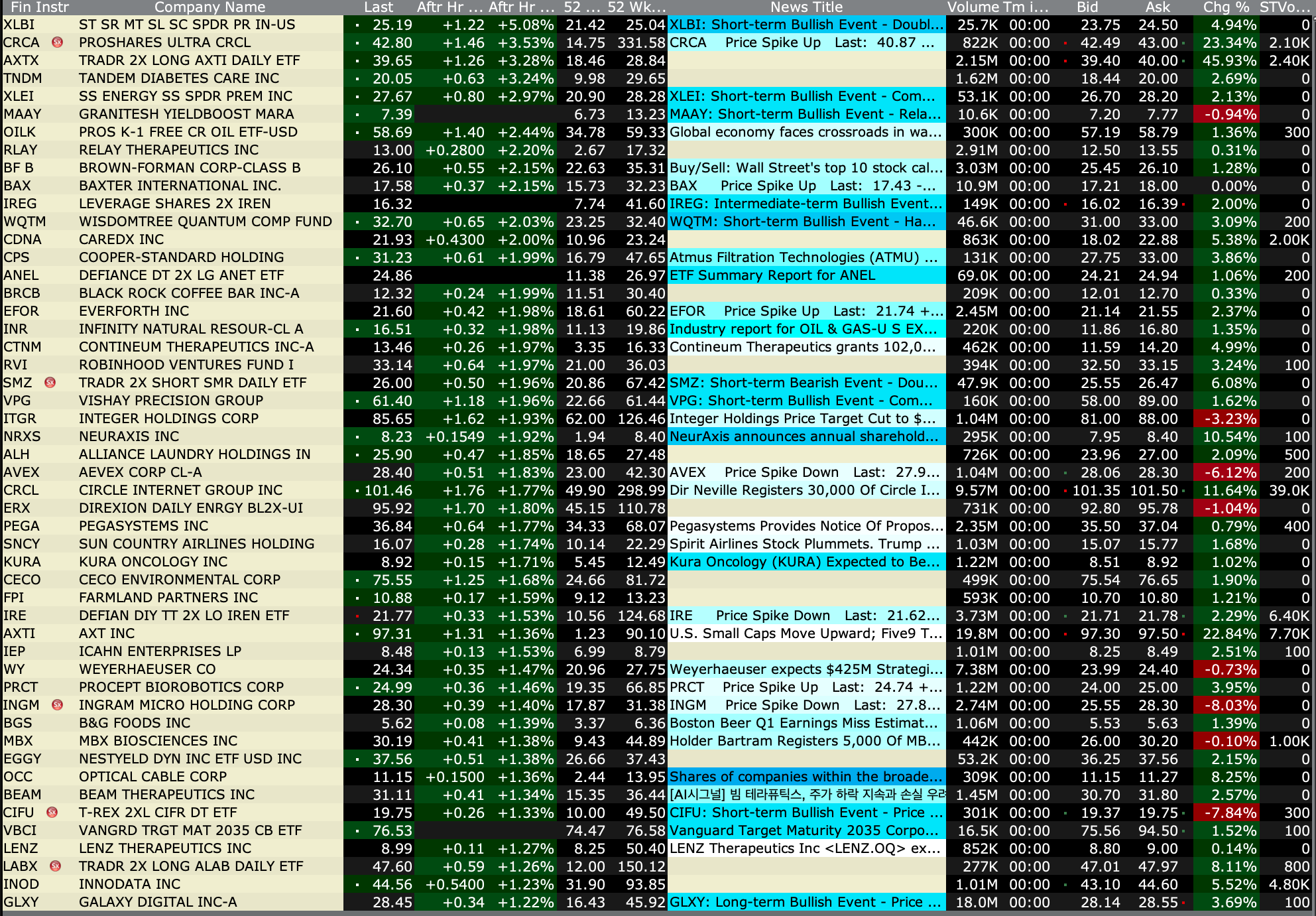

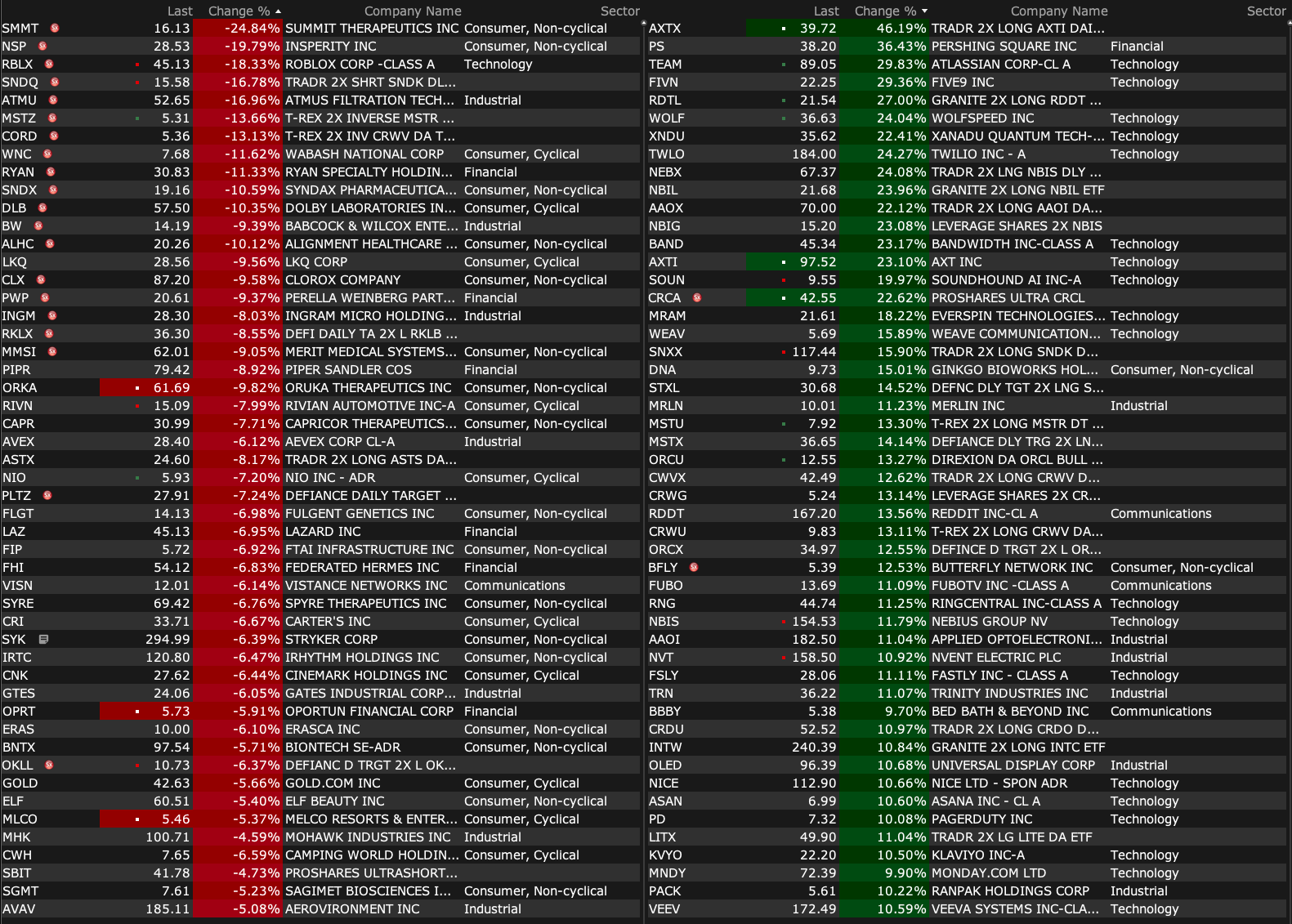

Friday's After-Hours Advancers and Decliners

After-Hours % Advancers

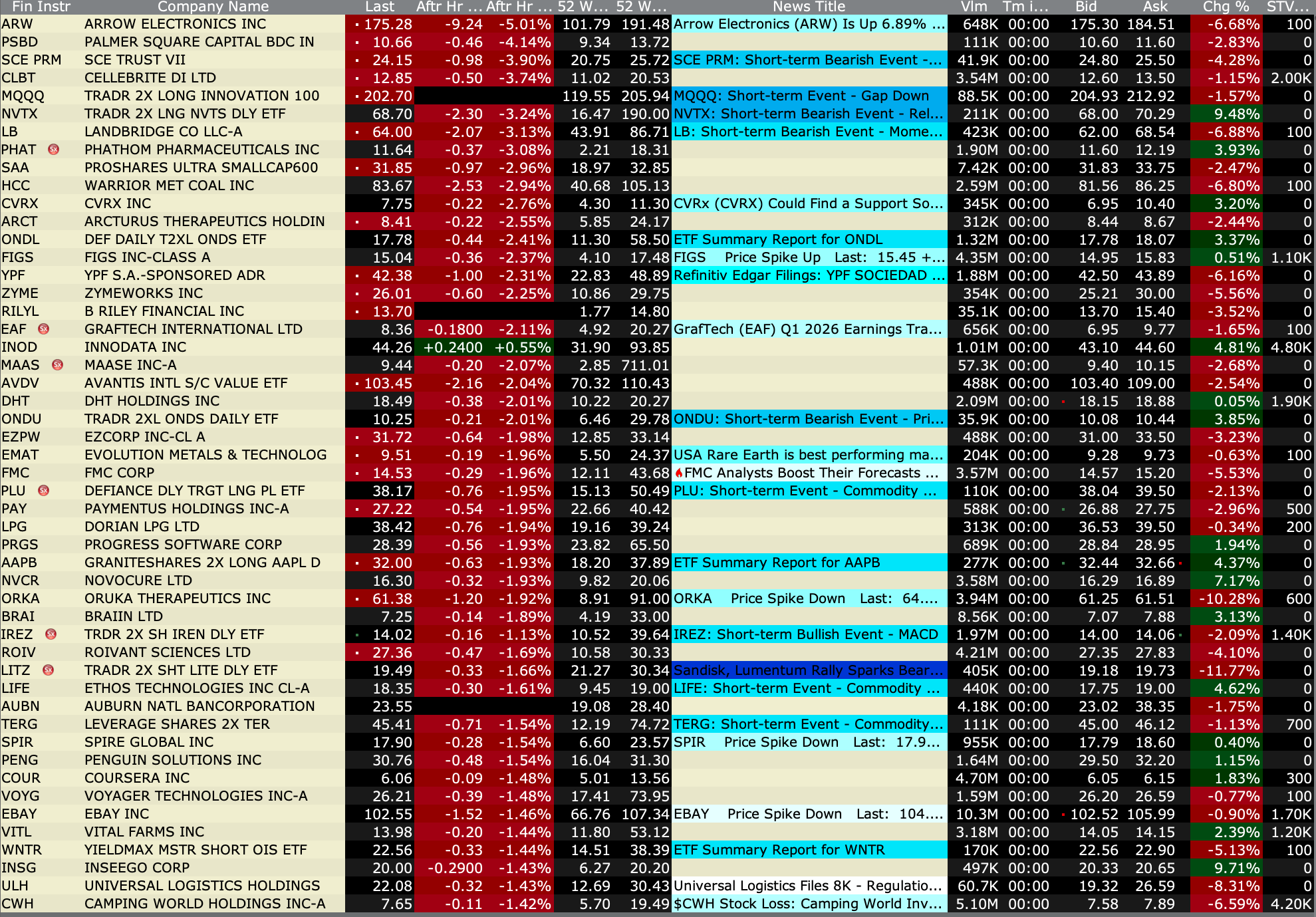

After-Hours % Decliners

BY Doug Kass · May 1, 2026, 4:45 PM EDT

After-Hours % Advancers

After-Hours % Decliners

BY Doug Kass · May 1, 2026, 4:45 PM EDT

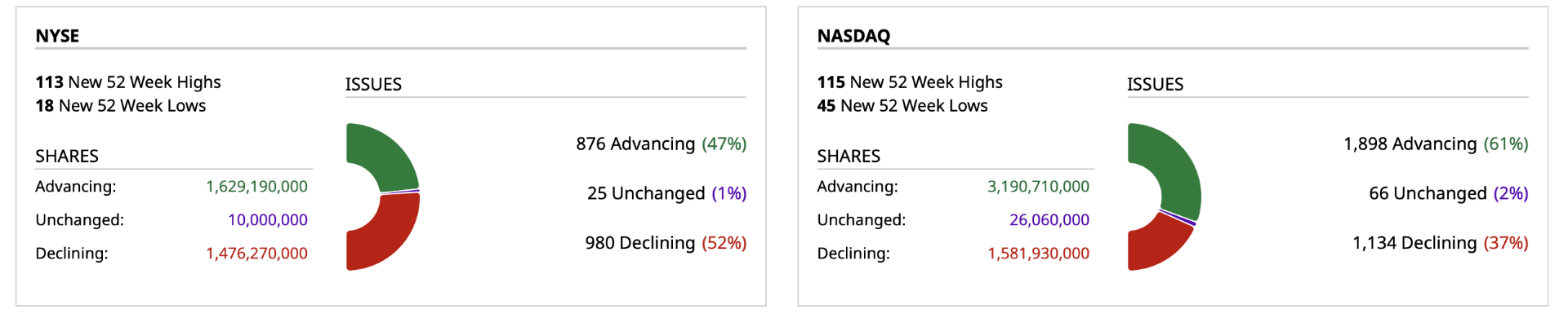

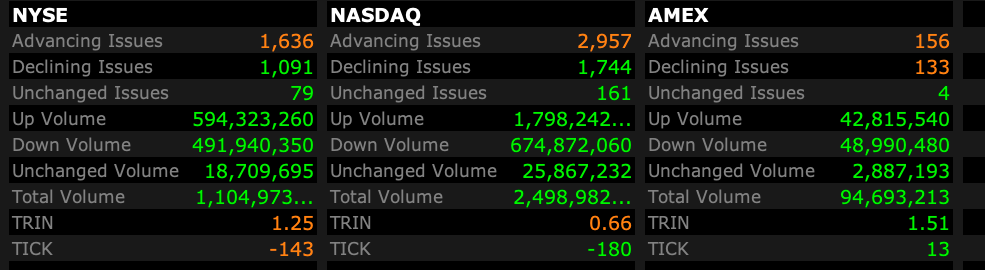

Closing Volume

- NYSE volume 1% below its one-month average

- NASDAQ volume 16% below its one-month average

- VIX index: up 0.59% to 16.99

Breadth

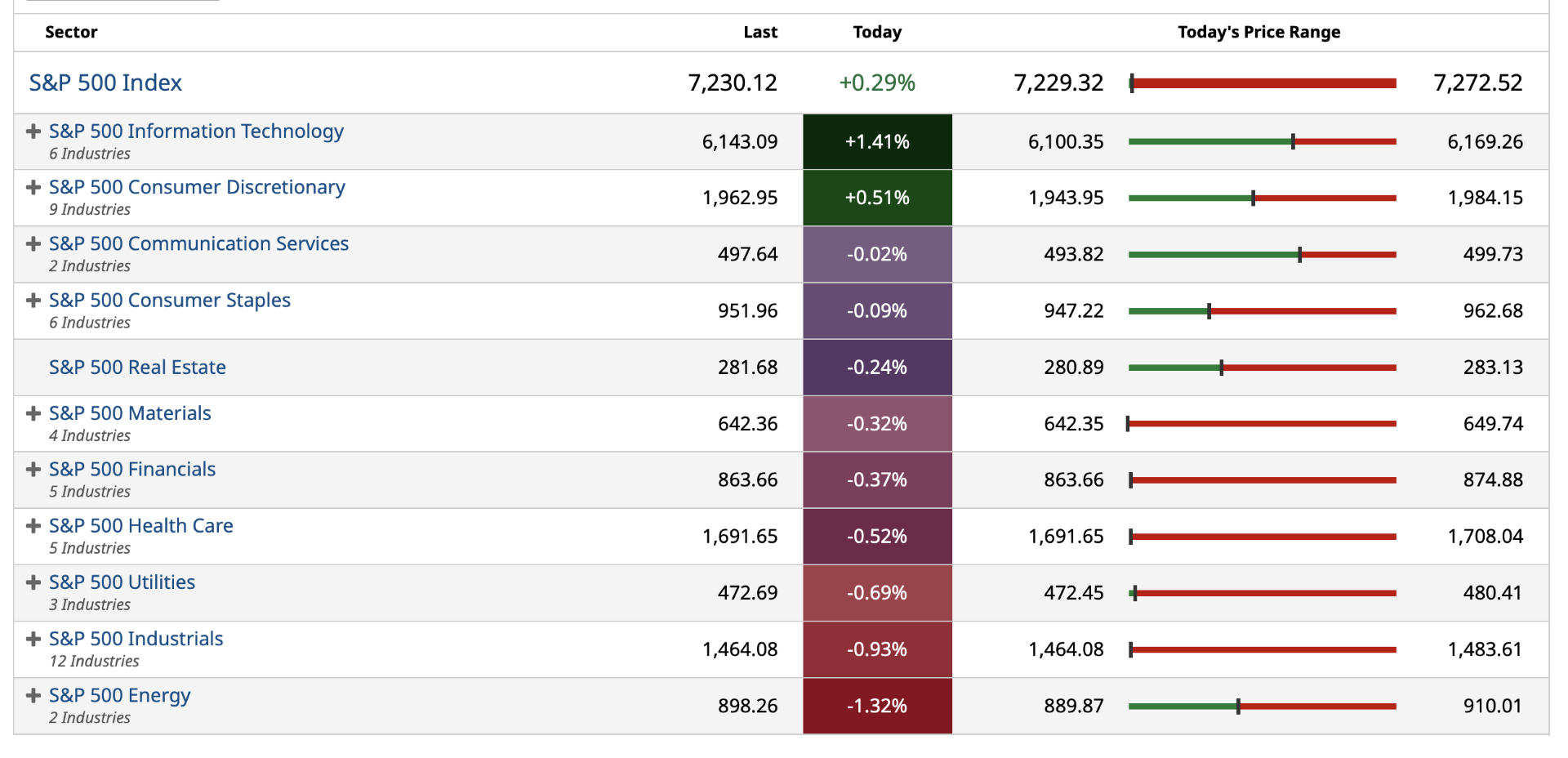

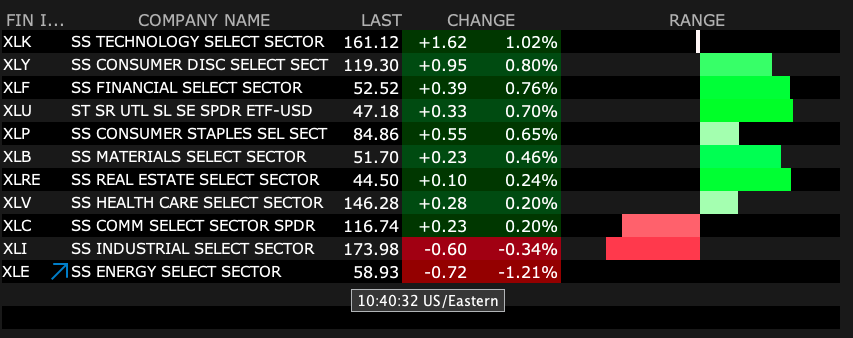

S&P 500 Sectors

% Movers

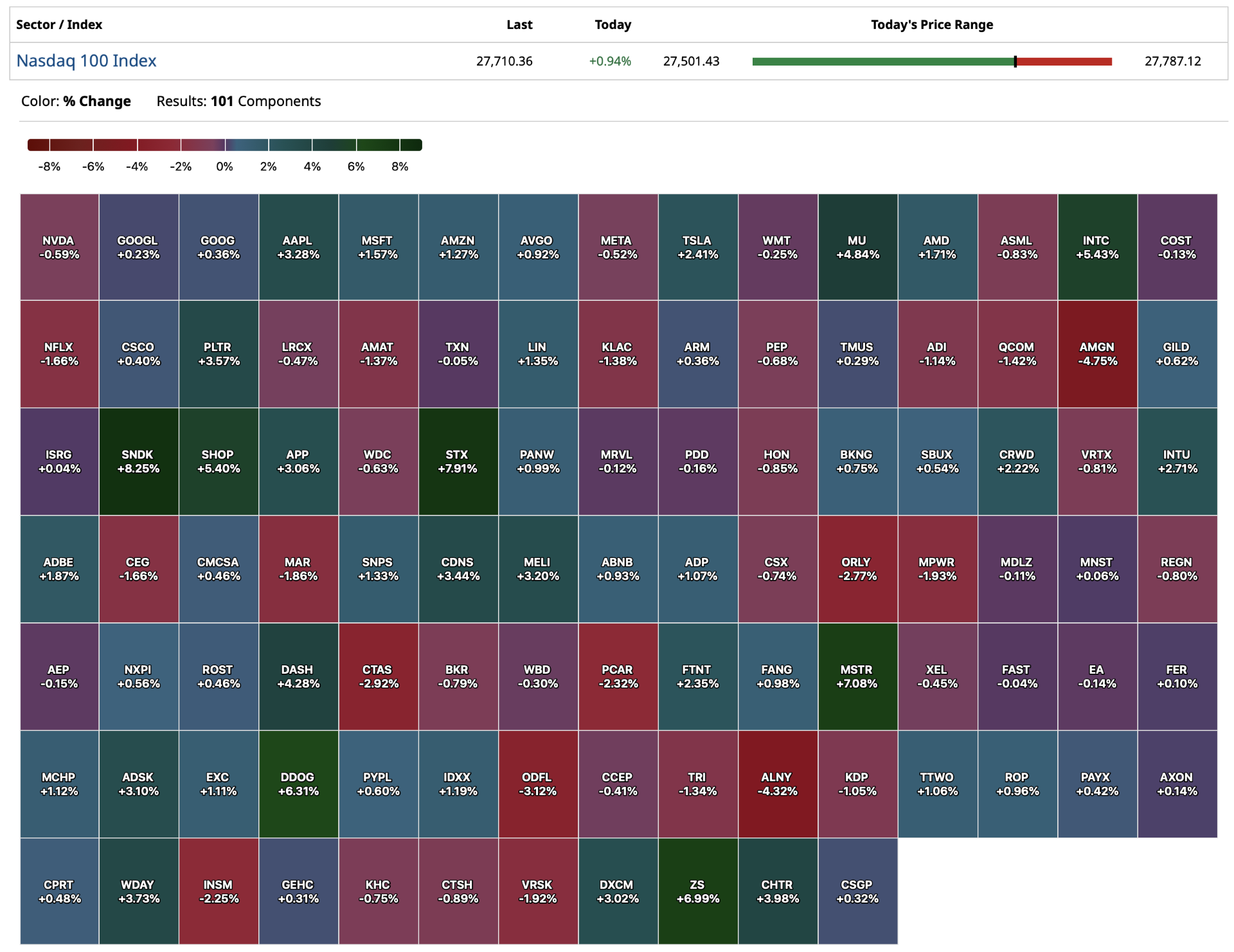

Nasdaq 100 Heat Map

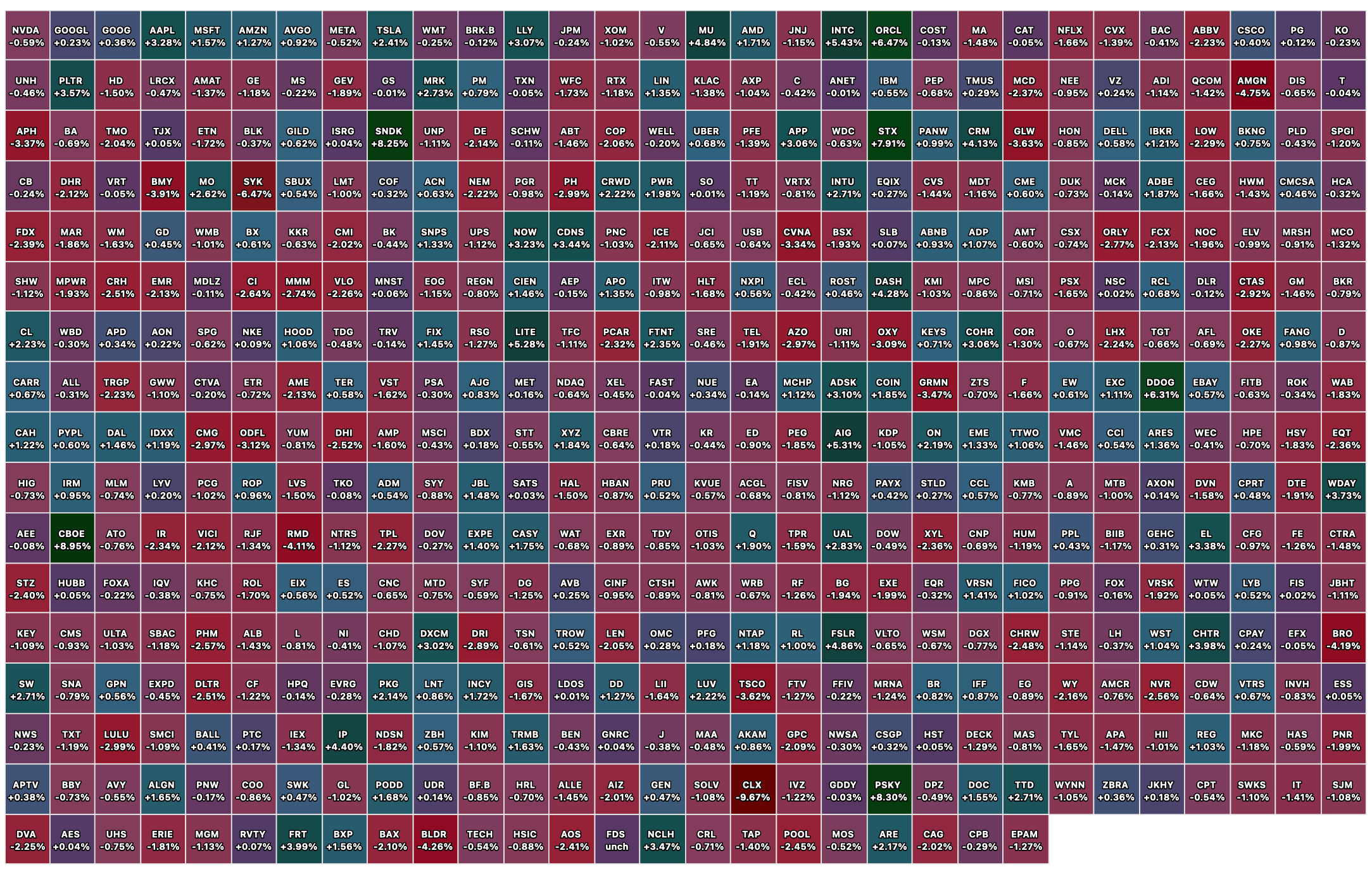

Closing S&P 500 Heat Map

BY Doug Kass · May 1, 2026, 4:30 PM EDT

As always I thank you all for providing me with this forum.

Enjoy the weekend

Be safe.

BY Doug Kass · May 1, 2026, 3:50 PM EDT

As one

“Keep your seatbelt fastened. When the tape starts running away like this, it tends to end not with a whisper, but a wobble. Seen it before — folks get a little too comfortable, then the trapdoor opens".

BY Doug Kass · May 1, 2026, 2:56 PM EDT

The SPX is about to hit its 4th all time high, of the past 5, on negative breadth: more decliners than advancers pic.twitter.com/cPWNXaSeRk

— zerohedge (@zerohedge)

BY Doug Kass · May 1, 2026, 2:45 PM EDT

BY Doug Kass · May 1, 2026, 2:30 PM EDT

Risk appetite among investors is skyrocketing:

— The Kobeissi Letter (@KobeissiLetter)

Risky asset fund inflows have exceeded safe asset fund inflows by a record $220 billion over the last 4 weeks.

Risky assets represent equities and corporate bonds, among others, while safe assets include money markets and Treasury… pic.twitter.com/y6wns4gTlp

BY Doug Kass · May 1, 2026, 2:10 PM EDT

The US Leading Economic Index is at 2014 levels.

— ₿rett (@brettmacro)

The disconnect between the stock market and the economy has never been this large.

Historically, stock market bottoms line up with USLEI bottoms.

Notice where the disconnect happened? The month ChatGPT was released in… pic.twitter.com/nsKCM78S2T

BY Doug Kass · May 1, 2026, 1:57 PM EDT

I have a 45-minute research call at 1:30 PM.

BY Doug Kass · May 1, 2026, 1:35 PM EDT

BY Doug Kass · May 1, 2026, 1:30 PM EDT

"When investing, I am often wrong and always in doubt."

- Grandma Koufax

Like Grandma, when I am wrong-sided on the market (and not trading with confidence)... I trade a lot less.

I don't pretend.

Position: None

BY Doug Kass · May 1, 2026, 1:20 PM EDT

BY Doug Kass · May 1, 2026, 1:10 PM EDT

Quotes U hear near the top, Kevin Simpson, on #CNBC, discussing $AAPL's valuation, "This isn't just a stock, it's the zeitgeist of the American consumer." God help us all. $QQQ

— edward m kelly (@ryan554)

BY Doug Kass · May 1, 2026, 1:00 PM EDT

BY Doug Kass · May 1, 2026, 12:50 PM EDT

The amazing thing in particular about Apple (AAPL) is that people are now paying 33x earnings for a 49% profit margin, a company record, and Tim Cook told us it's going lower in coming quarters because of skyrocketing component costs.

Position: None

BY Doug Kass · May 1, 2026, 12:40 PM EDT

BY Doug Kass · May 1, 2026, 12:30 PM EDT

BY Doug Kass · May 1, 2026, 12:10 PM EDT

The percentage of S&P 500 stocks outperforming the index over a rolling 21-day period fell to 21% on Wednesday.

— Turning Point Market Research (@TPMRSignals)

Since 1928, there have been only 59 other instances with weaker participation. pic.twitter.com/hBZu8uBMa8

Position: None

BY Doug Kass · May 1, 2026, 12:00 PM EDT

Hemp derived D9 would be in the crosshairs of S1 if the DEA keep this train moving. https://t.co/OBFlF9raXm

— Anthony Varrell (@V_arrell)

Position: None

BY Doug Kass · May 1, 2026, 11:45 AM EDT

🇺🇸 Here's what $39 trillion in debt really means:

— Hedgeye (@Hedgeye)

If we confiscated every dollar of U.S. corporate profit ($3.8T/year), it would take over 10 years to pay off.

Sell every ounce of gold ever mined: $32 trillion. Still $7 trillion short.

Liquidate every Bitcoin in existence on… pic.twitter.com/IYqsEiE7T9

BY Doug Kass · May 1, 2026, 11:35 AM EDT

Month beginning inflows overwhelming the markets.

I would normally short into this but I want to give the market a wider berth.

Positions: None.

BY Doug Kass · May 1, 2026, 11:20 AM EDT

- NYSE volume 7% above its one-month average;

- Nasdaq volume 19% below its one-month average;

- VIX index: down 0.89% to 16.74

Positions: None.

BY Doug Kass · May 1, 2026, 11:10 AM EDT

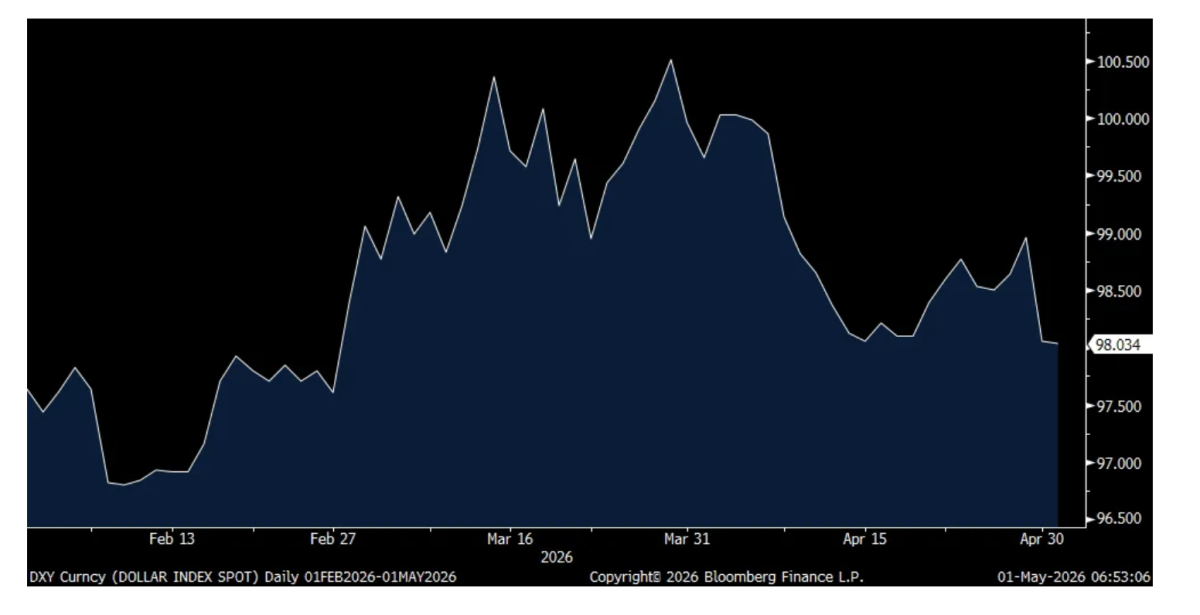

From Peter Boockvar:

Helped by this yen move and talk yesterday that the ECB might raise rates in June, the US dollar index has given back almost all of the post war rally. On the Friday before the war started the DXY closed at 97.6 and today is at 98.04 as of this writing. The commodity currencies have traded even better. The Aussie$ is just off the best level vs the US dollar in 4 years and the Canadian dollar has gotten back all that it lost since the war. The Brazilian real is at a 2 yr high vs the US dollar.

I believe the US dollar remains vulnerable as diversifying trade and capital flows are a secular trend now. We own international stocks and local currency emerging market bonds, along with gold and other commodities on this belief.

DXY

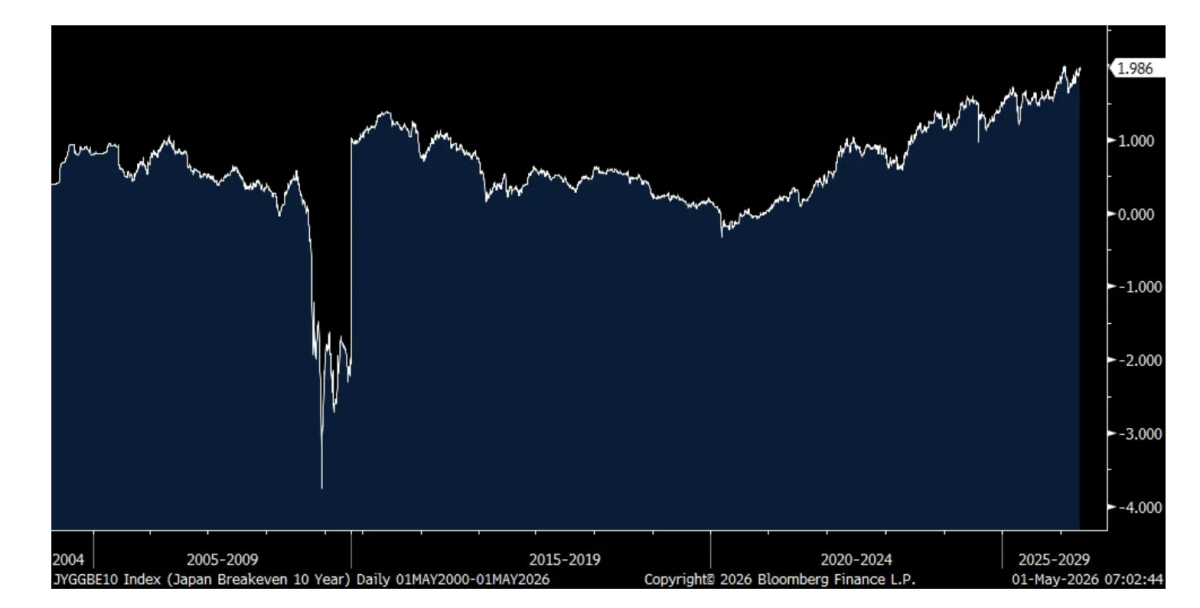

A day after the yen intervention and two days after the BoJ meeting, April Tokyo CPI rose 1.9% y/o/y, below the estimate of 2.2% but mostly because of childcare subsidies given out. That took away about a .5 percentage point to the headline figure that rose 1.5%. There is also energy subsidies included too. While the 10 yr JGB yield fell about 2 bps, the 10 yr inflation breakeven rose 1.2 bps to 1.99%. That is just 1 bp from matching a record high going back to when inflation linkers were first issued in Japan in 2004.

10 yr JGB Inflation Breakeven

Another flood of calls to go through so bear with me. The economic picture remains mixed with those touching the data center buildout and upper income consumers doing much better than other parts of the economy, still.

I’m hearing from more companies that want to raise prices. From Mohawk Industries, the carpet and flooring maker:

“Energy prices as well as the cost of oil and natural gas derivatives are increasing, which affects the cost of many of our products. We are implementing price increases across many product categories and geographies, and further price increases could be required. The impact of higher cost raw materials will be greater in the second half of the year due to our flow through of inventory.”

“Across our regions, the commercial sector continued to outperform residential. New home construction remained soft, and consumers continued to defer home purchases and remodeling projects due to economic uncertainty.”

From Scotts Miracle Gro, a stock we own:

In response to rising costs, particularly urea, “I do think pricing is going to be something that has to be used this coming year.”

Apple’s guidance was strong and while they have exciting new products it’s hard not to wonder how much is the front loading of ordering ahead of possible price increases and/or supply issues mostly in part due to the memory chip situation. To the current supply and cost challenges:

“We were constrained during the March quarter. This was primarily on iPhone and, to a lesser extent, on the Mac. And, as we talked about in the last call, the constraints were primarily driven by the availability of the advanced nodes our SoCs are produced on. If you look forward to the June quarter, the majority of our supply constraints will be on several Mac models, given the continued high levels of demand that we’re seeing. And we have less flexibility in the supply chain than we normally would.”

Cook also said, “let me talk about memory specifically...in the December quarter, we really had a minimal impact due to memory, and you kind of see that in the gross margin results. We said it would be a bit more in the March quarter, and we did see higher memory costs in the March quarter. And they were partially offset by benefits from carry-in inventory that we had. For the June quarter and what’s embedded in the guidance, we expect significantly higher memory costs. They are also partly offset by the benefit of carry-in inventory. And then where we don’t give color beyond June, I can tell you that, beyond the June quarter, we believe memory costs will drive an increasing impact on our business. And we’ll continue to evaluate this; and as we’ve said before, we’ll look at a range of options.”

I mentioned this week after we heard from Avalon Bay that the coastal apartment rental market is much better than the sunbelt where the former is still seeing rental increases because of supply constraints. As for the latter, Camden Property Trust, a stock we own, said in Q1 blended lease rates fell 1.4% with new leases down 5.2%, partly offset by a 2.9% rise in renewal rates. Q1 is seasonally soft so I await the conference call this morning to see how Q2 is shaping up.

From Ford, down 1% yesterday:

“In the US, we had our highest Q1 share of revenue in five years, led by large utilities and trucks.”

Ford Motor credit saw a rise in earnings “reflecting improvements in financing margin and enabled by a high quality book of business. Results also benefited from favorable performance on our derivatives.”

Commodity inflation is now going to cost them “just above $2 billion, about $1 billion higher than our previous estimate, largely due to higher aluminum pricing driven by global supply constraints.” On the flip side, “We have the $1.3 billion IEEPA tariff benefit.”

Not really much commentary on the consumer.

This was from last week but Robert Half, touching the labor market directly as a staffing company, said this:

“Resource levels at small and mid sized businesses, which represent the majority of our client base, remain lean following several years of cost discipline, creating capacity constraints as project activity begins to recover. In addition, broader labor market indicators continue to point to underlying demand for skilled talent. Unemployment remains low, particularly among college educated workers and in many of the roles we support, while job openings continue to run above historical averages.”

“Decision timelines remain extended, but are beginning to improve as companies revisit postponed initiatives and consider hiring tied to business critical priorities. Economic uncertainties related to the conflicts in the Middle East and higher energy costs have not yet significantly impacted client demand. However, concerns remain if these conditions persist.”

And what are they seeing from the impact of AI on the jobs market? “With respect to artificial intelligence, we continue to see limited impact on employment levels related to the roles we place in our specialties. AI is supported by multiple external studies, and there is very little evidence to data that AI adoption is leading to widespread job displacement. Instead, AI is reshaping the way work gets done and increasing the need for skilled professionals with domain expertise and enhanced AI skills who can also apply judgment, validate outputs, and support implementations.”

“In addition, the growing use of GenAI by job seekers has increased application volumes, made it more difficult to verify candidate qualifications, and made resumes more homogeneous and harder to differentiate. This further underscores the value of our services, including our proprietary data on candidate performance and our ability to deliver vetted, proven talent.”

From Caterpillar, whose stock had a big day yesterday and is now trading 50% above its 200 day moving average:

The drivers of the revenue and earnings gains, “In Power & Energy, sales to users grew a robust 32% with growth across all applications. Power generation grew 48%, driven by strong demand for large gen-sets and turbines used in data center applications with an increasing mix towards prime power. Sales to users in oil and gas increased 16%.”

Also, “Construction Industries total sales to users grew for the 5th consecutive quarter up 7%. Increases in North America were slightly better than we anticipated, mostly due to non-residential construction.”

SAIA, the trucking company, was up 6% yesterday and said:

“First quarter results were largely in line with our expectations as volumes in late March were strong, offsetting to some extent a weather impact in January and February…While trends in the first couple of months of the year can always be volatile, I was pleased to see the volume acceleration in the back half of March, resulting in a shipment increase of 1% for the quarter.”

They recapture higher diesel prices via surcharges.

From Group 1 Automotive, owner of car dealerships and whose stock rallied 2%:

“First quarter performance remained solid across most businesses, despite continued pressure on volumes and margins. New vehicle unit sales declined both on a reported and same store basis, reflecting not only ongoing affordability concerns, but a tough comparative period, which saw elevated new vehicle sales ahead of tariffs. However, new vehicle GPUs (gross profit per unit) increased sequentially from $3,260 to $3,313.”

“Our used vehicle operations performed in line with the broader market environment. Used vehicle retail units declined both on a reported and same store basis, which were partially offset by higher selling prices. GPUs declined approximately 3% on the same store and as reported basis, reflecting continued pressure on vehicle acquisition costs in a more competitive sourcing environment.”

On the growing issue of negative equity when customers turn cars in, “I think it’s a fact negative equity is at a high and can be a headwind. We try to watch affordability measures quite a bit. The average car payment is high, insurance rates are high, negative equity is high. But also there’s evidence that affordability is actually a little better now than it has been in some time when you look at car payments as a percentage of people’s salary and people’s pay.”

From Brunswick, the boat marker and whose stock was little changed yesterday:

“Global and US boat retail were approximately flat on a unit basis compared to the relatively strong first quarter of last year, and premium sales were up.”

“From an inventory perspective, boat and engine pipelines remain healthy, lean and well aligned with demand.”

“Fuel prices have risen recently due to geopolitical events but generally remain within historical bounds and we are not experiencing any clearly discernible direct impact on retail or OEM demand or on boating participation in our largest markets.”

“Current dealer sentiment is improved overall but still cautious, supported by healthy and fresh inventories and lower pre-owned boat supply which supports new boat demand. While incentives remain elevated versus historical norms, they improved approximately 100 bps last year and we are forecasting further modest improvement in 2026.”

From Hershey, which slipped by 2% yesterday in a very strong tape:

“Within our North American Confectionary segment, price elasticities were comparable to what we saw in the fourth quarter of 2025 and favorable versus planned levels. This was offset by unfavorable winter weather and consumer macro pressure, which we are monitoring closely. SNAP program changes had a mild impact on our categories given the limited states where waivers have taken effect.”

“We see continued consumer demand for confection, even as shoppers make more deliberate choices about their spending.”

Interesting here, “We’ve also seen strong demand for gum and mint products as the category benefits from functional snacking tailwinds, including GLP-1 adoption. Retail sales for our third largest confection brand, Ice Breakers, increased over 8% in the quarter.”

“Our North America Salty Snacks segment continued to demonstrate strong momentum in the first quarter.”

Blue Owl Capital rebounded by 10% yesterday and they said this of note:

“In recent months, we’ve spent time with clients and other stakeholders addressing the questions that have arisen around private credit...Across the business, fundamental performance remains strong and portfolios remain strong, and the portfolios continue to behave in line with the discipline with which they were built.”

“direct lending represents only 37% of Blue Owl’s AUM.” And, “in direct lending, underlying portfolio company growth has remained healthy with no meaningful adverse movement in metrics such as our watch list, non-accruals, amendment requests or revolver draws. Our average annual loss rate remains a very low 12 basis points, an important factor in driving our continued outperformance to leverage loan and high yield indices.”

More on this, “We have seen no material negative developments in our portfolios in terms of amendments, in terms of PIK, in fact, PIK has been on a decline as a percentage of the portfolio.”

“While the level of debate around private credit has resulted in elevated industry wide redemption requests, the actual impact of Blue Owl’s revenues and earnings for the first quarter was quite modest.”

From International Paper and whose stock got whacked by 9% yesterday:

“In both North America and EMEA, overall market demand is softer than we expected coming into the year by about a point. This reflects a more cautious consumer, particularly as inflation pressures and uncertainty persist. We have not seen abrupt changes in order patterns in either region, but I’m cautious about demand. Visibility beyond the near term is limited.”

“Lastly, due to macro trends, our full year 2026 industry demand outlook is now approximately flat y/o/y compared to prior assumptions of flat to up 1%.”

From Wayfair and whose stock fell 13% yesterday:

“The home furnishings category has had a choppy start to the year with weather disruptions in the front part of the quarter leading right into a broader pullback in consumer spending, driven by elevated energy and fuel prices. Sometimes we get asked why weather would impact an online business and the answer is pretty simple. Weather disrupts our customers lives and when you have no power or your children are home from school, you’re simply not shopping for home goods.”

“By our estimates, the home furnishings category was down in the low single digit range for the first quarter, suggesting that we outperform the market by a high single digit spread.”

Royal Caribbean had a good quarter as cruising remains popular and with a 4% pop yesterday they said this:

“The consumer backdrop remains healthy, and demand for our vacation experiences continues to be strong. Across our portfolio, we see consistent engagement from guests, strong booking volumes, and onboard spending that remains well above prior years.”

“The most notable financial impact from the Middle East conflict has been on fuel costs. While we are approximately 60% hedged for 2026, fuel prices at current spot levels are expected to increase costs by roughly $.62 per share this year.”

“In addition to fuel, we saw a short term moderation in demand trends for 2026 for high-yielding Mediterranean sailings, which modestly impacted our outlook for the upcoming summer season. The softer booking trends lasted for a few weeks, but we have now turned a corner and we are experiencing improved demand for the limited inventory we have remaining for Q2 and Q3 sailings. Lastly, we experienced some disruption in demand for select West Coast Mexico itineraries driven by travel disruption concerns during the quarter. Demand trends for other products remain largely consistent with our expectations.”

Positions: None.

BY Doug Kass · May 1, 2026, 9:36 AM EDT

-CUE +91% (expands Pipeline with Exclusive License from Ascendant Health Sciences Ltd. for Clinical-Stage Dual-Mechanism Anti-IgE Antibody)

-ESPR +57% (to be acquired by ARCHIMED at $3.16/shr)

-TWLO +24% (earnings, guidance)

-FIVN +19% (earnings, guidance)

-TEAM +19% (earnings, guidance)

-WEAV +17% (earnings, guidance)

-EL +12% (earnings, guidance; cutting additional jobs)

-VEEV +11% (to be added to S&P500, effective May 7th)

-ZETA +8.1% (earnings, guidance)

-ROKU +7.4% (earnings, guidance)

-MRNA +6.9% (earnings, guidance)

-CBOE +6.1% (earnings, guidance)

-HUN +5.6% (earnings, guidance)

-TWO +5.6% (UWMC increases cash election from $11.30/share to $12.00/share through issuance of open letter to Two Harbors Stockholders)

-PS +4.5% (momentum following IPO)

-GDDY +4.1% (earnings, guidance)

-PSKY +3.7% (Morgan Stanley Raised PSKY to Overweight from Underweight, price target: $14)

-CHD +3.6% (earnings, guidance)

-AAPL +3.5% (earnings, guidance; announces buyback)

-RIOT +2.7% (reports revenue)

-ARES +2.6% (earnings)

-BAFN -37% (earnings, guidance)

-RBLX -24% (earnings, guidance)

-RNTX -21% (prices 50M shares at $1.00/share)

-SMMT -20% (earnings)

-GRO -11% (prices $55M public offering of common shares and pre-funded warrants)

-ATMU -9.8% (earnings, guidance)

-RYAN -9.4% (earnings, guidance)

-CLX -6.5% (earnings, guidance)

-FND -6.1% (earnings, guidance)

-DXCM -3.4% (earnings, guidance)

-SNDK -3.2% (earnings, guidance; approves buyback)

-AMGN -2.4% (earnings, guidance)

-RIVN -2.2% (earnings, guidance)

Positions: None.

BY Doug Kass · May 1, 2026, 9:09 AM EDT

Positions: None.

BY Doug Kass · May 1, 2026, 9:00 AM EDT

BY Doug Kass · May 1, 2026, 8:38 AM EDT

Positions: None.

BY Doug Kass · May 1, 2026, 8:23 AM EDT

Positions: None.

BY Doug Kass · May 1, 2026, 8:15 AM EDT

🇺🇸 S&P 500

— ISABELNET (@ISABELNET_SA)

The market used to be a mirror. Now it acts more like a megaphone. Ten mega-caps account for 40% of the S&P 500, stretching valuations and amplifying volatility

👉 https://t.co/yIk7SZYp6p@GoldmanSachs $spx #spx #sp500 #stocks #equity pic.twitter.com/ESZFTYqbtC

BY Doug Kass · May 1, 2026, 8:00 AM EDT

JUST IN: 🇺🇸 US national debt surpasses size of the entire United States GDP for first time since World War II. pic.twitter.com/15fcysvCep

— Watcher.Guru (@WatcherGuru)

BY Doug Kass · May 1, 2026, 7:50 AM EDT

AI Still Has A Real Economy Problem

— Bob Elliott (@BobEUnlimited)

The hyperscaler earnings bonanza last night continued to show that AI related capex is still only delivering marginal incremental growth benefits in end real economy activities like advertising.https://t.co/TJ6VNsnXH8 pic.twitter.com/QNPflbqGhS

BY Doug Kass · May 1, 2026, 7:40 AM EDT

From The Street of Dreams:

On April 12, we published a piece with a section titled, “Why aren’t oil prices higher?” Here’s what I wrote: Over the weekend, I had a subscriber express his frustration to me: “How can the oil market be so complacent?” Let me answer that question by first saying this: I’ve been neck deep in the oil market for the last 11 years. And oil prices almost always trade to extremes. Right before it does, it always gets “obvious” from a fundamental setup standpoint. I remember a great conversation I had with Nelson Wu of Open Square Capital about the oil market being analogous to toilet paper. You don’t realize how badly you need it until you run out of it. Oil prices trade on the margin. As long as there are onshore inventories to draw from, traders don’t panic. It’s when you run low on onshore inventories that panic starts to set in. Goldman published an update on Thursday that basically captured the storage math phenomenon that we are seeing: Global visible total oil inventories remain bloated relative to historical standards. If, for example, we had started the conflict with global oil inventories at the 2025 lows, WTI and Brent would already be above $200/bbl. The ~1.4 billion bbl cushion at the start of 2026 is what gave the US time to navigate the Iranian conflict without the oil market blowing up. It was also the same reason why at the beginning of the conflict, I wrote a piece titled, “Why Aren’t Oil Prices At $100?” But fast forwarding 6-weeks later, the facts have changed. The conflict is ongoing, and that onshore cushion you are seeing in storage is nothing but a mirage. Even if the conflict ends this very second and everything returns to normal, that oil inventory is gone. Vanished. No more. In essence, the oil market really should be pricing forward balances as if we are already near 7.6 billion bbls, but it’s not, and this creates the biggest mispricing trade since the COVID lockdown (short oil) trade. Oil traders, the physical guys, lack both the means and capabilities to drive financial prices higher. Financial markets are exponentially larger than the physical side, but there’s one quirk: expiry. As the futures market approaches expiry, people who continue to hold the contracts are obligated to deliver the goods (literally). This mechanism will be tested first at the May WTI expiry, where the physical market is already quoted at a +$20 premium to financial prices. It will be tested again in the Brent expiry at the end of the month. What will happen is that as we get closer to the expiry, market participants who are short have to cover because there’s no way in hell they can deliver the goods physically. We are literally going to run out of available commercial crude storage. This will force the prompt month higher, which will suck in financial flows into the June contracts. This inflection point will shock market participants awake. This is one of the main reasons why I’ve remained so calm over the past few weeks. The math is what it is. The Trump administration can jawbone oil prices all they want. Axios can publish whatever headlines it wants, but the reality will be swift and vicious. If you do not have the means to deliver the goods, you have to cover.

Position: None

BY Doug Kass · May 1, 2026, 7:30 AM EDT

Ladies and gentlemens, dignitaries, celestial beings, royals, harbingers, and past kings...Behold!

— The Great Martis (@great_martis)

We stand at the precipice of financial history, gazing upon the sacred scrolls of valuation the Shiller PE Ratio (CAPE), that venerable cyclically adjusted oracle of the S&P 500.… pic.twitter.com/K6NjTapjQ9

BY Doug Kass · May 1, 2026, 7:20 AM EDT

BY Doug Kass · May 1, 2026, 7:10 AM EDT

Wolf Street howls about core PCE inflation's rise.

BY Doug Kass · May 1, 2026, 7:00 AM EDT

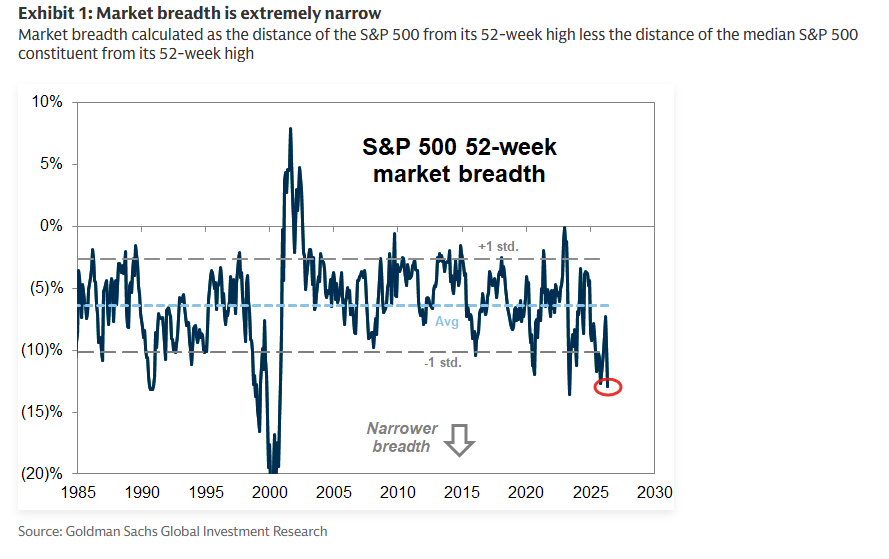

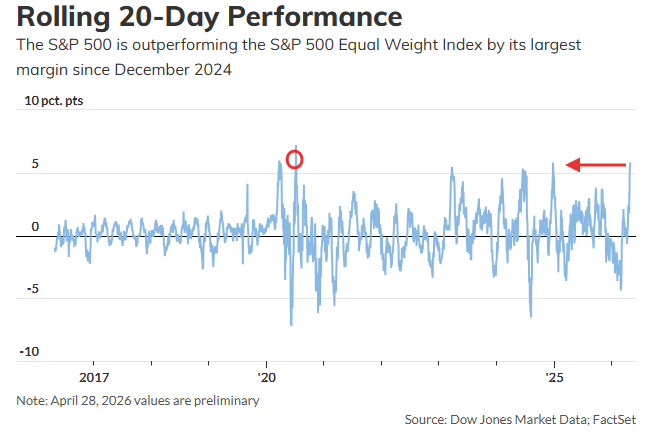

Chart of the Day: The Market's Advance Narrows (S&P is outperforming the equal weighted Index by largest margin since December 2024)

The Equal Weight S&P 500 (RSP) snapped a seven-day losing streak, and logged its fifth-best daily gain of the year.

Coming into today, the cap-weighted S&P 500 had outpaced the equal weight by the widest margin since December 2024, underscoring the outsized leadership from mega-cap names off the recent lows.

While RSP still hasn’t reclaimed its February highs, improving momentum across the broader market paints a constructive backdrop for a potential next leg higher.

The Takeaway: Today's action in the equal weight S&P suggests underlying strength is expanding beyond the market's largest stocks.

-

After just one week, the AAII Sentiment Survey Bull/Bear spread has flipped back into negative territory.

— Optuma (@Optuma)

We just saw a -13.2 swing - the largest weekly sentiment drop since mid-November. pic.twitter.com/zlyJqom090

The S&P 500 is having a huge April, up more than 9% right now.

— Ryan Detrick, CMT (@RyanDetrick)

10 other times in history it gained >5%.

May was higher 9 of those times and both the Sell in May (May - Oct) period and the rest of the year were up substantially better than the average returns. pic.twitter.com/xA4wFv1NaO

Sectors’ percentage of stocks trading at various period highs pic.twitter.com/JCNEU6Au9a

— Liz Ann Sonders (@LizAnnSonders)

Bulls winning the battle so far today. https://t.co/AzNfg7ms8Q pic.twitter.com/suuw0dJnZ0

— Bob Sheehan, CFA, CMT (@LHMacro)

The Week in Charts (4/29/26) - Charlie Bilello's Blog

Agricultural commodities look poised to begin their 10th cyclical upcycle since the 1960s. Recognizing sector leadership trends that develop during these phases is essential, and we recently shared our findings with subscribers. pic.twitter.com/QdUyV19OYX

— Turning Point Market Research (@TPMRSignals)

Bonus — Here are some great links:

BY Doug Kass · May 1, 2026, 6:45 AM EDT

Having correctly called and/or sidestepped the three biggest declines in my 42-year career, I'm highly confident that my most bearish position now towards the U.S. stock and bond market can make me 4 for 4.

— Peter Grandich (@PeterGrandich)

Having Paul Tudor Jones in the same camp adds to my confidence!… https://t.co/T5N32ON1Q5

BY Doug Kass · May 1, 2026, 6:35 AM EDT

Consumer sentiment is near historic lows. Stocks are near historic highs.

— Elliott Wave International (@elliottwaveintl)

That divergence is hard to ignore.

In fact, U.S. consumer sentiment is now lower than it was at the depths of the 2008 financial crisis.

What happens when perception and price finally reconnect? Get free… pic.twitter.com/vRXzfVoaDQ

BY Doug Kass · May 1, 2026, 6:25 AM EDT

Shorting the indices (remain small, though):

* (SPY) $720.15

* (QQQ) $667.56

Position: Short SPY (VS), QQQ (VS)

BY Doug Kass · May 1, 2026, 6:15 AM EDT

GDP Shocker: 75% Of US Growth In The First Quarter Was Due To AI https://t.co/S7uCRwhDKJ

— zerohedge (@zerohedge)

BY Doug Kass · May 1, 2026, 6:05 AM EDT

The S&P Short Range Oscillator moved to a more overbought reading of 2.48% vs. 1.12%

Position: Short SPY (VS), QQQ (VS)

BY Doug Kass · May 1, 2026, 5:55 AM EDT

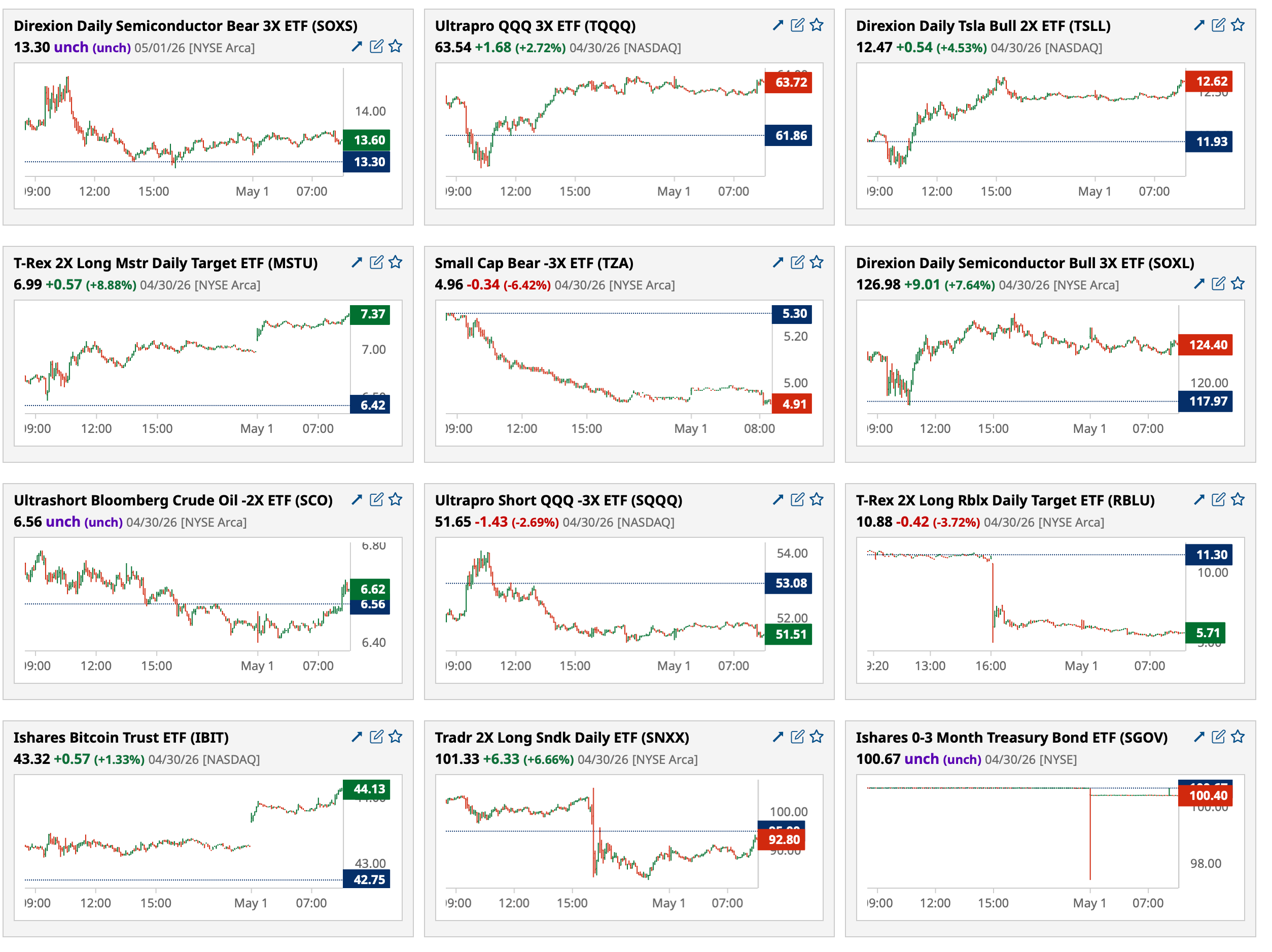

Retail investors are piling into leveraged semiconductor ETFs at an unprecedented pace:

— The Kobeissi Letter (@KobeissiLetter)

Combined daily trading volume in the 3x leveraged short semiconductor ETF, $SOXS, and the 3x leveraged long semiconductor ETF, $SOXL, has surged to ~330 million shares, the highest in at… pic.twitter.com/6tRnn4VtO4

Position: Short AMD (S), MU (S), INTC (S)

BY Doug Kass · May 1, 2026, 5:45 AM EDT

The embedded tweet could not be found…

The percentage of S&P 500 stocks outperforming the index over a rolling 21-day period fell to 21% on Wednesday. Since 1928, there have been only 59 other instances with weaker participation.

The SPX is about to hit its 4th all time high, of the past 5, on negative breadth: more decliners than advancers

I’ve been trading for 40 years, and I’ve seen this kind of runaway bull market before. This market looks vulnerable to an abrupt ~1% downside close. Chasing here isn’t advisable — it’s reminiscent of the late-stage surge in March 2000. Had Art Cashin lived, he might have said: Show more

Risk appetite among investors is skyrocketing: Risky asset fund inflows have exceeded safe asset fund inflows by a record $220 billion over the last 4 weeks. Risky assets represent equities and corporate bonds, among others, while safe assets include money markets and Treasury Show more

GDP Shocker: 75% Of US Growth In The First Quarter Was Due To AI zerohedge.com/economics/gdp-…

Sectors’ percentage of stocks trading at various period highs

After just one week, the AAII Sentiment Survey Bull/Bear spread has flipped back into negative territory. We just saw a -13.2 swing - the largest weekly sentiment drop since mid-November.

The panelists are breathless on the show. @HalftimeReport

AI Still Has A Real Economy Problem The hyperscaler earnings bonanza last night continued to show that AI related capex is still only delivering marginal incremental growth benefits in end real economy activities like advertising. bobeunlimited.substack.com/p/ai-still-has…

The US Leading Economic Index is at 2014 levels. The disconnect between the stock market and the economy has never been this large. Historically, stock market bottoms line up with USLEI bottoms. Notice where the disconnect happened? The month ChatGPT was released in Show more

Consumer sentiment is near historic lows. Stocks are near historic highs. That divergence is hard to ignore. In fact, U.S. consumer sentiment is now lower than it was at the depths of the 2008 financial crisis. What happens when perception and price finally reconnect? Get free Show more

Ladies and gentlemens, dignitaries, celestial beings, royals, harbingers, and past kings...Behold! We stand at the precipice of financial history, gazing upon the sacred scrolls of valuation the Shiller PE Ratio (CAPE), that venerable cyclically adjusted oracle of the S&P 500. Show more

🇺🇸 S&P 500 The market used to be a mirror. Now it acts more like a megaphone. Ten mega-caps account for 40% of the S&P 500, stretching valuations and amplifying volatility 👉 isabelnet.com/?s=S%26P+500 @GoldmanSachs $spx #spx #sp500 #stocks

JUST IN: 🇺🇸 US national debt surpasses size of the entire United States GDP for first time since World War II.

🇺🇸 Here's what $39 trillion in debt really means: If we confiscated every dollar of U.S. corporate profit ($3.8T/year), it would take over 10 years to pay off. Sell every ounce of gold ever mined: $32 trillion. Still $7 trillion short. Liquidate every Bitcoin in existence on Show more

Agricultural commodities look poised to begin their 10th cyclical upcycle since the 1960s. Recognizing sector leadership trends that develop during these phases is essential, and we recently shared our findings with subscribers.

Hemp derived D9 would be in the crosshairs of S1 if the DEA keep this train moving.

The DEA just made a major announcement: They have officially classified HHC as a Schedule I controlled substance and assigned it its own DEA drug code. What’s important here is the reasoning they used: They’re clarifying that only cannabinoids naturally produced by the cannabis

Bulls winning the battle so far today.

Having correctly called and/or sidestepped the three biggest declines in my 42-year career, I'm highly confident that my most bearish position now towards the U.S. stock and bond market can make me 4 for 4. Having Paul Tudor Jones in the same camp adds to my confidence!Show more

Paul Tudor Jones says the US is more dependent on equity prices than ever, and explains what a 35% correction would trigger in the economy: "We're 252% of stock market cap to GDP. In 1929 we were 65%. In 1987 we got to ~85-90%. In 2000, 170%. If you think about the periodicity