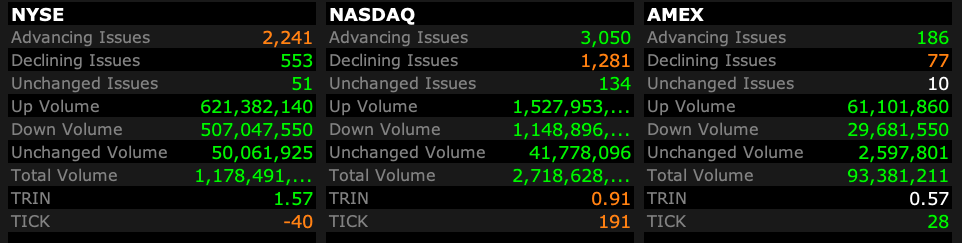

Friday's Closing Market Stats

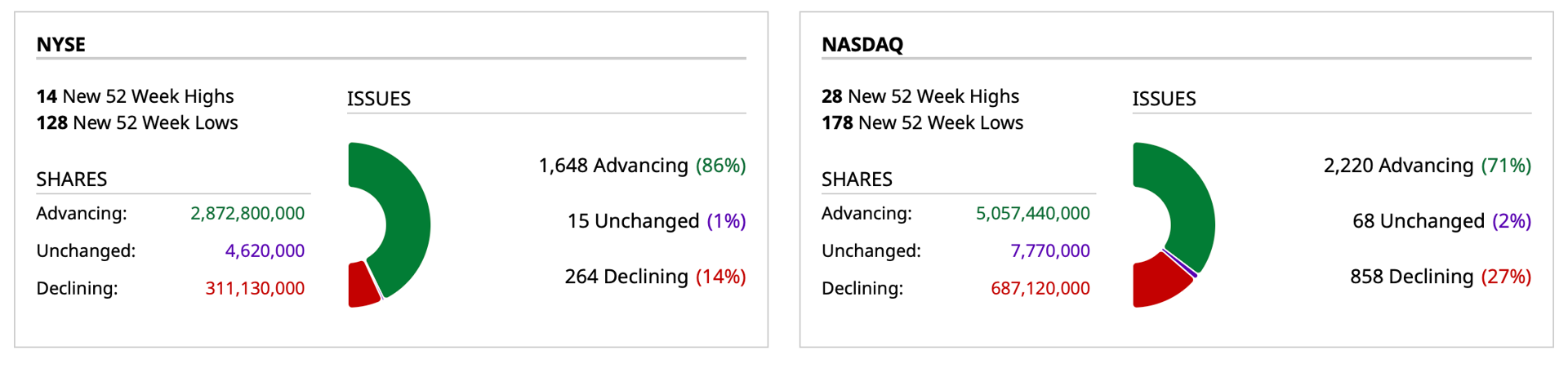

Breadth

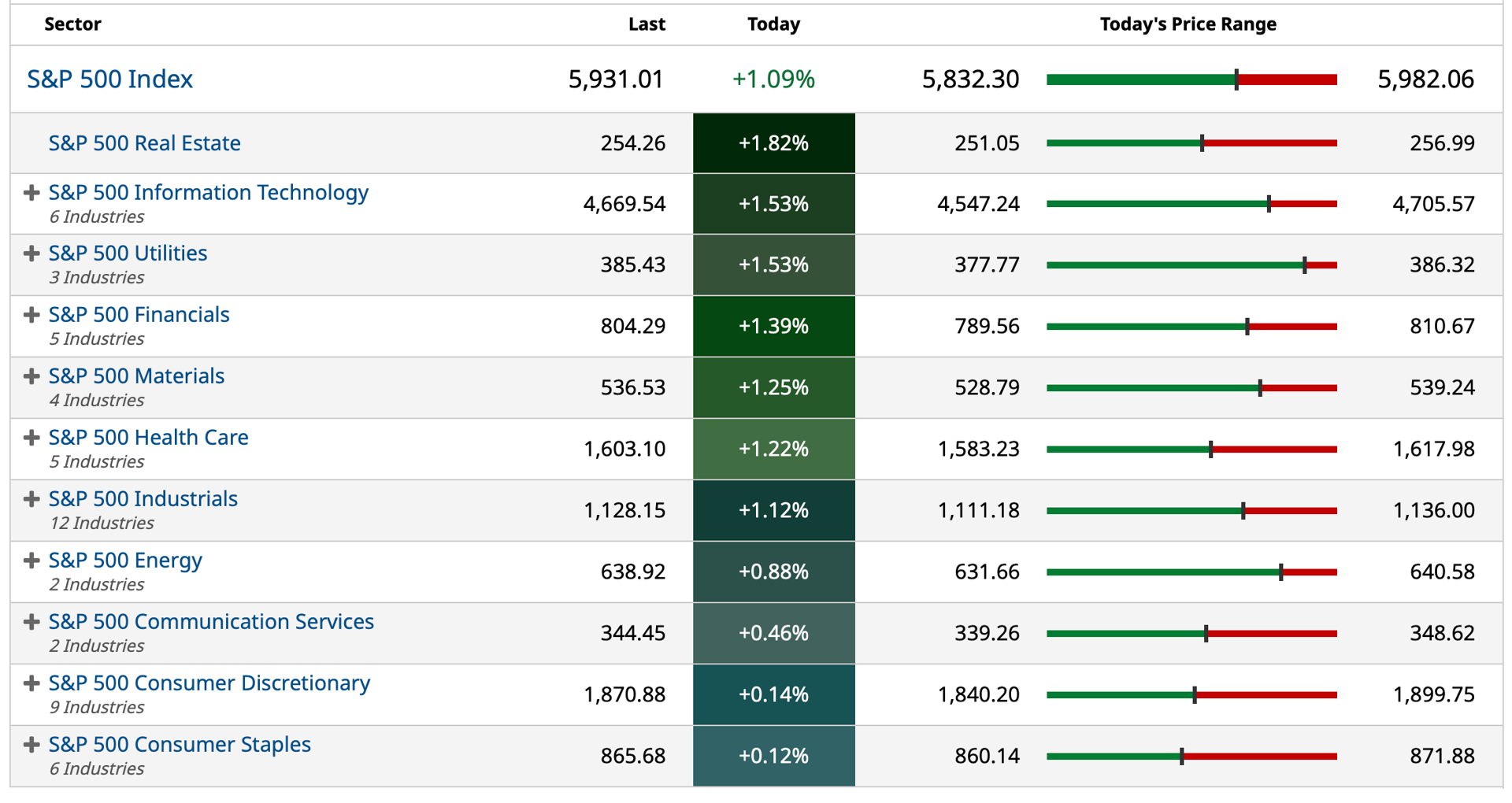

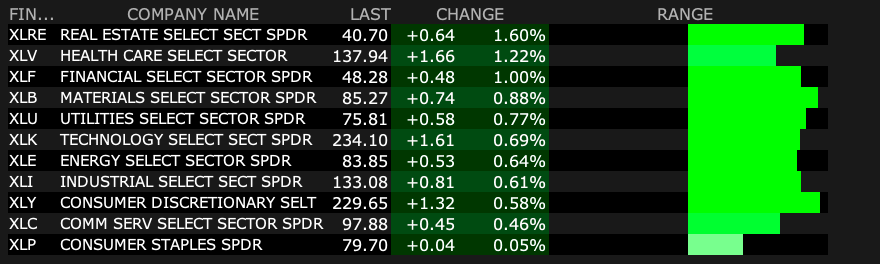

S&P Sectors

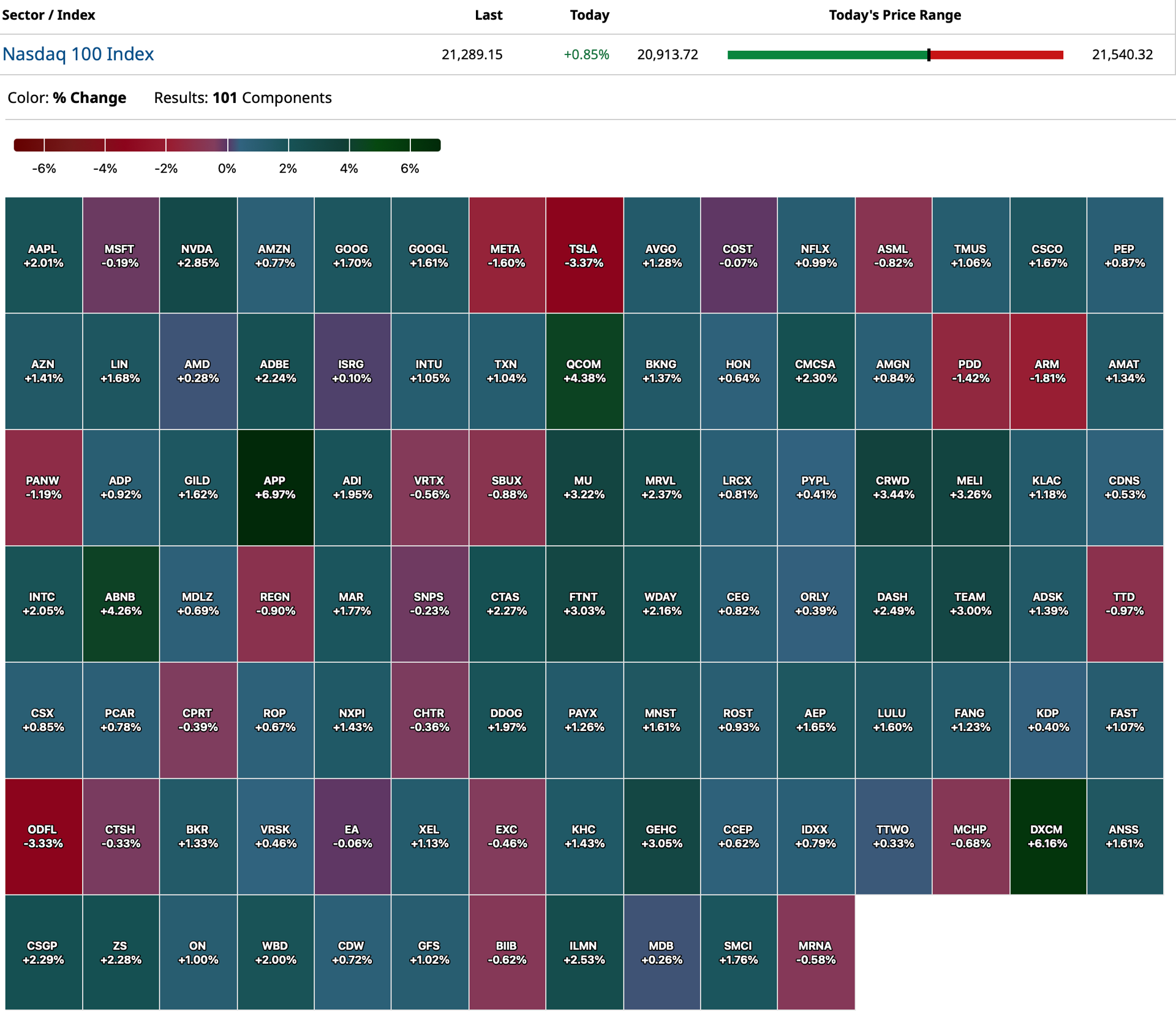

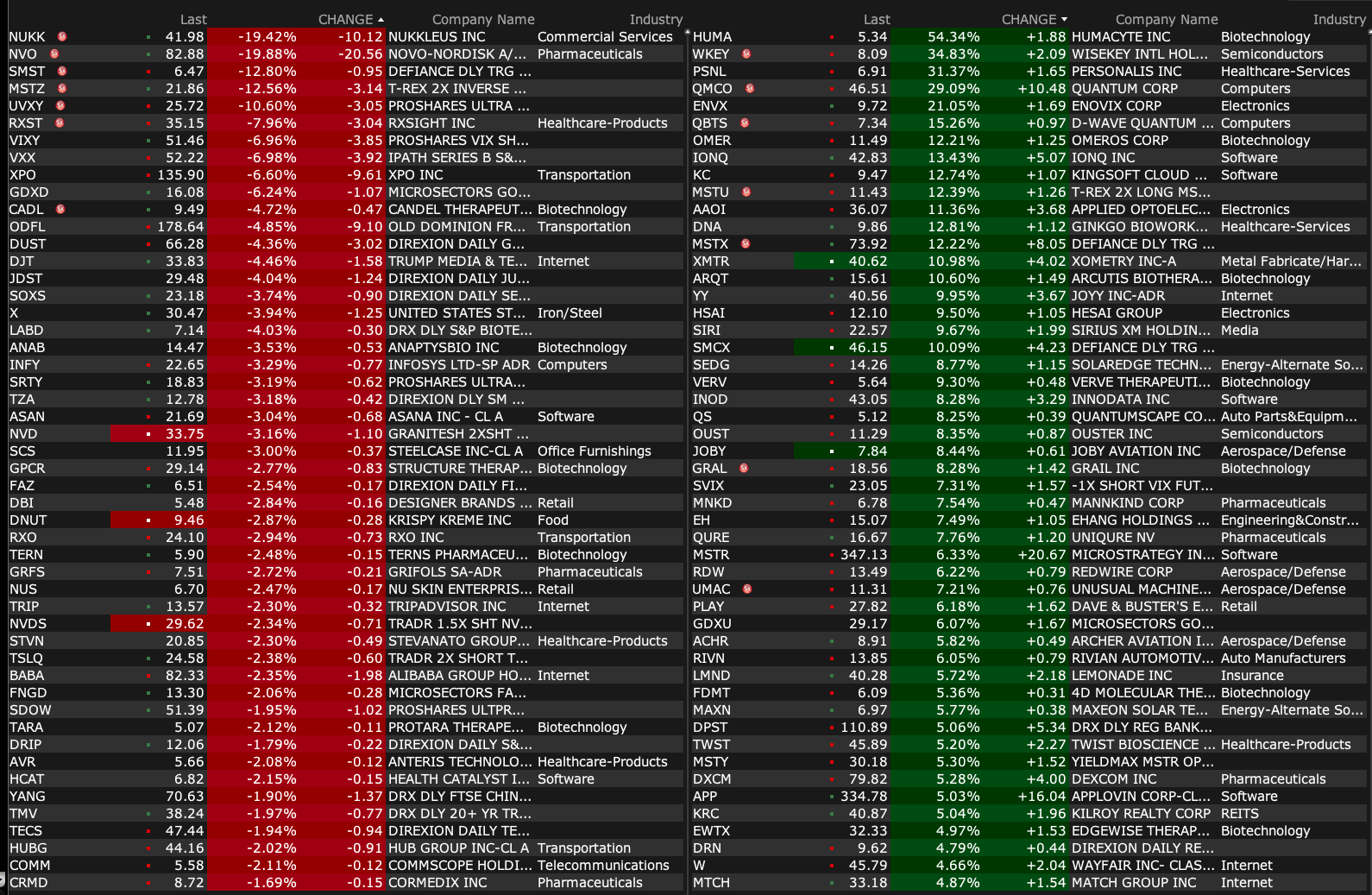

Nasdaq 100 Heat Map

BY Doug Kass · Dec 20, 2024, 4:50 PM EST

BY Doug Kass · Dec 20, 2024, 4:50 PM EST

$11 billion to sell market on close!

BY Doug Kass · Dec 20, 2024, 3:56 PM EST

Into expiration, what will be the last program standing?

Thus far -40 handles taken from the top.

BY Doug Kass · Dec 20, 2024, 3:44 PM EST

Wolf Street howls about what the Fed said.

BY Doug Kass · Dec 20, 2024, 3:41 PM EST

From Peter Boockvar:

Positives

1)Anyone who is borrowing money or has a loan coming due celebrates the Federal Reserve’s rate cut but mitigated by where on the yield curve one is borrowing against as long rates rise again in response. One yr ago when the fed funds rate was at 5.25-5.50%, the 10 yr yield was at 3.90% vs today’s fed funds rate of 4.25-4.50% and a 10 yr yield of 4.50%.

2)The December S&P Global PMI for the US gained 1.7 pts m/o/m to 56.6 with all the strength coming from services. This component rose to 58.5 from 56.1 while manufacturing remains under continued pressure at 48.3 vs 49.7 in November.

3)The final December UoM consumer confidence was 74, up from 71.8 in November. That’s the best since April but with a wide differential in opinion between Republicans and Democrats. One yr inflation expectations rose to 2.8% from 2.6% but the 5-10 yr guess fell to 3% from 3.2%.

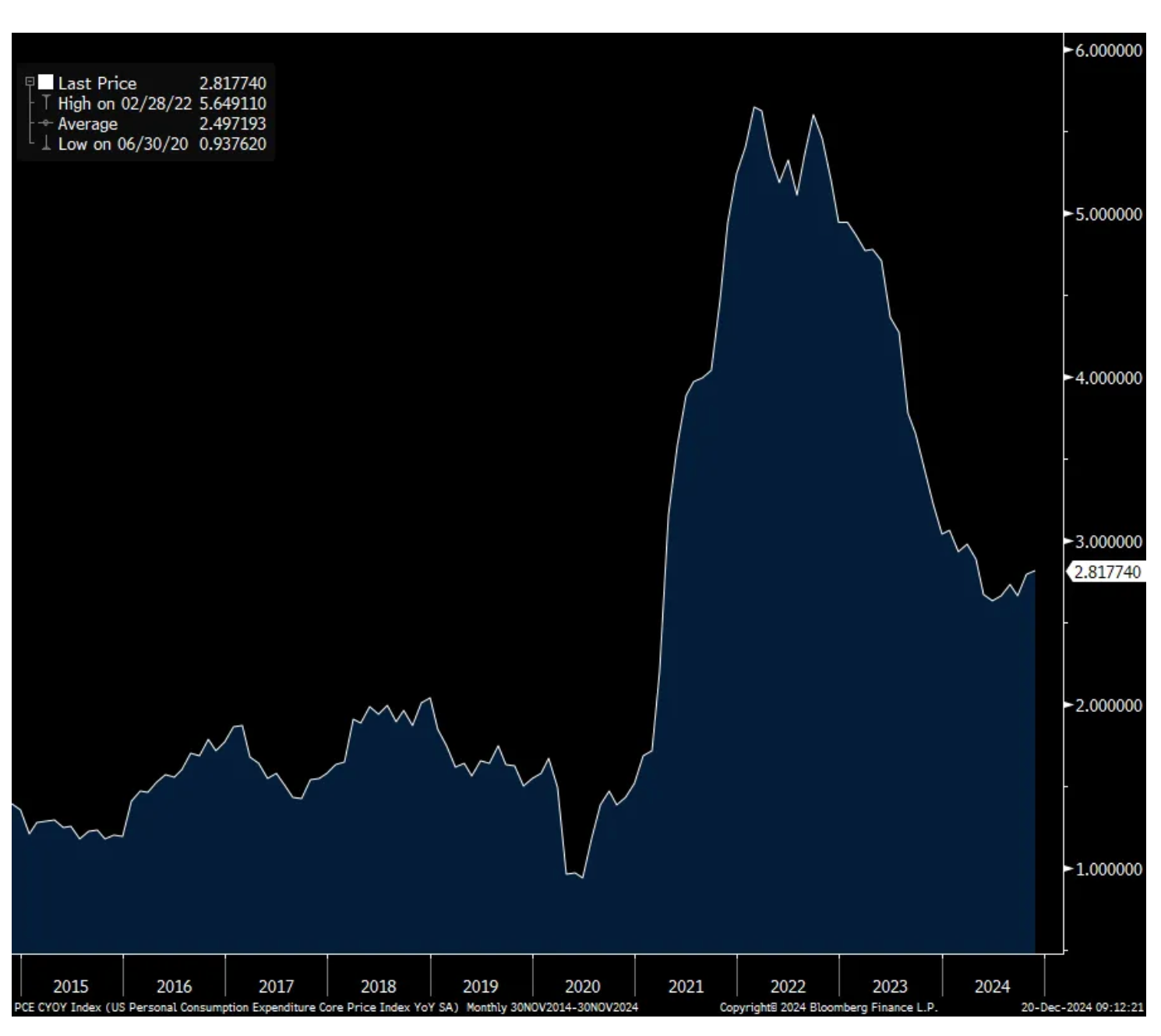

4)The PCE November inflation rate rose one tenth for headline and core with both one tenth below expectations. The headline gains were 2.4% and 2.8% for headline and core vs 2.3% and 2.8% in the month before. Energy prices rose .2% m/o/m but fell 4% y/o/y while food was also up .2% m/o/m and 1.4% y/o/y. Goods deflation continued, lower by .4% y/o/y, offset by services inflation of 3.8%.

5)When including the slight October revision, personal income in November was in line with the estimate. Specifically private sector wage/salaries grew by .6% m/o/m and 5.7% y/o/y (the quickest since May).

6)Core retail sales in November rose .4% m/o/m as expected after a one tenth decline in October. Not included in the core print was the 2.6% m/o/m jump in auto sales/parts after a 1.8% rise in October. Building materials, also outside the core read, was up .4% m/o/m and 2.5% y/o/y.

7)Q3 GDP was revised up to 3.1% from 2.8% and vs the estimate of no change. Old news though.

8)After the surprising pop higher last week in initial jobless claims to 242k, they fell back to 220k this week, 10k less than expected. Smoothing this out puts the 4 week average to 226k from 224k. Continuing claims was 1.874mm, little changed with the week before but below the estimate of 1.892mm.

9)Purchase applications rose 1.4% w/o/w after falling by 4.1% last week.

10)From CarMax: It’s good for them but sign of the times, "I think consumers are still pinched from an inflationary standpoint, so they're looking for alternatives. And used cars, whether it's a two year old used car or a 14 year old used car, I think that helps the industry as well."

11)From Darden: On their overall consumer research, it "shows that consumer sentiment is trending positive, and there's a little bit of a feeling of optimism out there by the belief the labor market will improve…In contrast to previous quarters, we're seeing growth in visits from our guests making between $50,000 and $100,000 a year, which is really more of our Casual Dining brands. We're not seeing as much of an increase in visits yet on the consumers that are above that...it appears that consumers who were splurging on Fine Dining, basically those who were making less than $150,000, have continued to pull back. So, it's impacting Fine Dining a little bit. The kind of more average income consumer is starting to feel a little bit better."

12)From Accenture: "GenAI continues to be a catalyst for reinvention across the enterprise, and building out the data foundation necessary to capitalize on AI is an increasing part of that growth. Themes around achieving both costs efficiencies and growth continue across the demand we're seeing."

13)With inflation still elevated, the BoE kept rates unchanged as did the Norges Bank. The Riksbank followed the ECB with a 25 bps cut. Thailand, Taiwan and Indonesia left rates unchanged. The Philippines bank cut rates by 25 bps.

14)Japan's exports in November lifted by 3.8% y/o/y, above the estimate of 2.5%, boosted by the weak yen as volumes actually fell by .1% y/o/y.

15)Japan's December composite PMI index rose to 50.8 from 50.1 with services still leading the growth with this component at 51.4 from 50.5 vs manufacturing at 49.5 vs 49. India remains the standout with its composite index at 60.7 vs 58.6 in November with services at 60.8 and manufacturing at 57.4, both higher m/o/m.

16)Singapore said its November non-oil exports jumped by 14.7% m/o/m, well above the estimate of up 9.2% and was up 3.4% y/o/y vs the forecast of down 1%. The rise was led by a 23.2% y/o/y jump in electronics exports. The export strength was to India, Hong Kong, Taiwan, Korea and Malaysia. Exports to the US fell by 19% and to the EU by 1.2%.

17)China said in November the decline in home prices has slowed. For new homes, prices fell .20% m/o/m, the smallest amount since June 2023. For existing homes, prices fell .35% m/o/m, the least since May 2023.

18)Wages ex bonus in the UK for the 3 months ended October rose by 5.2% y/o/y, above the estimate of 5% and a 4 month high. This was part of their full jobs report where 173k jobs were added vs the estimate of just 5k. Also, there was no change in November jobless claims.

19)In the Eurozone December PMI, services rebounded to back above 50 at 51.4 from 49.5 and above the estimate of no change. Manufacturing remained though in the doldrums at 45.2, unchanged with November.

20)The UK December PMI held steady at 50.5 with also services well outperforming manufacturing. The services component was 51.4 vs 50.8, offsetting manufacturing at 47.3 vs 48.

Negatives

1)Very easy financial conditions did not warrant an interest rate cut and neither did the confusing confluence of conflicting economic data but the market tightened financial conditions for them instead.

2)Personal spending in November was a touch light with a .4% m/o/m increase, one tenth below expectations and October was revised down by one tenth to a .3% gain. Spending on durable goods drove the gain, likely in part to a pick up in auto sales, helped by the post hurricane recovery. There could be a slight tweak down in GDP forecasts as a result.

3)Combining income and spending puts the savings rate at 4.4% vs 4.5% in October but continues to hover around the lowest since 2008 not including the Covid influence.

4)The December Philly manufacturing index remained weak, falling to -16.4 from -5.5 and vs an expected rise to +2.4. After the post election spike in the 6 month outlook in November to 56.6 from 36.7 in October, it fell back to 30.7 which is about the 6 month average. Capital spending plans moderated.

5)After the initial post election November spike in the NY manufacturing index to +31.2 from -11.9 in October, it fell back to reality in December at +.2. The six month outlook was 24.6 vs 33.2 in November and 38.7 in October and compares with the six month average of 29.3 and is at a 4 month low. Capital spending plans jumped in October and November but fell back by 2 pts to 11.6 but above the half yr average of 7.4.

6)On shipping costs ahead of the holidays and likely tariffs, they broke its downtrend with the Shanghai to LA route jumping by almost $1,000 w/o/w to $4,499. The trip to NY rose $875 w/o/w to $6,074.

7)The average rate per mile for a truck rose to the highest level since February, up 9% y/o/y.

8)Housing starts in November fell to 1.289mm, 55k less than expected and down from 1.312mm in October. Multi family starts fell to just 278k, the 2nd lowest amount, not including Covid, since September 2013. Single family starts totaled 1.011mm from 950mm in October (which could have been subdued because of the storms) and vs 1.045mm in September. With respect to permits, the precursor to starts, they rebounded to 533k from 448k for multi family but were flat for single family at 972k.

9)Refi’s fell 2.6% w/o/w after a 6.1% rise last week.

10)Manufacturing production rose .2% m/o/m vs the estimate of up .5% and October was revised down by 2 tenths to a drop of .7%. Auto production rebounded by 3.5% after a 5.4% drop in October but manufacturing production ex autos fell for a 3rd straight month and is down .7% y/o/y. Mining and utility output both fell. Capacity utilization for manufacturing stands at just 76% which is below the 10 yr average of 77% and is just off the lowest level since March 2017 ex Covid.

11)The December NAHB home builder sentiment index was unchanged m/o/m at 46. The estimate was 47 and thus also remaining below 50. Expectations though are for a notable improvement as this component rose again to 66 from 63 and vs 57 in October pre-election. The Present Situation held at 48. The drag remains really in the Prospective Buyers Traffic component which was 31 vs 32 in November and 19 pts below the breakeven. The NAHB said, “While builders are expressing concerns that high interest rates, elevated construction costs and a lack of buildable lots continue to act as headwinds, they are also anticipating future regulatory relief in the aftermath of the election,” said NAHB Chairman Carl Harris, a custom home builder from Wichita, Kan. “This is reflected in the fact that future sales expectations have increased to a nearly three-year high.”

12)From FedEx: The CEO mentioned "the challenging demand environment...Similar to last quarter, we experienced weakness in the industrial economy which negatively affected our B2B volumes, particularly in the US domestic package and the LTL markets. Continued market pressure coupled with difficult y/o/y comparisons weighed on our freight segment in the second quarter."

13)From Nike: "What I've seen is traffic in NIKE Direct, digital and physical, has softened because we've lacked newness in product and we're not delivering inspiring stories. The result is we've become far too promotional. We've moved to a push mode.” Sales fell 9% on a currency neutral basis, "with traffic and retail sales across the marketplace falling below our expectations, especially in September and October. In November, we saw momentum build, with digital and physical traffic inflecting positive, especially around the quarter's biggest consumer moments…inventory levels are higher than we would like, especially given recent sales trends on NIKE Direct."

14)From Lamb Weston: "Our second quarter performance was below our expectations and not what we aim to achieve at Lamb Weston...We expect a challenging operating environment will persist in the near term as weak restaurant traffic trends and additional capacity expansions announced by our competitors since our Investor Day last year add to the current imbalance in global industry supply and demand, especially outside North America."

15)From Conagra: A margin squeeze, "there's inflation in cocoa and sweeteners, and that's very narrow in our portfolio, and we will be pricing to offset that, but the bigger driver for us has been protein. It's meats, eggs, things like that, and we did anticipate that there would be inflation in the 2nd half, but we anticipated that level of inflation will be lower. And we still anticipate that those peak protein costs are going to come down pretty much across the board, but there's a bit of a deferral for that."

16)From General Mills: "I think we've learned a couple of things and so we'll start with the consumer. I mean it's clear that from the beginning of the year to now, we've seen more prolonged value seeking behavior than we anticipated back in June and that manifests itself in a couple of ways. One is that the consumer is eating more at home, which is good. So you see our categories are growing...And that's because eating away from home is about 4 times more expensive than eating at home. So we've seen this increased value behavior."

17)From Accenture: "Starting with the demand environment, we saw more of the same. Our clients are focused on reinvention, which means large scale transformations. We do not currently see an improvement in overall spending by our clients, particularly on smaller deals."

18)From Lennar: "In the course of our fourth quarter, the housing market that appeared to be improving as the Fed cut short term interest rates, proved to be far more challenging as mortgage rates rose almost 100 bps through the quarter. Even while demand remained strong, and the chronic supply shortage continued to drive the market, our results were driven by affordability limitations from higher interest rates. Accordingly, in our fourth quarter, sales lagged expectations as interest rates climbed and our new orders fell short of expectations to 16,895 homes vs the low end of our guidance of 19,000 homes. Consistent with our strategy of matching sales pace with production, we adjusted sales price, incentives, and margin in order to re-ignite sales and actively manage inventory levels."

19)The BoJ sits on its hands again at .25% just as inflation prints 2%+ for the 32nd straight month.

20)China retail sales in November were softer than expected, up 3% y/o/y instead of rising 5% as expected and after a 4.8% rise in October but Singles Day this year was in October vs the usual November time period so that likely pulled forward some sales. Industrial production grew by 5.4% y/o/y as forecasted and vs 5.3% in the month before. Not surprisingly, property investment remained soft, down 10.4% ytd y/o/y.

21)Brazil has lost control of the Real as markets call out excessive government spending.

22)Approaching the holidays, November retail sales ex fuel in the UK rose .3% m/o/m but after a .9% drop in October and that was 2 tenths below expectations. This though does not include Black Friday there as it occurred at the end of the month. The ONS said "For the first time in three months, there was a boost for food store sales, particularly supermarkets. It was also a good month for household goods retailers, most notably furniture shops. Clothing store sales dipped sharply once again, as retailers reported tough trading conditions."

23)Headline CPI rose 2.6% y/o/y in the UK as expected but up from 2.3% in October. Core CPI was higher by 3.5% vs 3.3% in the month before but one tenth less than anticipated. Services inflation in particular was up by 5%. Wholesale prices, both output and input charges, were as expected.

24)French business confidence in December fell 2 pts to 94, matching the lowest since February 2021.

25)The German December IFO business confidence index fell to 84.7 from 85.6. That is below the expectation of 85.5 and the weakest level since June 2009 not including Covid though the components were mixed. The Current Assessment ticked up to 85.1 from 84.3 but Expectations fell to just 84.4 from 87. The bottom line from IFO, "The weakness of the German economy has become chronic."

26)Australia's PMI index slipped a touch below 50 at 49.9 from 50.2 with services at 50.4 vs 50.5 and manufacturing at 48.2 from 49.4.

BY Doug Kass · Dec 20, 2024, 2:50 PM EST

From MacroStrategy's Andrew Lees:

AI’s scaling has been slowing as it approaches the limits of the parent universe, of tangible capital and information embedded within it, from which to learn.

Because information is physical, artificial intelligence cannot grow exponentially cleverer without the tangible capital and information embedded in it, first being created. For AI to grow exponentially, therefore, exponentially more tangible capital must be created and energy found to deliver that growth. That is not happening. AI is not creating the upstream capital for its own demand, and without that capital, its ability to learn, and therefore offer a service, is getting harder, and more expensive for the economy to bear.

This gradual realization by the tech sector that its vision of exponential growth will be limited by the need for physical capital and energy comes at a time when the supply of that capital is stagnating, and valuations are at an extreme.

BY Doug Kass · Dec 20, 2024, 2:30 PM EST

I took a few dollars out of the Microsoft MSFT trading short rental.

Now flat the name.

BY Doug Kass · Dec 20, 2024, 2:05 PM EST

Out of the balance of my small SPY/QQQ short calls position — for a quick and profitable trade.

S&P cash now +77 handles, or nearly -30 handles lower than when put on the trading rental.

BY Doug Kass · Dec 20, 2024, 2:00 PM EST

S&P cash is now +80 handles, or -26 handles from where I put on my short Index calls.

I will take off half of the position for a $2+ profit.

Just trading opportunistically and unemotionally.

BY Doug Kass · Dec 20, 2024, 1:39 PM EST

Up from $428 early this morning, I took a very short-term trading short rental in Microsoft MSFT at $442.37.

BY Doug Kass · Dec 20, 2024, 1:12 PM EST

The only financial I have shorted today is AXP.

I am offering stock above the market in 3-5 others — will report back when filled.

I cancelled my medical appointment for this afternoon, so I will be around!

BY Doug Kass · Dec 20, 2024, 1:05 PM EST

I added to AXP at $302.10 and AAPL at $253.72 shorts.

BY Doug Kass · Dec 20, 2024, 12:52 PM EST

With S&P cash +106 handles I have started to short in-the-money SPY/QQQ calls for January.

Starting small.

BY Doug Kass · Dec 20, 2024, 12:42 PM EST

I will be out of the office between 1:30 and 2:30 at a routine medical appointment.

BY Doug Kass · Dec 20, 2024, 12:30 PM EST

From Peter Boockvar:

The PCE November inflation rate rose one tenth for headline and core with both one tenth below expectations but typically always comes around expectations vs CPI where there could be more deviations. AGAIN, the biggest component of PCE is healthcare and paid for by 3rd party payers like Medicare, Medicaid and employer paid insurance companies as opposed to out of pocket medical expenses measured in CPI.

The headline gains were 2.4% and 2.8% for headline and core vs 2.3% and 2.8% in the month before. Energy prices rose .2% m/o/m but fell 4% y/o/y while food was also up .2% m/o/m and 1.4% y/o/y. Goods deflation continued, lower by .4% y/o/y, offset by services inflation of 3.8%.

Bottom line, because the Fed pays more attention to PCE than CPI and with the 50 bps difference between the core rate on each with the former about the latter, the Fed can theoretically cut 50 bps more than they would if the PCE didn’t exist as a calculation.

When including the slight October revision, personal income was in line with the estimate. Specifically private sector wage/salaries grew by .6% m/o/m and 5.7% y/o/y (the quickest since May).

Spending was a touch light with a .4% m/o/m increase, one tenth below expectations and October was revised down by one tenth to a .3% gain. Spending on durable goods drove the gain, likely in part to a pick up in auto sales, helped by the post hurricane recovery. There could be a slight tweak down in GDP forecasts as a result.

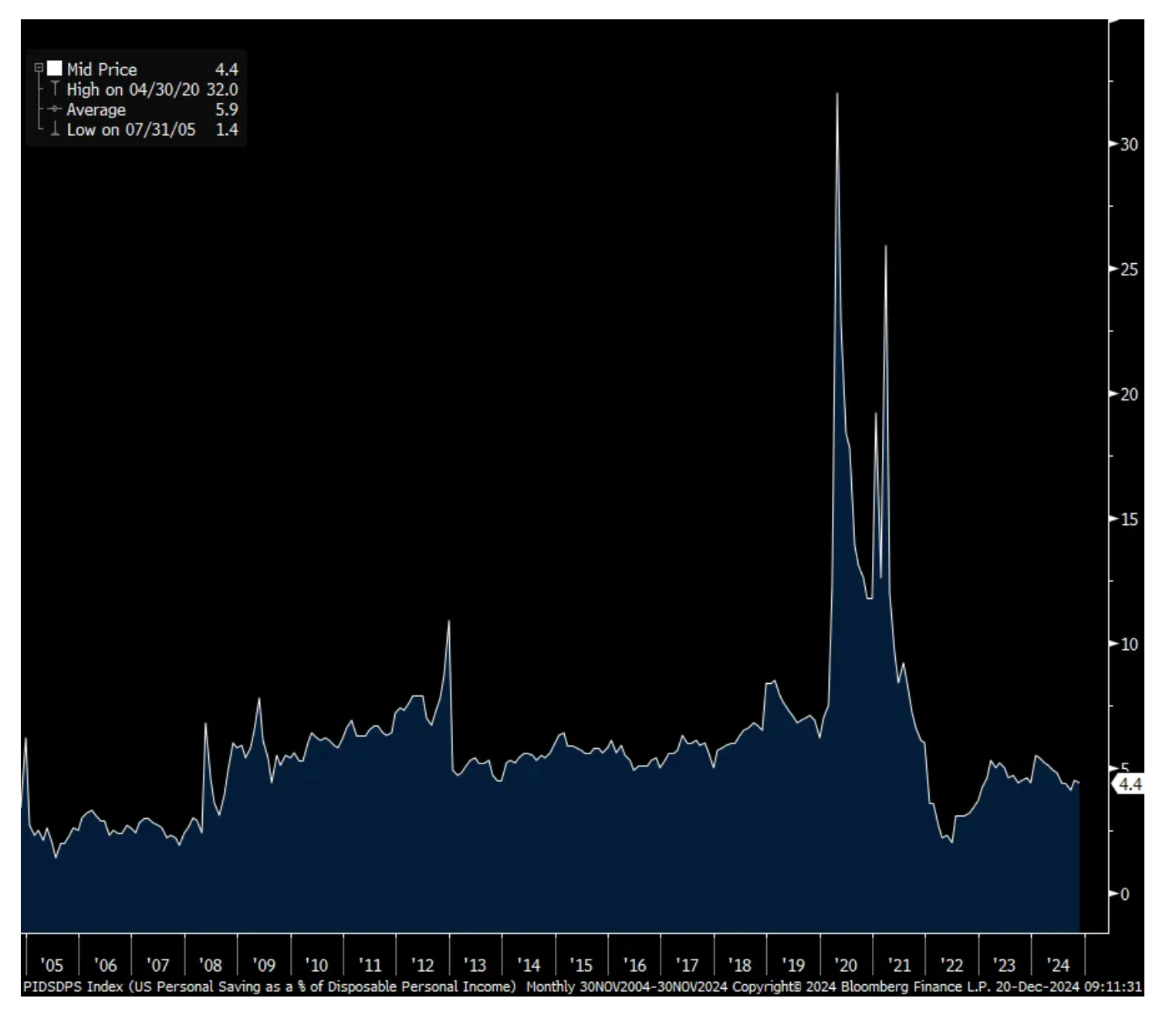

Combining income and spending puts the savings rate at 4.4% vs 4.5% in October but continues to hover around the lowest since 2008 not including the Covid influence.

Bottom line, bonds continued to rally post the data with the slightly lighter inflation stats and the miss in spending. The 2 yr is back under 4.30% and the 10 yr is below 4.50%. Rate cut odds of two more in 2025 is up to 72% vs 46% as of yesterday’s close.

Finally, Cleveland Fed president Beth Hammack gave her reasoning for not wanting to cut on Wednesday with her being the lone dissent. “Based on my estimate that monetary policy is not far from a neutral stance, I prefer to hold policy steady until we see further evidence that inflation is resuming its path to our 2% objective.”

Core PCE y/o/y

Savings rates

BY Doug Kass · Dec 20, 2024, 12:00 PM EST

Scott Galloway's No Mercy/No Malice: "People Are the New Brands"

BY Doug Kass · Dec 20, 2024, 11:58 AM EST

I'm adding to my Walmart WMT short above $93.

BY Doug Kass · Dec 20, 2024, 11:25 AM EST

At 10:35 a.m.:

BY Doug Kass · Dec 20, 2024, 11:15 AM EST

I'm adding to my Nvidia NVDA short at $133.32.

BY Doug Kass · Dec 20, 2024, 11:05 AM EST

As Boeing BA continues to surge, I'm down to tagends.

BY Doug Kass · Dec 20, 2024, 10:58 AM EST

I moved to medium-sized short Apple AAPL above $250.

BY Doug Kass · Dec 20, 2024, 10:52 AM EST

I am starting to re-short the financials that I covered.

BY Doug Kass · Dec 20, 2024, 10:45 AM EST

I added to my Apple AAPL short at $249.08.

BY Doug Kass · Dec 20, 2024, 10:37 AM EST

Buying JOE under $44 (down one third off high, but no catalyst) and picking up more ELAN below $11.75.

BY Doug Kass · Dec 20, 2024, 9:56 AM EST

Walmart WMT short starting to work.

BY Doug Kass · Dec 20, 2024, 9:53 AM EST

Subscriber Comment of the Day (And My Response)

Asaxelrod

41 minutes ago

Doug, enjoy your daily and though I don't regard TL's recurring bullishness with high regard, I know you sometimes post from Hedgeye who I do respect because of their process. They are positive, at least short-term, on financials and industrials in the New Year. Know you've covered your financial shorts. Curious if you agree with their early 2025 call, esp financials which I know is within your "power alley." HNY and TIA.

DK

Dougie Kass

STAFF

Just Now

I value Hedgeye's rigor and process but I currently disagree with Hedgeye's short term and positive view on the markets and financials...

Many of my fundamental concerns (growing policy (fiscal and monetary) risks, sticky inflation, slowing economic growth and rising interest (higher for longer)) are finally beginning to be accepted by investors -- at a point in time in which valuations are elevated and consensus corporate profit estimates seem too optimistic.

I plan to reshort the financials on any rally...

BY Doug Kass · Dec 20, 2024, 9:35 AM EST

-HUMA +61% (announces FDA Approval of SYMVESS (acellular tissue engineered vessel-tyod) for the Treatment of Extremity Vascular Trauma)

-AEMD +38% (notes miniature version of its investigational medical device Aethlon Hemopurifier device removed 99% of H5N1 following 6 hours of treatment)

-FRSX +18% (joins forces with SoftBank and Japanese Automaker to Advance Cellular V2X Technology for Enhanced Road Safety)

-FREY +16% (BTIG Raised FREY to Buy from Neutral, price target: $4)

-AVO +12% (earnings, guidance)

-HSCS +9.6% (files to withdraw S-1 registration statement originally filed Jun 7th, 2023)

-FDX +8.0% (earnings, guidance)

-LLY +6.9% (Tier1 analysts: Weaker CagriSema data is also likely to increase concerns into LLY Orforglipron PIII data in mid-2025)

-MTEM -49% (announces Notice of Delisting and Failure to Satisfy Continued Listing Rules)

-GALT -44% (announces Top-Line Results of NAVIGATE Clinical Trial Evaluating Belapectin in Patients with Cirrhotic Portal Hypertension Caused by MASH; while there was a favorable trend for incidence of varices in the primary end point intent-to-treat population, belapectin did not achieve statistical significance)

-APLM -31% (announces Top-line Results for Phase 3 Bridging Trial of Uproleselan in China in Patients with Relapsed or Refractory Acute Myeloid Leukemia; Trial did not demonstrate favorable benefit for uproleselan)

-BPTH -26% (announces preclinical testing of BP1001-A as a potential treatment for obesity in Type 2 diabetes)

-MOBX -23% (earnings)

-NVO -21% (weight loss drug trial misses expectations)

-ZCAR -19% (profit-taking)

-ARQQ -12% (downside momentum)

-MESO -11% (downside momentum)

-TPET -9.5% (acquiring producing oil and gas assets in prolific heavy oil region of Saskatchewan, Canada)

-SCHL -8.6% (earnings, guidance)

-NKE -6.2% (earnings)

-X -6.2% (guidance)

-MODD -5.6% (announces Licensing and Partnership Agreement with Nudge BG)

-WGO -3.9% (earnings, guidance)

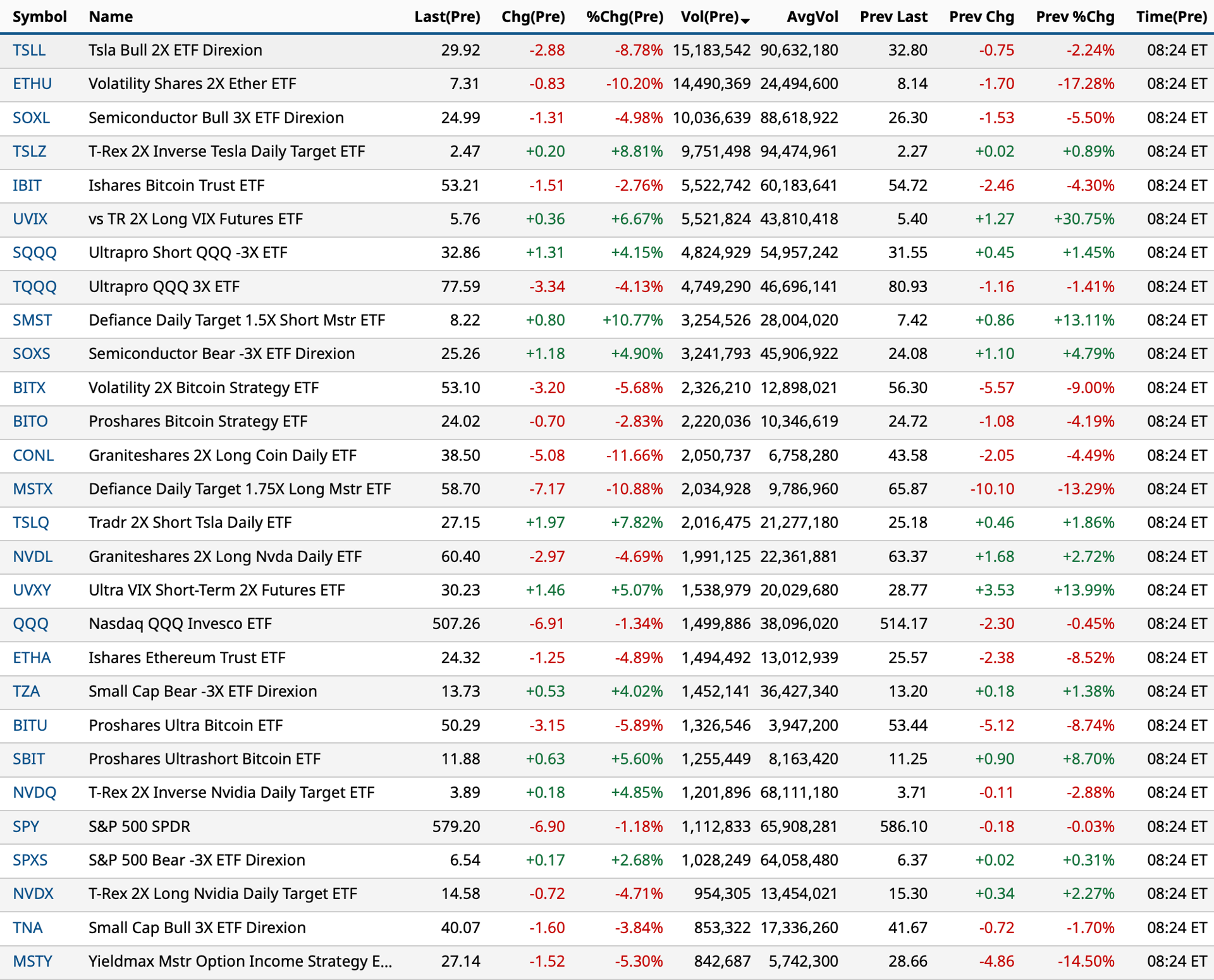

BY Doug Kass · Dec 20, 2024, 9:18 AM EST

Charts from 8:24 a.m. ET:

BY Doug Kass · Dec 20, 2024, 9:09 AM EST

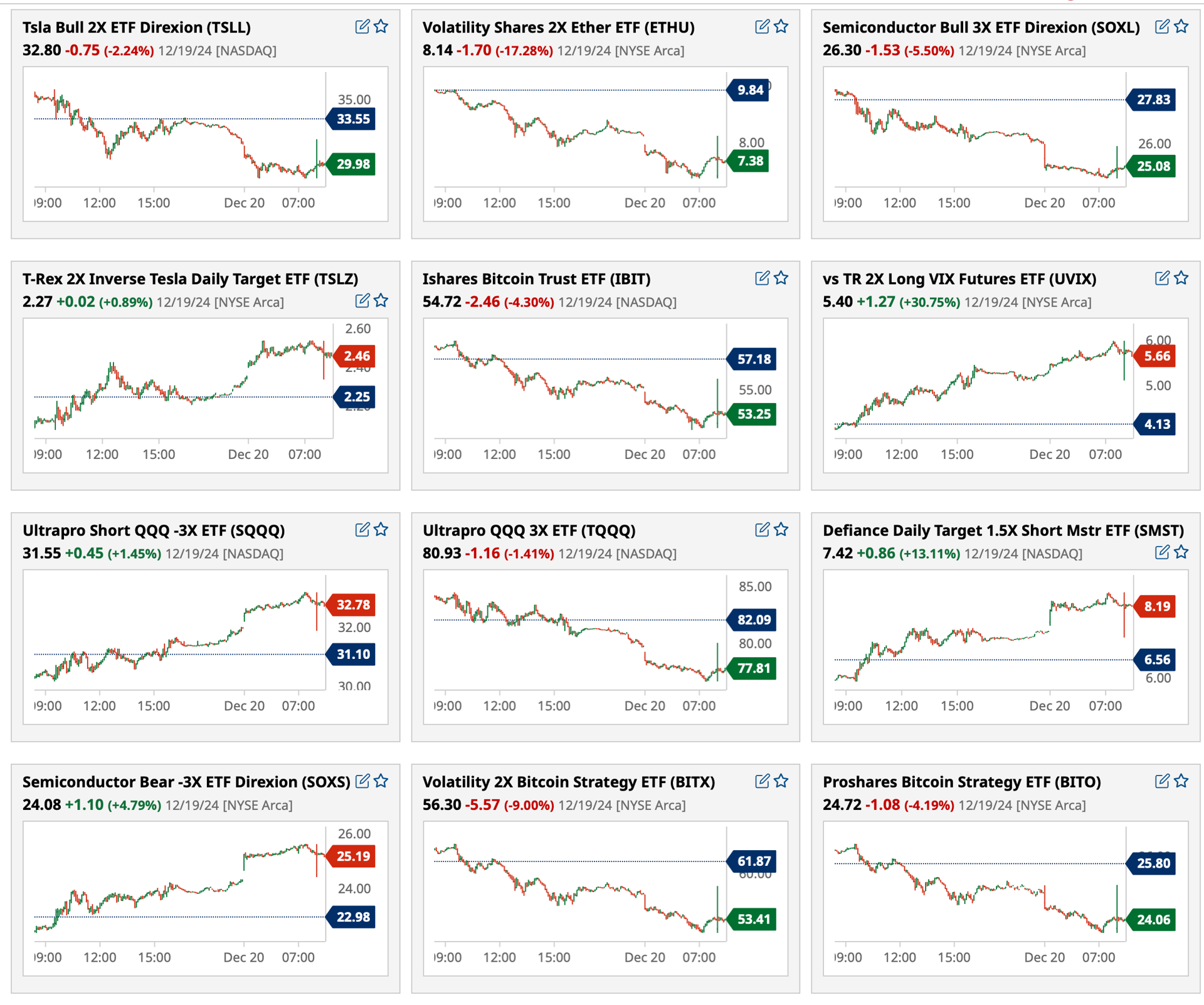

Chart from 8:43 a.m. ET:

BY Doug Kass · Dec 20, 2024, 8:58 AM EST

From Peter Boockvar:

Today will be my last day of writing for the year as I head off on a family adventure. I want to express my gratitude to my readers for taking out the time each day/week to read what I find important and have to say. Whatever holiday you celebrate I wish you a special time with your family and friends and I'll 'see' you on January 2nd.

One thing on the government shutdown possibility, I've been doing this long enough not to care because a deal always gets done and if the government does shut down for a short period of time, I guarantee that it will eventually reopen.

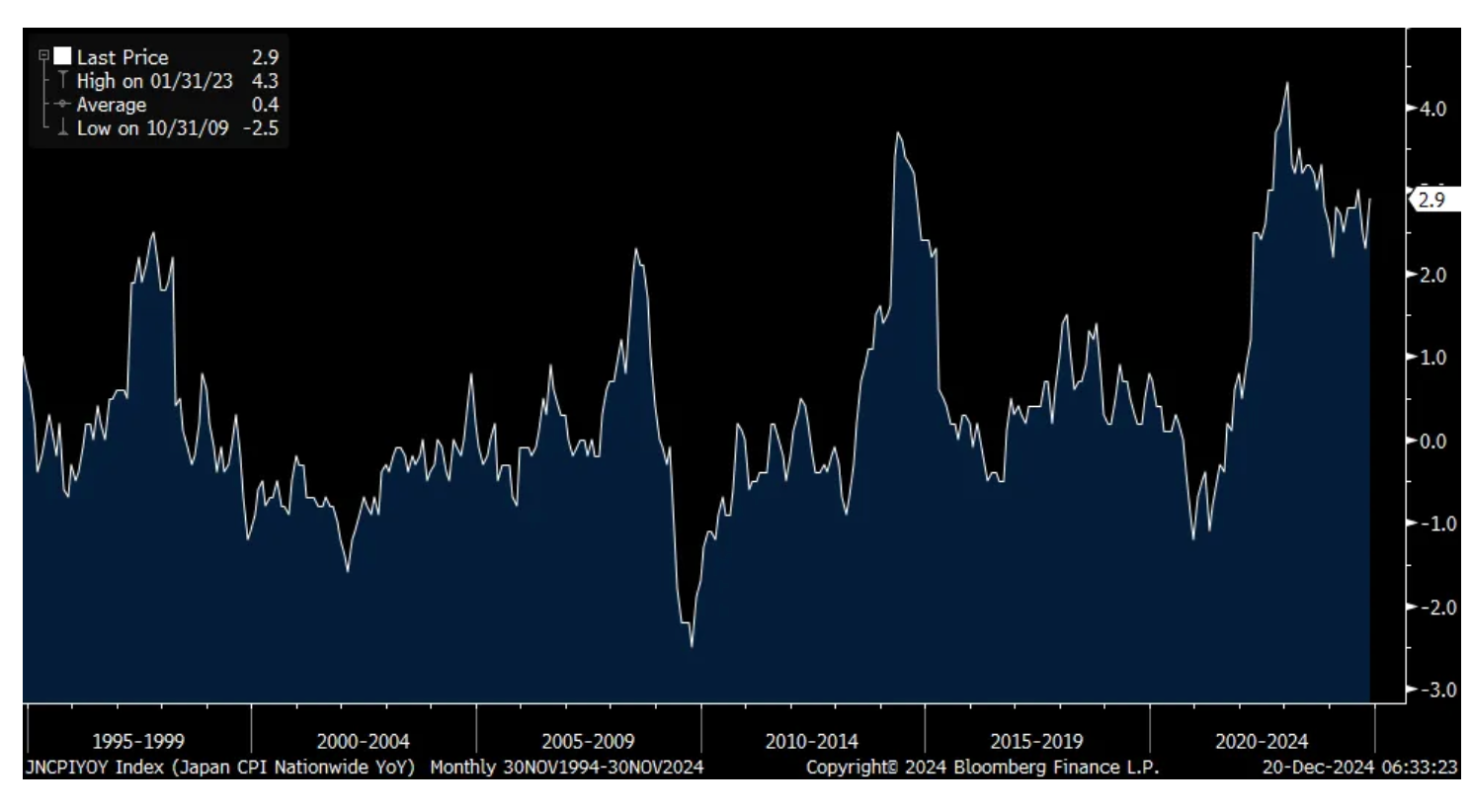

So, a day after the BoJ kept interest rates unchanged at just .25%, the November Japanese CPI rose 2.9% headline vs 2.3% in October and the core/core rate (ex food and energy) was up by 2.4% vs 2.3% in the month before. Both as expected but the headline figure is now above 2% for 32 straight months. As in the face of that the BoJ still expressed its interest in going slow and being patient with rate increases, this behavior reflects that the BoJ really is in bed with the Japanese government in that with so much debt the government constantly needs to roll, the higher interest rates go, the more expensive it gets.

As the data was in line, JGB yields were little changed but the yen is bouncing after yesterday's selloff. The Nikkei was down slightly, by .3%.

Wash, rinse, repeat. The BoJ drags its feet, the yen weakens, the Ministry of Finance threatens intervention, BoJ talks tough and hikes rates, yen rallies. BoJ doesn't follow thru with more hikes, yen weakens, the MOF threatens intervention. Overnight from the Finance Minister, we "are deeply concerned about recent currency moves, including those driven by speculators" and "we will take appropriate action if there are excessive moves in the currency market." We'll see if the BoJ hikes in January.

Headline CPI y/o/y in Japan

The PBOC kept its 1 and 5 yr loan rates unchanged as expected. The Taiwanese central bank did as well at 2% while the central bank in the Philippines cut its overnight borrowing rate to 5.75% from 6% as was the consensus.

The Brazilian central bank just intervened to defend the real by the way after it hit a record low vs the US dollar and spending concerns in Brazil.

Sovereign bond markets and FX are calling out reckless governments.

Approaching the holidays, November retail sales ex fuel in the UK rose .3% m/o/m but after a .9% drop in October and that was 2 tenths below expectations. This though does not include Black Friday there as it occurred at the end of the month. The ONS said "For the first time in three months, there was a boost for food store sales, particularly supermarkets. It was also a good month for household goods retailers, most notably furniture shops. Clothing store sales dipped sharply once again, as retailers reported tough trading conditions."

As we wrap up the year, the FTSE 100 is up just 4% year to date and trades at only 11.4x 2025 eps estimates with a 4% dividend yield, thus very cheap. In retail there, we own Tesco, the large supermarket company and luckily had a better year than the FTSE 100.

Let's get through the last batch of earnings reports for the year.

From FedEx, a stock we own:

The CEO mentioned "the challenging demand environment...Similar to last quarter, we experienced weakness in the industrial economy which negatively affected our B2B volumes, particularly in the US domestic package and the LTL markets. Continued market pressure coupled with difficult y/o/y comparisons weighed on our freight segment in the second quarter."

From Nike:

"What I've seen is traffic in NIKE Direct, digital and physical, has softened because we've lacked newness in product and we're not delivering inspiring stories. The result is we've become far too promotional. We've moved to a push model."

Sales fell 9% on a currency neutral basis, "with traffic and retail sales across the marketplace falling below our expectations, especially in September and October. In November, we saw momentum build, with digital and physical traffic inflecting positive, especially around the quarter's biggest consumer moments."

"inventory levels are higher than we would like, especially given recent sales trends on NIKE Direct."

From CarMax, the used car retailer:

"Our solid execution in a more stable environment for vehicle valuations enabled us to deliver robust EPS growth as we drove unit volume increases in sales and buys, maintained strong margins, stabilized the provision for loan losses and realized cost efficiencies."

"Average selling price declined approximately $1,100 per unit or 4% y/o/y" but gross retail gross profit per used unit rose a touch y/o/y.

The cost of borrowing to buy a used car from its finance unit? 11.2%, though down a slight 10 bps y/o/y. "The provision for loan losses was $73 million vs last year's provision of $68 million and results in a reserve balance of $479 million." They talked about payment extensions that provide customers that need help but "we recognize that some customers will eventually return to delinquency and result in a charge-off, and for this, we have reserved accordingly."

"I think consumers are still pinched from an inflationary standpoint, so they're looking for alternatives. And used cars, whether it's a two year old used car or a 14 year old used car, I think that helps the industry as well."

From Darden, the owner of restaurants across the income spectrum like Olive Garden, Longhorn Steakhouse, Yard House, Ruth's Chris, The Capital Grille, Cheddar's, Eddie V's and Seasons 52 to name a bunch and whose stock jumped 15% yesterday:

Providing value is helping, particularly at Olive Garden with its 'Never Ending Pasta Bowl' for a starting price point of $13.99. "Longhorn continues to exceed expectations driven by great guest value and strong operational execution." With Cheddar's, they "provide great food served with speed at a wow price."

On their fine dining segment, comps were negative at all their brands, in part due to the shift in timing with Thanksgiving and with the hurricanes but still down adjusted for this. Some of the reason is they got rid of lunch in some of their restaurants, "turned off 3rd party delivery" and "didn't take any price cuts at Ruth's Chris, where we had for the other brands."

They also talked about the influence of the GLP-1s. "I think right now, it's about 6% of the population are on GLP-1 drugs. It could be having an impact on the higher end brands, and we'll continue to monitor that."

On their overall consumer research, it "shows that consumer sentiment is trending positive, and there's a little bit of a feeling of optimism out there by the belief the labor market will improve."

"In contrast to previous quarters, we're seeing growth in visits from our guests making between $50,000 and $100,000 a year, which is really more of our Casual Dining brands. We're not seeing as much of an increase in visits yet on the consumers that are above that...it appears that consumers who were splurging on Fine Dining, basically those who were making less than $150,000, have continued to pull back. So, it's impacting Fine Dining a little bit. The kind of more average income consumer is starting to feel a little bit better."

"In regards to trade down, there could be some trade down from Capital Grille to Longhorn or Ruths' Chris to Longhorn, that might be benefiting them and maybe other steak players."

They saw total labor inflation of 3.7%.

From Lamb Weston, the maker of frozen potato products like french fries and whose stock fell 20% yesterday:

"Our second quarter performance was below our expectations and not what we aim to achieve at Lamb Weston...We expect a challenging operating environment will persist in the near term as weak restaurant traffic trends and additional capacity expansions announced by our competitors since our Investor Day last year add to the current imbalance in global industry supply and demand, especially outside North America."

I've been mentioning this week the continued rise in food prices and it caught up to Conagra, a stock we own as they said their inflation is closer to 4%, from a range of 3-4% they previously gave:

"there's inflation in cocoa and sweeteners, and that's very narrow in our portfolio, and we will be pricing to offset that, but the bigger driver for us has been protein. It's meats, eggs, things like that, and we did anticipate that there would be inflation in the 2nd half, but we anticipated that level of inflation will be lower. And we still anticipate that those peak protein costs are going to come down pretty much across the board, but there's a bit of a deferral for that."

US Steel is down pre market after lowering guidance on weak pricing and said "In Europe, the demand and pricing environment remains weak."

From Accenture, who benefited from business related to GenAI:

"Starting with the demand environment, we saw more of the same. Our clients are focused on reinvention, which means large scale transformations. We do not currently see an improvement in overall spending by our clients, particularly on smaller deals."

"GenAI continues to be a catalyst for reinvention across the enterprise, and building out the data foundation necessary to capitalize on AI is an increasing part of that growth. Themes around achieving both costs efficiencies and growth continue across the demand we're seeing."

BY Doug Kass · Dec 20, 2024, 8:41 AM EST

I covered my HOOD short at $34.50 (cost over $40) for a nice (+$6) and relatively quick gain in the premarket this morning.

From mid-December:

* Added to (HOOD) short at $41.59.

By Doug KassDec 9, 2024 3:10 PM EST

From early December:

I have added Robinhood (HOOD) to my financial services short list at $39.80 just now.

Trading within pennies of its 52-week high (and well off of its $10 low), most investors now fully appreciate the brokerage's successful transformation from a conduit for YOLO (and 0DTE option)trades to a more traditional asset gatherer.

Nonetheless, with an equity capitalization at nearly 1/5 of Goldman Sachs (GS) (I have been adding to this short) the shares seem overvalued.

More to come.

Position: Short HOOD (VS), GS (S)

By Doug KassDec 4, 2024 12:56 PM EST

BY Doug Kass · Dec 20, 2024, 8:36 AM EST

"We need to respect the up move... Because of policy changes and animal spirits small caps will benefit at only 10x forward EPS... I think small caps can outperform by more than 100% in the years to come... Everyone is scared of the bond market but we have had plenty of times when stocks rallied as bond prices fell and bond yields rose.... I kind of agree that animal spirits are growing ... Between now and year end (2024) a five to ten percent gain is likely and is my base case. The Fed is supportive of markets.... Margin debt hasn't risen in the last four months so we know investors haven't added risk. And with a dovish Fed multiple tailwinds exist."

- Tom Lee, CNBC Interview One Month Ago (at top in small caps and the senior averages) Small caps could outperform by more than 100% in the next few years, says Fundstrat's Tom Lee - YouTube

"This is another buying opportunity. To us, the fundamental support of stocks is intact ... There are signs of capitulation, the market has been bleeding lower. The spot VIX rose by +75% on Wednesday, of those four times in history with similar declines, the market recovered.... Investors are tired about getting the rug pulled, but nothing has undermined the attraction for small caps. Mergers and deal activity is another chance to buy the dip in small caps. "

- Tom Lee, CNBC Interview Thursday Market dip a buying opportunity, says Fundstrats' Tom Lee

I have argued strenuously over the last month against Tom Lee's call that the market will broaden away from large-cap tech and rotate towards small-cap and value stocks.

On small-caps: the Russell Index is not crowing and is leading the senior averages lower. About one week ago IWM traded at $240, in premarket trading today IWM is at $217.

Value stocks have declined for fourteen consecutive trading sessions (the previous record was nine days):

On value stocks (let's define this group by homebuilders, energy, financial and healthcare):

* Homebuilder equities are down by over -25% from their 2024 highs — TOL traded at $169 three weeks ago, now $123.

My tweet this morning:

* Energy stocks have been leading the S&P to the downside — a month ago XOM sold at $123, now $105.

* Financial stocks are rolling over now (that includes private equity, money center banks and other selected financials). Less than four weeks ago, Goldman Sachs GS traded at $615, now $550.

* Healthcare equities took this GLP-1 thing quite seriously as they have recently been losing a lot of weight:

BY Doug Kass · Dec 20, 2024, 8:00 AM EST

* A no drama short...

Investment short, Winnebago WGO, spits the bit on results and guidance.

The shares are -$4 to $48.50 and at a 52 (-7%) week low.

Here is the complete release. Winnebago Industries Reports First Quarter Fiscal 2025 Results - Winnebago Industries

BY Doug Kass · Dec 20, 2024, 7:38 AM EST

BY Doug Kass · Dec 20, 2024, 7:15 AM EST

The S&P Short Range Oscillator has moved further into a deeper oversold — at -8.55% vs. -7.86%.

BY Doug Kass · Dec 20, 2024, 6:42 AM EST

Berkshire Hathaway BRK.A BRK.B FINALLY added to its Occidental Petroleum OXY holdings this week, purchasing approximately 8.9 million shares between $45.80 and $46.56. Berkshire Hathaway's Warren Buffett purchases $409m in Occidental Petroleum stock By Investing.com

Announced in a Form 4 filing last night, Berkshire now owns nearly 265 million shares of OXY.

Here is the filing:

Sec Form 4 Filing - BERKSHIRE HATHAWAY INC @ OCCIDENTAL PETROLEUM CORP /DE/ - 2024-12-17.

There was no change in Berkshire's intent — for investment purposes only.

BY Doug Kass · Dec 20, 2024, 6:32 AM EST

Bonus — Here are some great links:

Dollar Breakout - Trouble for Stocks?

Entering Historically Best Season for Small Caps (From Jazzy Jeff Hirsch)

BY Doug Kass · Dec 20, 2024, 6:17 AM EST

From my friends at Miller Tabak:

Thursday, December 19, 2024

The November FOMC meeting was hawkish for three reasons. First, the Fed probably cut rates begrudgingly. Based on the dot-plot, four FOMC members (one dissenter and three non-voting members preferred to hold steady. The Fed likely cut partly because it was so widely expected. With policy uncertainty so high and growth strong, for now, we expect no rate cuts in Q12025 (January and March).

Second, the FOMC dialed back from 100 bps of cuts in 2025 to just 50 bps. The nature of the Summary of Economic Projections (SEP) makes it impossible to know how much of this was due to lingering inflation concerns versus the threat of tariffs. Chairman Powell acknowledged that some, but not all, FOMC members started to “incorporate economic effects of [new trade and fiscal] policies in their forecasts.” It is encouraging, however, that Powell stood by the Fed’s 2018 analysis of earlier tariffs. That analysis recognized that tariffs usually lead to one-time price spikes rather than sustained inflation and “looking through” this impact by not adjusting policy is realistic. Finally, the FOMC upgraded its estimate of neutral from 290 bps to 300 bps. Relatedly, six members now put neutral at 350 bps or higher, up from four.

In deciding how the new SEP affects our view, we start by asking if the Fed’s economic outlook is consistent with the policy guidance. In other words, with just 50 bps of cuts in 2025, will unemployment equal the Fed’s 4.3% forecast and will GDP growth reach 2.0%? We think not. The Fed has become too confident in the economy’s ability to further weather high rates. Absent any new tariffs, expect 50 bps of cuts to push unemployment up to 4.5% with GDP growth closer to 1.5%. Moderate new tariffs could push unemployment up to 4.8% and growth down to 1.0%, with further downgrades beyond 2025. Upcoming data are likely to push the Fed back towards a more aggressive set of rate cuts. 75 bps of cuts in 2025 are most likely with 100 bps at least as likely as the Fed’s predicted 50 bps.

The most significant aspect of the November meeting is the upgrade to the neutral rate. We still see 290 bps as the best estimate of neutral. Nevertheless, with six members now putting neutral at 350 bps or higher, the Fed is likely to move very slowly on additional rate cuts once it reaches 325-350 bps. We are thus upgrading our targets for long-term yields with the 10-year now likely to reach 390 bps (up from 380) by December 2025 and 335 bps (up from 320) by the end of 2026. This assumes that the U.S. avoids recession.

BY Doug Kass · Dec 20, 2024, 6:05 AM EST

Wolf Street howls about Census Bureau revisions for population growth.

BY Doug Kass · Dec 20, 2024, 5:55 AM EST

BY Doug Kass · Dec 20, 2024, 5:45 AM EST