From Peter Boockvar:

Succinct Summation of the Week’s Events:

Positives,

1)Within the October jobs data, average hourly earnings were as expected when including revisions and the y/o/y gain was 4% which compares with the pre Covid pace of 2.5%. Hours worked ticked up by one tenth to 34.3, still hovering around multi year lows, not including Covid.

2)Helped by a big seasonal adjustment lift, ADP said the US private sector added a net 233k jobs in October, about double the estimate of 111k and vs 159k in September which was revised up by 16k. There was almost no job growth for small businesses with employees under 50 but jumps for medium and large companies. On the pay side, wages for ‘job stayers’ rose by 4.6% y/o/y vs 4.7% in the month before. For ‘job changers’, pay was up 6.2% y/o/y vs 6.6% in September.

3)Initial claims fell to 216k, 14k below expectations and down from 228k in the week before. I’m not sure now what impact the recovery from the hurricanes is having in certain states. Smoothing it out, the 4 week average fell to 237k from 239k. Still elevated, though off the highest level in 3 years, continuing claims fell to 1.862mm from 1.888mm.

4)The headline September PCE gain was .2% m/o/m and the core rate was higher by .3% (and August was revised up by one tenth to a .2% gain), about as expected. The y/o/y increases were 2.1% and 2.7% y/o/y vs 2.3% and 2.7% in the month before. Lower energy prices kept a lid on the top line, partly offset by another gain in food. Also, services inflation continued on, offsetting the deflation in goods prices.

5)With regards to Q3 GDP, it was about as expected at 2.8% and driven by a 3.7% rise in consumption which added 246 bps to that figure. Within consumption was a jump in durable goods spending which added 60 bps to GDP, with almost half being motor vehicles. Spending on services added 120 bps. The other area of GDP growth was from government spending, contributing 85 bps to GDP with national defense making up 50 bps of that. Elsewhere, there was no growth. Trade was a detraction of 56 bps, inventories subtracted just under 20 bps and gross private domestic investment was flat. The only bright spot in this last category was 56 bps added by spending on equipment which I’d guess is related to AI data center buildouts. There was no contribution from spending on intellectual property as AI spend is stealing from other CapEx. Residential construction took off 20 bps from GDP.

6)September personal Income growth was as forecasted, up by .3% while spending was up .5% m/o/m, one tenth above expectations. Spending growth was evenly split between goods and services.

7)The Q3 Employment Cost Index rose .8% q/o/q vs the estimate of .9%. It was up 3.9% y/o/y. Specifically private sector wages and salaries rose .8% q/o/q and 3.8% y/o/y which is further moderation but in part due to tougher comps. They rose 4.5% in Q3 2023 to highlight. In Q3 2019, private sector wages and salaries grew by 3% y/o/y, for perspective.

8)With the average 30 yr mortgage rate in September falling all the way down to about 6.15% (now back to 6.73%), the lowest in a year and a half, home buyers stepped up according to the National Association of Realtors in today’s pending home sales figure which rose 7.4% m/o/m, well above the estimate of 1.9%. Sales were up 2.2% y/o/y.

9)Apartment List released its October rent report and new lease rates fell by .7% m/o/m "as we get further into the slow season for the rental market." Rental rates are also down .7% y/o/y. Also, "On the supply side of the rental market, our national vacancy index ticked up to 6.8%, the highest reading since the onset of the pandemic...The third quarter of 2024 saw the most new apartment completions for a single quarter in 50 years, and with more than 800k units still in the construction pipeline, the supply boom has runway to continue into 2025."

10)The October consumer confidence index from the Conference Board rose to 108.7 from 99.2 and that was much above the estimate of 99.5. Both main components were up m/o/m. One yr inflation expectations rose one tenth m/o/m to 5.3% which matches a 4 month high. The Conference Board said the uptick in inflation expectations could be led by food and services. They also said “Mentions of prices and inflation continued to top write-in responses as topics affecting consumers’ views of the economy, but more respondents mentioned slower inflation and lower grocery prices.” The main reason for the confidence lift was the improvement in the answers to the labor market questions. Spending intentions were mixed.

11)From Apple: "iPhone revenue set a September quarter record of $46.2b up 6% from a year ago, with growth in every geographic segment. On Apple Intelligence, “We're getting a lot of positive feedback from developers and customers. And in fact, if you look at the first three days, which is all we have, obviously, from Monday, the 18.1 adoption is twice as fast as the 17.1 adoption was in the year ago quarter. And so, there's definitely interest out there for Apple Intelligence."

12)From Amazon: "At a time when consumers are being careful about how much they spend, we're continuing to lower prices and ship even more quickly, and we can see this resonating with customers as our unit growth continues to be strong and outpace even our revenue growth."

13)From Microsoft: Their cloud drove most of the growth and their AI business "is on track to surpass an annual revenue run rate of $10 billion next quarter, which will make it the fastest business in our history to reach this milestone."

14)Meta saw 20% y/o/y revenue growth, an incredible pace off a big base and with 3.2 billion people "using at least one of our family of apps on a daily basis in September."

15)From Google/Alphabet: Sundar Pichai wasted no time talking about AI going right at it after saying "Q3 was another great quarter." Cloud growth was strong at 35% y/o/y with operating margins at 17%. Search saw sales rise by 12% y/o/y "led by growth in the financial services vertical due to strength in insurance followed by retail."

16)From Camden Property Trust: Not positive for them but for the consumer was easing rental growth, 'Signed New Lease Rates' fell 4.8% y/o/y in October 2024 and only partly offset by 'Signed Renewal Rates' which rose 3%, thus giving a 'Signed Blended Lease Rate of -1.7%. If you look at when these rates will become effective, the blended rate is down .8% y/o/y.

17)From Mastercard: "The macroeconomic environment remains supportive and continues to underpin the strength in consumer spending. The labor market remains strong, even if slightly below historically tight levels. And inflation has moderated, albeit at varied levels across categories and countries. Overall, we remain positive about our growth outlook, but we will continue to monitor the environment."

18)From Visa: On the US consumer, "Consumer spend across all segments from low to high spend has remained relatively stable to Q3. Our data does not indicate any meaningful behavior change across consumer segments from last quarter."

19)From Capital One: On the consumer, "I think the US consumer remains a source of relative strength in the overall economy. The labor market remains strong. You know we saw signs of softening in the first half of 2024 and the unemployment rate ticked up a bit, but the most recent data points on unemployment and job creation have actually shown renewed strength. Incomes are growing in real terms and last month, we saw a significant upward revision of the savings rate. Consumer debt servicing burdens are stable relative to pre-pandemic levels and consumers have higher average bank account balances than before the pandemic."

20)From Mister Car Wash: To a question on the broader demand trends and income level, "it's been pretty consistent across the board. We haven't seen anything unusual, when we slice and dice it by average household income. Again, you would think that the bottom quartile would behave differently, but we're just not seeing that. So it's a little head scratching, to be honest with you. And our interpretation again is that the universal appeal of car wash services and the fact that, if anything, if people have been holding back, they're starting to come back because their cars are really dirty and they want to get them clean."

21)Brinker’s via Chili’s, Cheesecake Factory, Shake Shak and Texas Roadhouse all thread the restaurant needle in casual dining with value menus and having less lower income consumer exposure.

22)From Chipotle: On their consumer, "We're still seeing strength across all income cohorts, even in this competitive environment, which gives us the belief that we are still delivering extraordinary value for the consumer...Again, all income cohorts, even low income, are showing positive signs of strength."

23)From Booking Holdings: Revenue grew by 9% y/o/y. "From a regional perspective, we observed an improvement in our room night growth in Europe in the third quarter, which was the primary driver of the sequential increase in our global room night growth. In Asia, we continue to perform well with another quarter of double digit growth...In the US, we see relatively stable levels of growth in our business so far this year, which we think continues to outpace the broader US accommodation industry."

24)From MGM Resorts: "we saw record ADRs in Las Vegas and record occupancy at our regional resorts…In the 4th quarter here in Las Vegas, we're encouraged by the stability of demand that we're seeing. We're also gearing up for year two of F1, which while not as large as last year's event, still brings significant economics to MGM during what has historically been one of the slowest weekends of the year, no more…In Macau, MGM China achieved a record breaking 3rd quarter with net revenues increasing 14% y/o/y."

25)From Royal Caribbean: "Robust demand for its vacation experiences drives strong results and improved outlook." They saw "stronger pricing on close-in demand, continued strength in onboard revenue and lower costs due to timing" and "We see elevated demand patterns continuing as we build the business for 2025."

26)From Martin Marietta:: "Looking ahead to 2025 and beyond, we expect to benefit from record levels of federal and state investments in highways, streets and bridges. Additionally, reshoring and the build out of artificial intelligence infrastructure should provide steady growth in these aggregates-intensive end markets for years to come."

27)From Decker’s: "HOKA continued to experience solid growth around the globe" and "UGG again demonstrated broad based growth across regions and channels."

28)China's private sector focused Caixin manufacturing PMI rose 1 pt m/o/m to 50.3. The improvement was domestic as "External demand, however, remained weak. The gauge for new export orders stayed in contractionary territory for the 3rd consecutive month, reflecting sluggish global economic conditions, which weighed particularly on exports of investment and consumer goods."

29)China's October manufacturing and non-manufacturing composite index rose a touch to 50.8 from 50.4 in September with manufacturing lifting to 50.1 from 49.9 while the latter rose to 50.2 from 50.

30)The October Vietnam manufacturing PMI 51.2 vs 47.3.

31)While the BoJ may hike again in December or January, they dragged their feet again this week.

32)Japan reported better than expected jobs data for September.

33)The Eurozone saw a better than expected Q3 performance with a q/o/q gain of .4%, twice the estimate and higher by .9% y/o/y. Part of the increase was a better than expected print from Germany but only after their Q2 figure was revised down. It really was a slightly above estimate number from France and Spain that helped while Italy saw no growth vs the estimate of a .2%.

34)There was slight improvement in the German consumer confidence index from GFK to -18.3 from -21. The estimate was -20.5 and while still negative, it's the best print since April 2022. While a slight m/o/m gain, GFK said "The uncertainty caused by crises, wars and rising prices is still very much present and is preventing factors that encourage consumption, such as real income growth, from taking full effect."

Negatives,

1)Let’s put aside the weaker than expected October job growth in the establishment survey due to all the noise and distortions due to the weather (strike impact easier to quantify) but the prior two months were revised down a total of 112k. Also, look at household survey. Jobs lost in this figure totaled 368k and also there was a 220k fall in the size of the labor force. This follows gains of 430k in the month before in employment and 150k in the labor force size.

2)Job openings in September fell to 7.44mm, down about 400k m/o/m and well below the estimate of 8mm. That is the least since January 2021. The hiring rate did tick up to 3.5% from 3.4% but the quit rate fell to 1.9% which is the lowest since 2015 not including Covid.

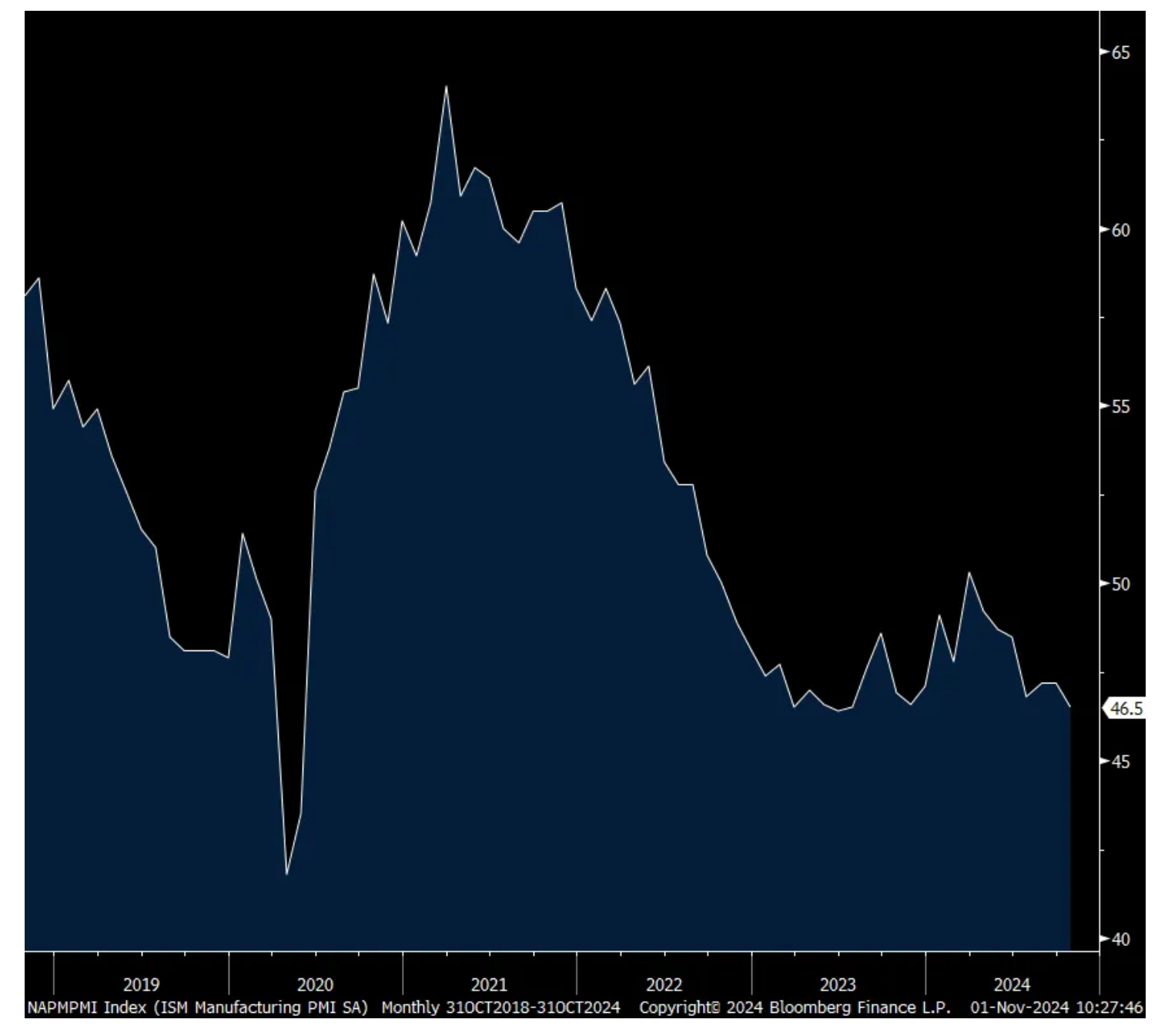

3)The US manufacturing recession continues on as measured by the October ISM index which fell to 46.5 from 47.2 and that was 1.1 pts below expectations. This index has had one 50+ print since October 2022. In terms of overall industry breadth, 5 of 18 surveyed saw growth, the same number seen in September, while 11 experienced a contraction. The bottom line from the ISM, “Demand remains subdued, as companies continue to show an unwillingness to invest in capital and inventory due to concerns (for example, inflation resurgence) about federal monetary policy direction in light of the fiscal policies proposed by both major candidates. Production execution eased in October, consistent with demand sluggishness.”

4)Combining the income and spending figures saw the savings rate drop to 4.6% in September which is the lowest since December 2023.

5)The MBA said the average 30 yr mortgage rate jumped by 21 bps w/o/w to 6.73% coincident with the rise in the 10 yr yield. Purchases though did rebound by 5% after 3 weeks of declines but refi's fell again, by 6.3% w/o/w.

6)The 10 yr gilt yield rose to a one year high as clearly UK debts and deficits matter again. The 2 yr yield jumps too.

7)From Apple: On Apple Intelligence and the upgrade cycle, I don’t think it’s ramping as quick as hoped but CFO said, "we've very early in the cycle, very early in the cycle with a lot of new products and features that we are launching, and we're very excited about them, but it's early, and the Apple Intelligence rollout is going to happen over time, not across the world as normally we do with software releases."

8)From Microsoft: All the spend is a big focus. "Capital expenditures including finance leases were $20 billion in line with expectations...Roughly half of our cloud and AI related spend continues to be for long lived assets that will support monetization over the next 15 years and beyond. The remaining cloud and AI spend is primarily for servers both CPUs and GPUs to serve customers based on demand signals." As a result of all this spend, free cash flow fell 7% y/o/y.

9)From Meta: Same here. "Capital expenditures, including principal payments on finance leases were $9.2 billion, driven by investments in servers, data centers, and network infrastructure." And here is their guidance, "We anticipate our full year 2024 capital expenditures will be in the range of $38 billion to $40 billion, updated from our prior range of $37 billion to $40 billion. We continue to expect significant capital expenditure growth in 2025."

10)From Google/Alphabet: Same here. Their CapEx in the quarter was $13b, "reflecting investment in our technical infrastructure with the largest component being investment in servers, followed by data centers and networking equipment. Looking ahead, we expect quarterly CapEx in the 4th quarter to be at similar levels to Q3."

11)From Hyatt: "we reported system wide RevPAR growth of 3%, and we continue to see high end consumers prioritizing travel as RevPAR growth was strongest amongst our luxury brands. Leisure transient revenue decreased approximately 4% in the quarter driven by the US and Greater China."

12)From Uber: "we've been very public in terms of the increase, the substantial increase in commercial insurance costs, really that have happened over the past two years. And as we have passed on those increases in costs, especially in states where insurance costs are very, very high, like New Jersey or California, as we passed on those costs, we've seen the kind of the typical elasticity from consumers, which is as price goes up, the transaction growth slows down a bit. And that elasticity is usually one for one." Also, "We are seeing weekday growth stronger than weekend growth as well. So people are definitely getting back to work. I think like the weekend party hours, maybe consumers are a little more price sensitive in terms of whether they choose to go our or not. But weekday is very strong."

13)From Starbucks: With respect to the 6% drop in US comps, it was "driven by a 10% decline in comparable transactions, partially offset by a 4% increase in average ticket, mainly from pricing. Traffic declined across all channels and day parts, with the most pronounced decline in the afternoon day part. In addition to the continued decline of non-Starbucks Rewards member visits, frequency also slowed across all SR member deciles, in comparison to prior year and ultimately impacted spend."

14)From McDonald’s: "On our last call, we shared the QSR sector had meaningfully slowed in many of our markets with industry traffic declining in several major markets and that consumers, especially those in the low-income category were choosing to eat at home more often. This trend continued in the third quarter. QSR traffic has remained under pressure reflecting industry wide challenges. And while we anticipated a challenging environment in 2024, our performance so far this year has fallen short of our expectations."

15)From EBAY: "We continue to face a dynamic macro and consumer spending environment in the quarter. And as we noted on the last earnings call, political news, sporting events and elevated travel in July influenced consumer behavior."

16)From Malibu Boats: "we navigated a challenging market environment driven by continued macroeconomic factors and slower retail demand. Net sales decreased by approximately 33% y/o/y as we maintained our focus on reducing channel inventories. While we are encouraged by the recent move in interest rates, we will need a sustained cycle of rate cuts, bring back payment buyers into the market. Retail demand remains challenging and will likely remain challenging until payment buyers return to the market."

17)From CDW: "While demand for cloud solutions remained strong and we continued to see a pickup in client device growth, hardware solutions remained under pressure and the firmer footing we anticipated for our corporate channel did not materialize…the macro and IT spending environment remained challenging. Technology complexity combined with persistent economic and geopolitical uncertainty has led to large project delays and further extension of sales cycles. Laid on top was the uncertainty around the outcome of the US election, which has dampened not only government spending but also other public sector end markets, as well as spend from commercial customers.” Also, "this limited demand environment has heightened competition and increased pricing intensity across all end markets."

18)From Stanley Black & Decker: "As we look at our markets in aggregate today, they remain relatively stable on the surface. That said, some continue to be pressured by the continuation of mixed consumer trends, especially related to housing, as well as weak automotive production backdrop."

19)From DR Horton: "Our sales pace was in line with normal seasonality from the 3rd to 4th quarter but was below our expectations. While mortgage rates have decreased from their highs earlier this year, many potential homebuyers expect rates to be lower in 2025. We believe that rate volatility and uncertainty are causing some buyers to stay on the sidelines in the near term. To help spur demand and address affordability, we are continuing to use incentives such as mortgage rate buydowns, and we have continued to start and sell more of our homes with smaller floor plans."

20)From TriNet: "Slower economic growth, higher interest rates, and generally cautious outlook resulted in a third quarter of no net hiring amongst our customer base. While the headline jobs reports have been generally positive from the BLS over the last year, our experience has differed materially. Growth in several sectors, including government, construction, and healthcare are fueling aggregate headlines, while our core verticals of technology, life sciences, financial services, and other professional services have been muted."

21)From Ford: On the EV business, "No doubt there's a global price war and it's fueled by overcapacity, a flood of new EV nameplates, and massive compliance pressure. In our home market in the US, no OEM is immune. Since Q1 of last year, EV volumes have grown 35% while revenues in total are flat at $14 billion. That means the progress on volume has been fully offset by prices. We're expecting roughly 150 new EV nameplates to hit North America by the end of 2026. And some of our competitors are already resorting to very aggressive lease tactics even on brand new products which creates huge residual risk and overhang and brand damage."

22)From Capital One: the caveat to their positive comments on consumer, "Now we see some pockets of pressure related to sort of the cumulative effects of inflation and elevated interest rates. And we are almost certainly still seeing a thing that we've been calling out for years, even really before it happened saying we think it inevitably will happen but we won't fully be able to measure that. We won't be able to measure that along the way, but that is delayed charge-offs from the pandemic period. We should remember that millions of consumers who would have charged off under normal circumstances in 2020, 2021 and 2022 avoided defaulting, thanks to unprecedented stimulus and forbearance. And these consumers were on the edge, and they got a lifeline. But for some of them, their underlying vulnerability remains. So I believe that what we're seeing today is catching up from that period of historically low charge-offs."

23)From Carter’s: "Shopping for holiday related apparel trended later than last year, we believe consumers are shopping closer to need and buying what's needed and only when needed. In recent weeks, thankfully, as weather turned cooler in more parts of the country, the trend in our holiday related apparel has improved."

24)Manufacturing PMI’s seen in Asia: Taiwan 50.2 vs 50.8, South Korea 48.3 vs 48.3, Thailand 50 vs 50.4, Indonesia 49.2 vs 49.2, and Malaysia 49.5 vs 49.5.

25)The UK October manufacturing PMI was revised to 49.9 from the initial figure of 50.3 and down from 51.5 in September. That's the weakest since April. S&P Global attributed some of this softness to hesitancy ahead of the unveiling of the new UK budget which is now out. Also, "This domestic headwind, combined with an ongoing loss of export business, led to the first outright contraction in new work intakes since April. Output growth came close to stalling as a result."

26)In the Eurozone, October CPI rose 2% y/o/y, a touch above the estimate of 1.9% and up from 1.7% last month. The core rate held at 2.7%, also one tenth above expectations. Services inflation is still pretty persistent, rising 3.9% y/o/y while goods prices are muted, rising .5% y/o/y. Lower energy prices continue to keep a lid on the headline, down by 4.6% y/o/y but food/alcohol/tobacco prices were higher by 2.9% y/o/y.

27)Germany said that in October the number of unemployed jumped by 27k which was about double the forecast of up 15k. Their unemployment rate was 6.1%, holding to match the highest since October 2020.

28)The October Eurozone Economic Confidence index fell to 95.6 from 96.3 which is below the estimate of no change and continues to flat line. Manufacturing weakened further while consumer confidence and those in retail and construction were less negative. Services continue to be the standout, though unchanged m/o/m in positive territory.

29)Phil Lesh, “such a long, long time to be gone and a short time to be there.”