From Peter Boockvar:

Positives,

1) In the payroll report, the workweek at 34.3 was as expected and unchanged m/o/m. Average hourly earnings were up by .4% m/o/m, one tenth more than expected and with a 3.9% y/o/y gain. Combining the two saw average weekly earnings higher by .4% m/o/m and 3.9% y/o/y.

2) In the ADP jobs report, there wasn’t much change in wages from April but still pretty good with ‘job stayers’ seeing a 4.5% wage gain, the same pace last month. For ‘job changers’, wages rose 7% vs 6.9% in the month before.

3) Challenger said hiring plans did increase by 57% y/o/y but also said, “it remains historically low when compared to pre-pandemic and early-pandemic years.”

4) The April job openings count was 7.39mm, up about 200k m/o/m, above the estimate of 7.1mm and vs 7.48mm in February. The hiring rate rose one tenth to 3.5% after four months of 3.4% prints. The quit rate though slipped one tenth to 2%.

5) Mathematically good for GDP but obviously tariff distorted, the April trade deficit plunged to $61.6b because of a 16.3% collapse in imports, well more than offsetting the 3% rise in exports. The estimate was $66b and down from $138b in March.

6) Steel companies get the benefit of 50% tariffs on their competitors. The impact is more mixed for aluminum companies.

7) From Dollar General: Comps were up 2.4% y/o/y in the quarter, "driven by growth of 2.7% in average basket, including relatively similar increases in average unit retail price per item and average items per basket. Customer traffic slightly decreased by .3% during the quarter, but remained strong on a two year stack as we lapped the 4.3% traffic increase from the prior year's first quarter. We are excited to see broad based category growth during the quarter with positive comp sales in each of our consumables, seasonal, home and apparel categories."

8) From Dollar Tree: "Each week, more shoppers across a diverse range of economic and demographic backgrounds are responding to the appeal of Dollar Tree's unique value, convenience, and discovery proposition...New customers and increasing trip frequency are both driving share gains…Trade-in trends remains strong as we attract customers from other retail channels. In recent quarters, higher income customers have been a meaningful growth driver for us. In Q1, we had measurable sales improvement across all income levels, with the most growth coming from our higher income customers. In particular, we saw a meaningful traffic increase from customers with household incomes of more than $100,000, demonstrating Dollar Tree's broad appeal."

9) From Five Below: Their comps grew 7.1% and via increased transactions of 6.2% and comp ticket of .9%. Their strategy, "Providing fresh, trend-right, and quality products at amazing value is what we are known for and what makes us special."

10) From Cracker Barrel: "In our third quarter, as we noted on the last call, February started out a bit challenged as a result of both weather and some consumer uncertainty. Then we saw improvements into March and into April. And then we're particularly pleased that improvement continued further into Q4."

11) From American Express: On business, "It's really been consistent. What we've seen through May is what we saw through April and what we saw in March and in the first quarter, and so goods and services consistent. Airline, pretty consistent, and we said that was down a little bit. I think lodging gets a little more challenged, but restaurant is still very, very strong. And if you look at the individual segments, international, SME, and US consumer, pretty consistent to the way they are. So, unless something crazy happens in June, I think when we start talking about this in July, we're going to say, the second quarter pretty much looked just like the first quarter did, FX adjusted, and all that other kind of stuff."

12) From MasterCard: They reported earnings on April 28th, so this view is obviously a month later. "Now, if you include the first three weeks of May, we see exactly the same. So, spending trends have largely been the same, Now, if you look at this a little bit closer and then you'd say, why is that? If you look at the headlines, if you look at the sentiment surveys, and we just saw one yesterday, it was surprisingly positive. So, you see a lot of rhetoric there, and you see a lot of headlines, and it hasn't really translated into consumer behavior. So, why is that? Because the underlying support of the labor market continues to be there. We still have low unemployment, and we have wage growth that is kind of keeping up with inflation, above inflation. So, purchasing power is solid, which are both key drivers."

13) From Signet Jewelers: "We delivered positive same store sales growth each month of the quarter, and into May, by bolstering our offerings at key price points and continuing the evolution of our assortment. Our three largest brands - Kay, Zales, and Jared - all saw sequential comp sales improvement from the fourth quarter on higher margins, highlighting the impact of our outsized focus on our larger brands."

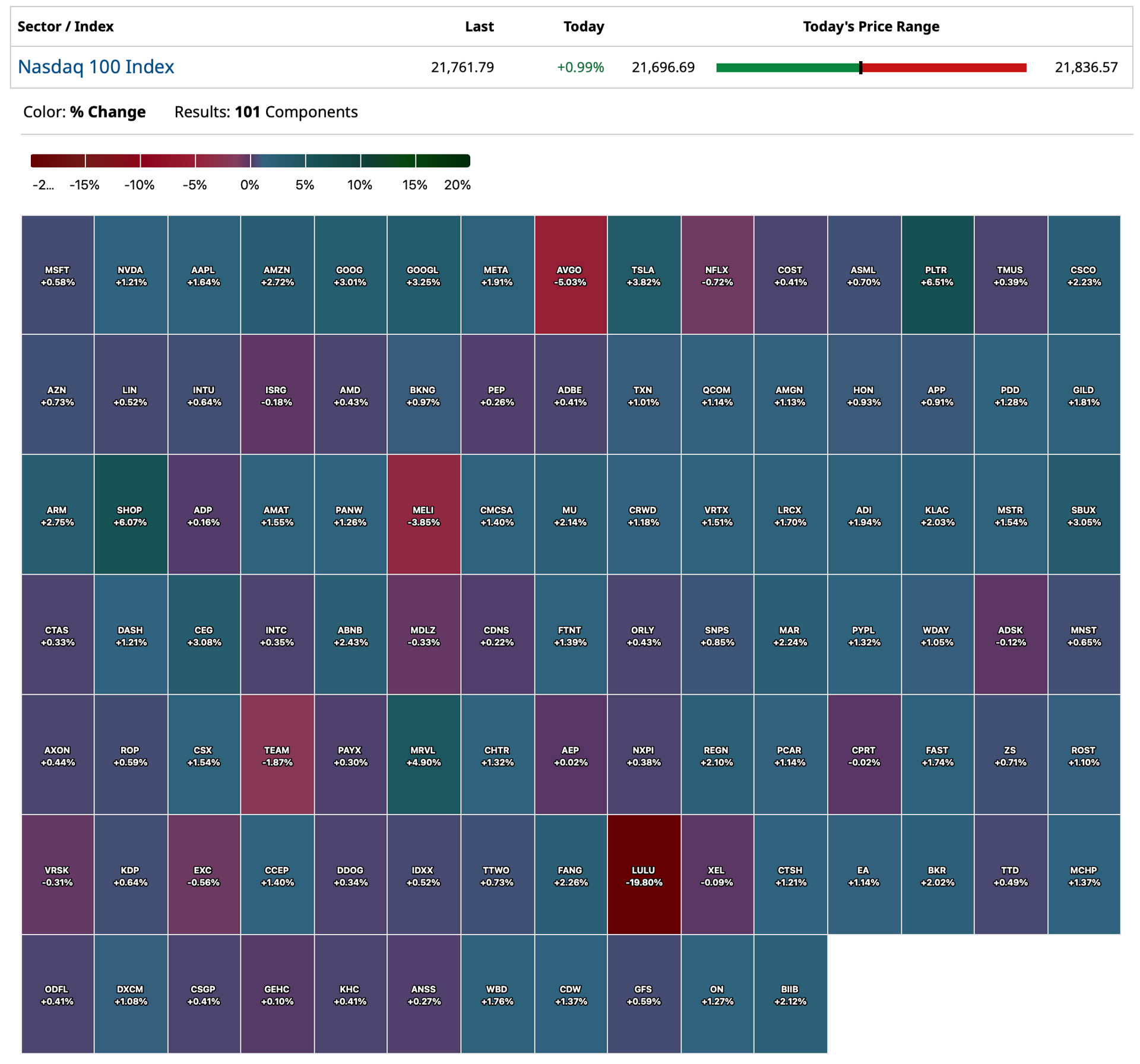

14) From Broadcom: Their AI chip business is seeing huge growth, up 46% y/o/y in the quarter just reported and in the current quarter they are in they see 60% y/o/y growth.

15) Depending on one’s view of the Canadian economy, this could have been a negative instead. The Bank of Canada kept policy unchanged as expected at 2.75%.

16) The Reserve Bank of India cut rates by 50 bps to 5.50% where only 25 bps was expected. While India is already seeing solid growth, the RBI Governor said "Our aspiration is to grow at 8% and we would like to grow as fast as possible."

17) China's May private sector services Caixin PMI rose a touch to 51 from 50.7 and as expected. Caixin said, "Overall sentiment remained positive in the Chinese service sector midway through the 2nd quarter of 2025. Firms were hopeful that improvements in global trade conditions and business development plans could help to spur sales and boost activity levels over the next 12 months. The level of confidence strengthened since April, but remained below average."

18) The May Eurozone services PMI was revised up from its previous read to 49.7 from 48.9 but still down from 50.1 in April and is the lowest since last November. S&P Global said "A shaper drop in international orders was partly to blame, with export sales also falling to the quickest degree since November last year."

19) The UK May services PMI held above 50 as it was revised to 50.9 from 50.2 initially and up from 49 in April and vs 52.5 in March. S&P Global said, "The service sector regained its poise in May as receding concerns about US tariffs, recovering global financial markets and greater confidence among clients all helped to support output growth."

20) The Eurozone May CPI was higher by 1.9% y/o/y, down from 2.2% in the month before and one tenth less than expected. Helping to keep a lid on the headline was the 3.6% y/o/y drop in energy prices. The core rate slowed to 2.3% y/o/y from 2.7% and that was also one tenth below the estimate.

21) China's state sector weighted manufacturing PMI rose a .5 pt to 49.5 as expected. The non-manufacturing component remained above 50 at 50.3 vs 50.4 in the month before.

Negatives,

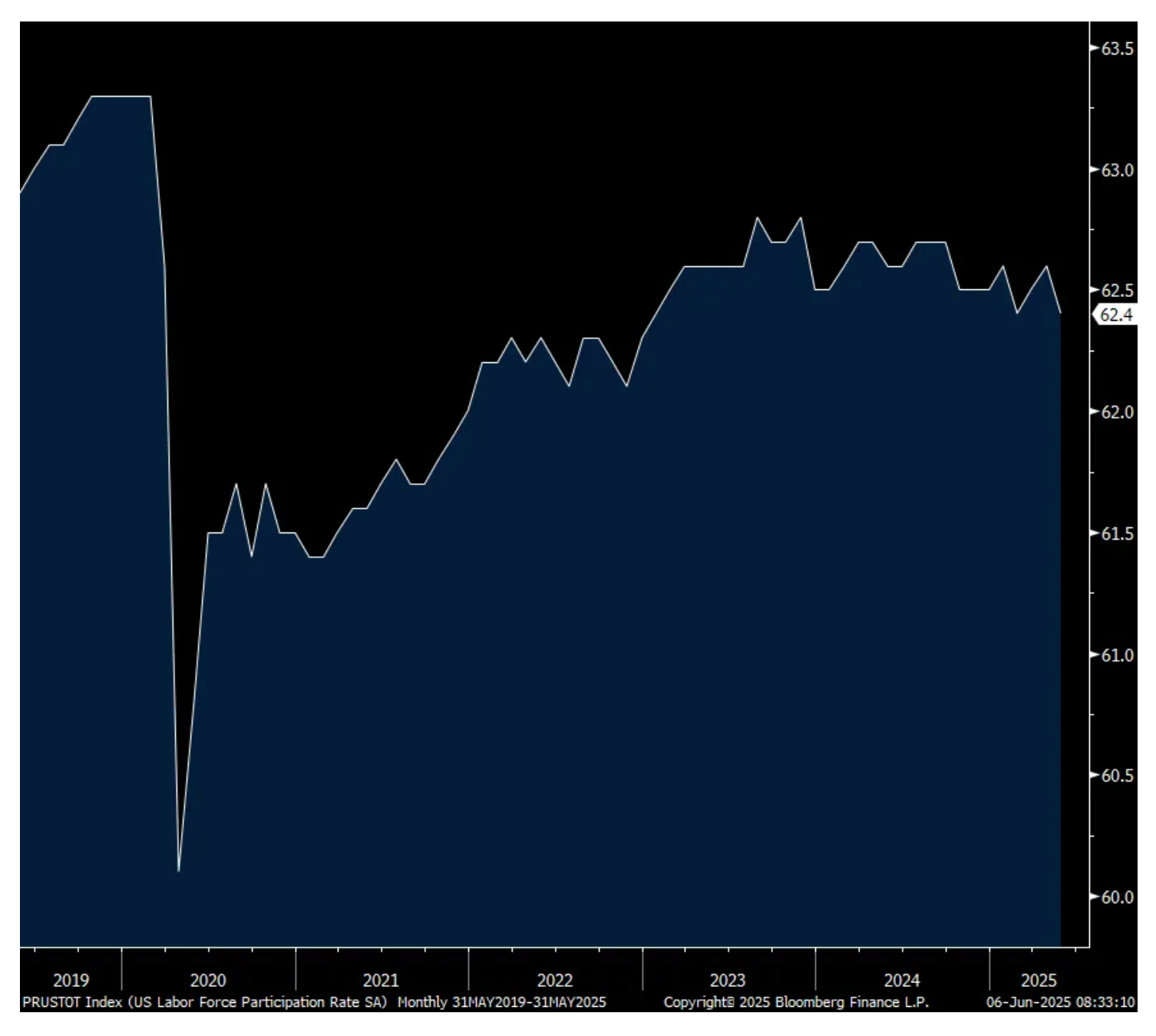

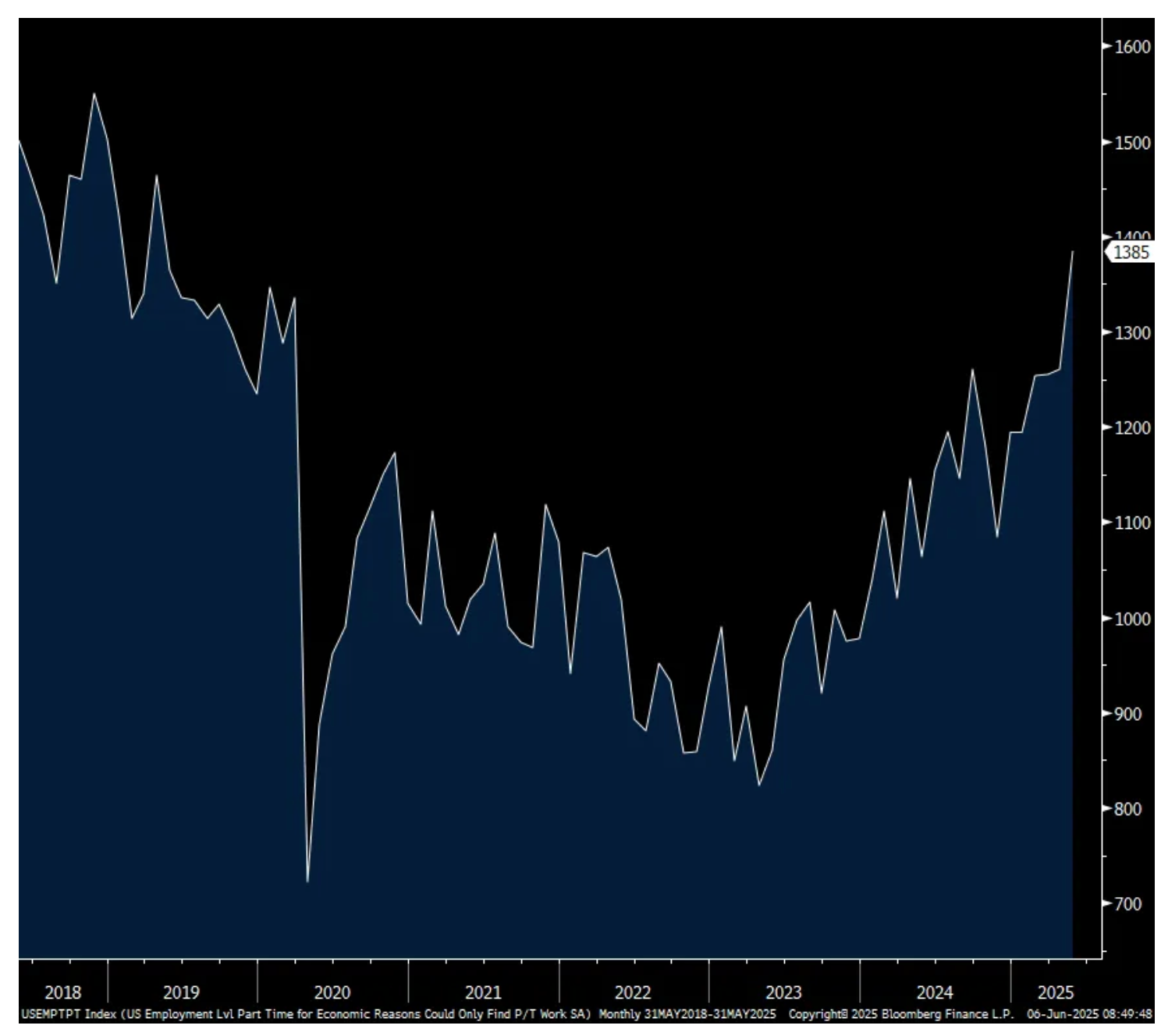

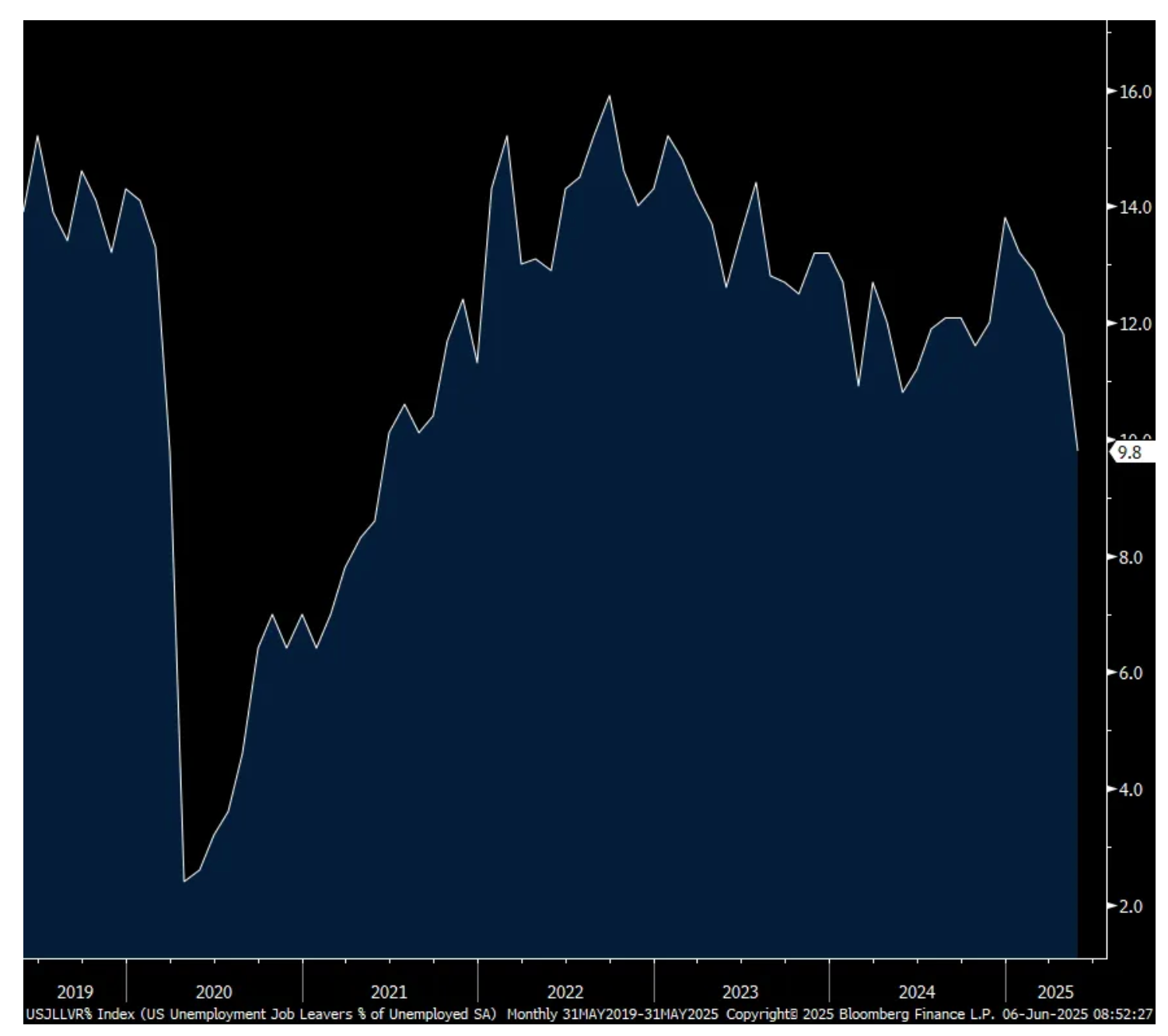

1) Payrolls in May rose a net 139k, 13k above expectations but the two prior months were revised lower by a combined 95k. There was a large decline of 696k jobs in the household survey but is very volatile month to month. As this though matched the 625k person decline in the labor force, the unemployment rate held at 4.2% for a 3rd straight month. Helping to explain the big drop in the labor force was the participation rate that fell to 62.4% from 62.6% and that matches the lowest since December 2022. The participation rate for the key 25-54 yr old age cohort also fell two tenths m/o/m to 83.4% but after rising by .3% last month. Also, there was a big drop in the ‘job leavers’ category. This fell to 9.8% from 11.8% and that’s the least since May 2021. Of note too, the number of people who are working part time because they can’t find full time work rose by 125k people to the most since April 2019. Smoothing out the monthly data has the 3 month headline payroll average at 135k vs the 6 month average of 157k and the 12 month average of 144k.

2) ADP said there were just a net 37k private sector jobs created in May after a 60k person rise in April. That was well under the estimate of 114k. Small business not just reigned in their hiring, they shed workers on a net basis with companies with less than 50 workers losing 13k jobs. Also of note, large companies, those with more than 500 employees, let go a few thousand. So, the only area of job growth was the 49k person gain for medium sized businesses.

3) For the 2nd week in a row initial jobless claims popped above expectations. For the week ended May 31st they totaled 247k, 12 more than expected and follows 239k last week (revised down by 1k) . The 4 week average shifted up to 235k from 231k and that is the most since late October. Continuing claims were 1.904mm, about as forecasted and down 3k w/o/w but still around the highest since November 2021.

4) Challenger reported its monthly job cut/hire data and said May job cuts were up by 47% y/o/y. They said, “Tariffs, funding cuts, consumer spending, and overall economic pessimism are putting intense pressure on companies’ workforce. Companies are spending less, slowing hiring, and sending layoff notices.” Challenger said the ‘DOGE Impact’ “remains the leading reason for job cut announcements in 2025.” The second reason cited, “market and economic conditions” followed by “closings of stores, units, or plants.”

5) The May ISM services index fell to 49.9 from 51.6. This is the weakest print since June 2024. The Business Activity component fell to exactly 50 from 53.7 in April and 55.9 in March. In terms of industry breadth, 10 saw growth out of 18 surveyed vs 11 in April. Its peak this year was 14. Eight industries saw a contraction in their business versus 7 last month. ISM said, “May’s PMI level is not indicative of a severe contraction, but rather uncertainty that is being expressed broadly among ISM Service Business Survey panelists…Respondents continued to report difficulty in forecasting and planning due to longer-term tariff uncertainty and frequently cited efforts to delay or minimize ordering until impacts become clearer.”

6) After the rush to buy autos in March (17.7mm) and April (17.27mm) to save money ahead of the tariffs, May sales saw a cool down to 15.65mm. These are seasonally adjusted annualized rate figures. The estimate was 16mm. There was also less vehicles to choose from according to Wards Automotive. "The drop in inventory, which at the end of last month was down y/o/y for the first time in nearly three years, helped explain a 10% decline in incentive spending in May from April, as there was less pressure to move stock off dealer lots despite the sharp slowdown in demand. That dynamic likely continues not just in June, but into Q3, as most automakers do not currently appear anxious to raise production levels enough to fully replace declining stock levels."

7) From the Fed’s Beige Book on the economy: "Reports across the twelve Federal Reserve Districts indicate that economic activity has declined slightly since the previous report. Half of the Districts reported slight to moderate declines in activity, three Districts reported no change, and three Districts reported slight growth." Also, "On balance, the outlook remains slightly pessimistic and uncertain, unchanged relative to the previous report. However, a few District reports indicate the outlook has deteriorated while a few others indicate the outlook has improved."

8) The NY Fed released its survey of tariffs and how companies are responding. They said, "about three-quarters of businesses facing tariff induced cost increases in both the manufacturing and service sectors passed along at least some of these higher costs to their customers by raising prices. Almost a third of manufacturers and about 45% of service firms reported fully passing along all tariff-related cost increases, while 45% of manufacturers and a third of service firms said they passed along some but not all of the cost increase."

9) Container rates exploded higher this past week and are up now 5 weeks in a row in the rush to procure whatever is needed. The Shanghai to LA container price spiked 57% w/o/w, by $2,138 to $5,876. The Shanghai to NY journey will now cost you $7,164, up 39% w/o/w, by $1,992.

10) Elevated mortgage rates still, resulted in a 4.4% drop in weekly purchase applications while refi's were down by 3.5% w/o/w.

11) Steel and aluminum tariffs are now up to 50% a big cost challenge to users of these materials.

12) From Dollar General: "During our recent customer survey work, 25% of DG customers reported having less income than they did a year ago and nearly 60% of our core customers noted that they felt the need to sacrifice on necessities in the coming year. While our core customer remains financially constrained, we have seen increased trade in activity from both middle and higher income customers. Our data shows that new customers this year are making more trips and spending more with us compared to new customers from last year, while also allocating more of their spend to discretionary categories. We believe these behaviors suggest we are continuing to attract higher income customers who are looking to maximize value while still shopping for items they want and need."

13) From Lululemon: “my sense is that in the US, consumers remain cautious right now, and they are being very intentional about their buying decisions… we did see a decline in store traffic, particularly in the US as we moved from Q4 into Q1. We did see that moderate somewhat, but we did still for the first quarter see a lower traffic trend in stores relative to Q4. Conversion trends remained relatively consistent, a little bit of a decline y/o/y. And then also, we did see an uptick in terms of average dollars per transaction in the first quarter. And then in terms of how it's progressing April into May, we don't share specifics on Q2, but I would say nothing materially different."

14) From Brown Forman: "Now, turning to our fiscal 2026 outlook; we believe the operating environment will remain volatile and visibility low due to geopolitical uncertainties and global macroeconomic conditions, particularly with regard to the tariff environment. This environment will create sustained levels of consumer uncertainty, which we believe will lead to another year of below historical total distilled spirits trends. We continue to expect that the behavior of the consumer and the level of trade inventories will not change meaningfully during the 2026 fiscal year.” Generally their view on the consumer, "I still would argue that it is the consumer and their wallet just doesn't have as much money in it. You're right, they're spending money on things like vacations and lodging and other things like that. But then when it trickles down and they go to the grocery store, I think in some cases, spirits has fallen out of the basket a little bit, and that isn't obviously great."

15) From Thor Industries: "We expect the fourth quarter of our fiscal 2025 and the first quarter of our fiscal 2026 to be challenging. The current economic uncertainty has led to downward pressure on consumer confidence and has negatively impacted retail pull-through."

16) From PVH: "We are navigating a highly dynamic and uncertain macroeconomic environment that is impacting our industry, our consumers, and our business results."

17) From Campbell’s: "In the current dynamic macro environment, consumers are making thoughtful spending decisions, which is materializing in our categories. Consumers continue to cook at home and focus their spending on products that help them stretch their food budgets, and they are increasingly intentional about their discretionary snack purchases. These behaviors supported growth in our meals & beverage categories and increased headwinds in our snaking categories."

18) From Kenvue: "we definitely see that the consumer continues to be under pressure regardless of the geography for slightly different reasons. But I would say consumers are under pressure. Consumers are worried when you look at belief in the future, and we see it in how people behave in store."

19) From Broadcom: Saw more muted growth from its non-AI semi business, "In Q2, broadband, enterprise networking, and server storage revenues were up sequentially. However, industrial was down, and as expected, wireless was also down due to seasonality."

20) From Hewlett Packard Enterprises: "In the second quarter, we saw a very dynamic macro and trade policy environment. The IT industry continues to navigate significant uncertainty, brought on by tariffs, the AI diffusion policy withdrawal, and broad macroeconomic concerns. While this led to uneven demand during the quarter, we did not benefit from significant order pull-ins. We ended Q2 with a stronger pipeline compared to Q1."

21) Vietnam's May exports were higher by 17% y/o/y, above the estimate of 15.5% and after a 19.8% y/o/y jump in April.

22) The May China private sector Caixin manufacturing index weakened to 48.3 from 50.4 and below expectations of 50.7. Of note, "The contraction in supply and demand was attributed to sluggish external demand, which fell for a 2nd straight month. The gauge for new export orders dropped to the lowest level since July 2023." Also, employment continued to decline and "prices remained at a low level as supply and demand weakened. Input costs declined for the third straight month on falling prices of energy and chemical raw materials. Sales prices were also subdued as businesses sought to lower prices to remain competitive, resulting in the corresponding gauge contracting in May for the sixth straight month."

23) The May Singapore PMI fell to 51.5 from 52.8 while Hong Kong's improved to 49 from 48.3 but still below 50.

24) Most other manufacturing PMIs remain below 50: Taiwan 48.6 vs 47.8, South Korea 47.7 vs 47.5, Vietnam 49.8 vs 45.6, Indonesia 47.4 vs 46.7, Philippines 50.1 vs 53 and India the bright spot at 57.6 vs 58.2. Japan's stayed below 50 after the revision at 49.4 while Australia's was a touch above 50.

25) The Eurozone May manufacturing index was left unrevised at 49.4 while the UK saw a lift to 46.4 from the initial print but still remaining well below 50.

26) The ECB cut rates to 2% as expected but keeping real rates still at zero.