From JPMorgan:

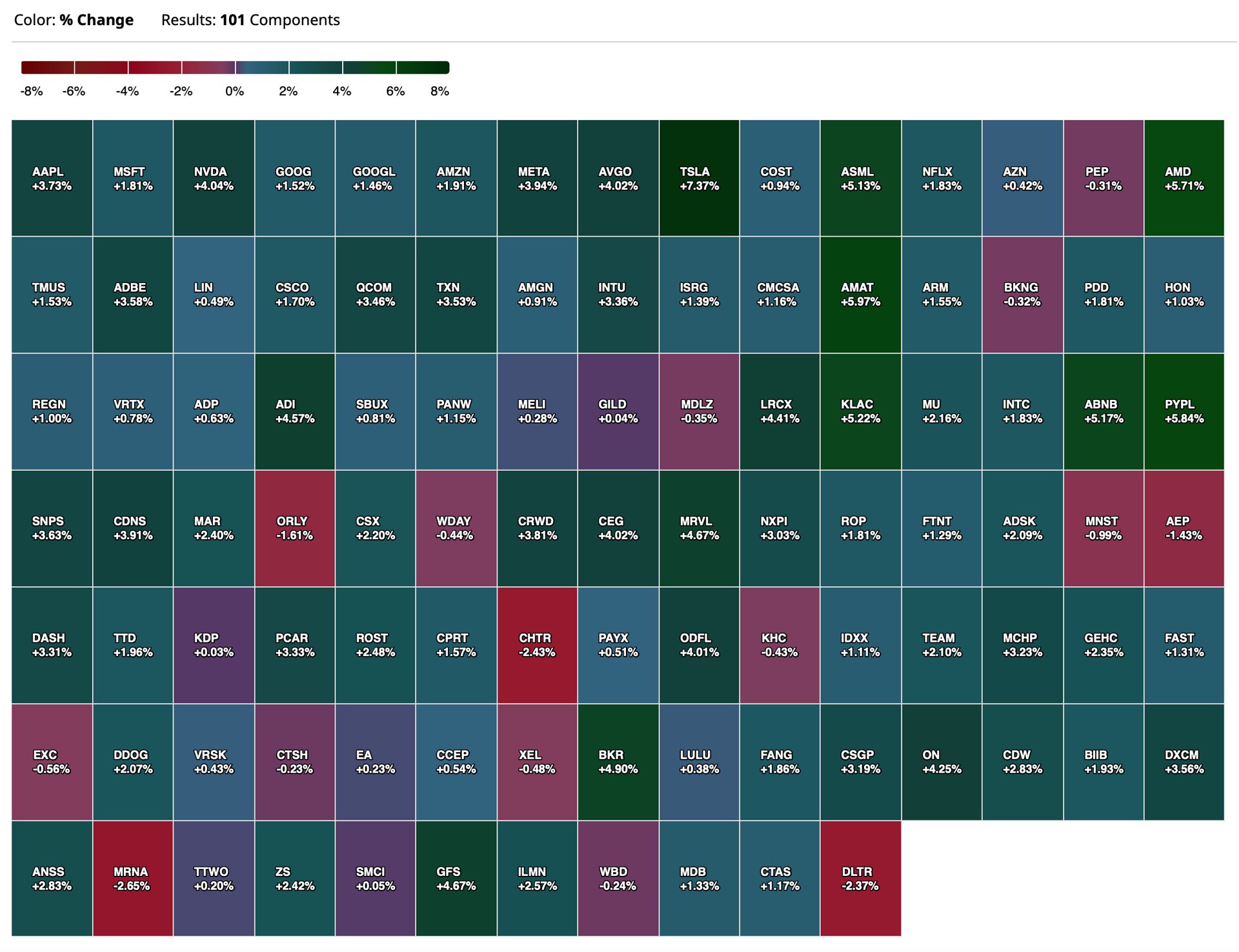

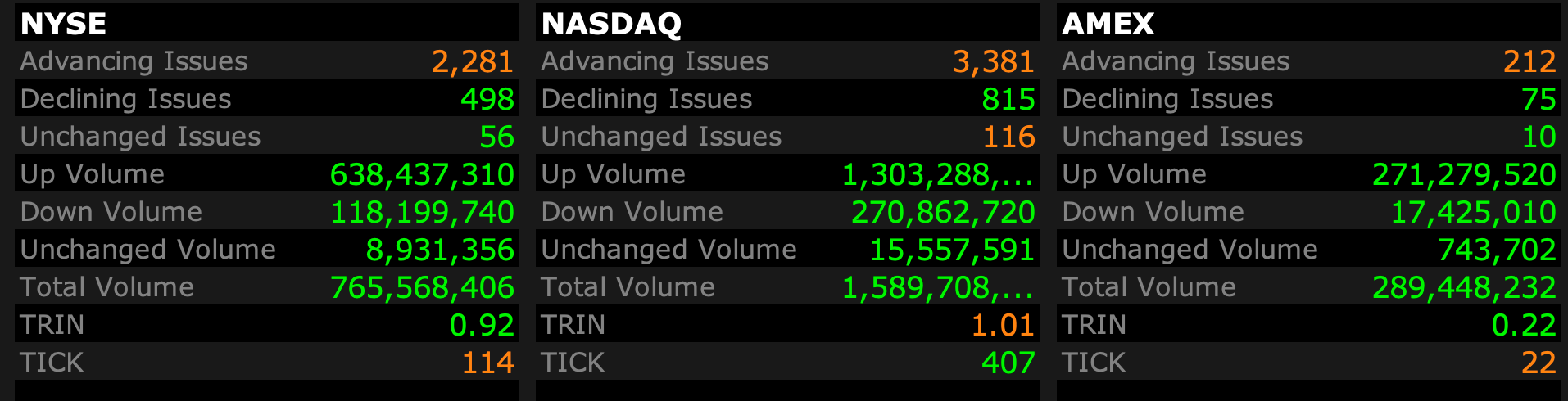

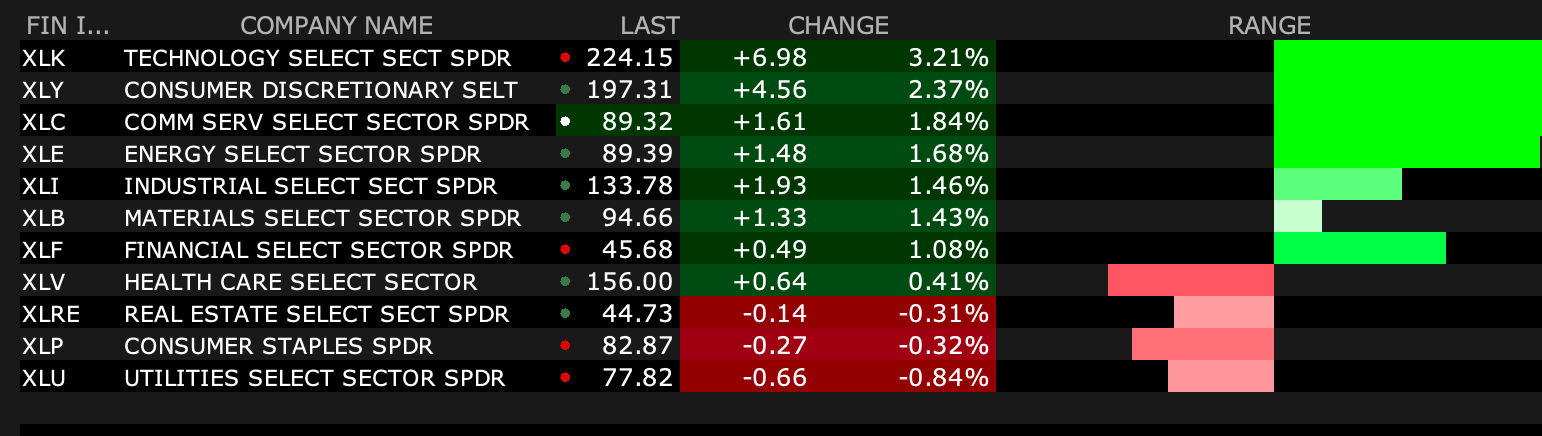

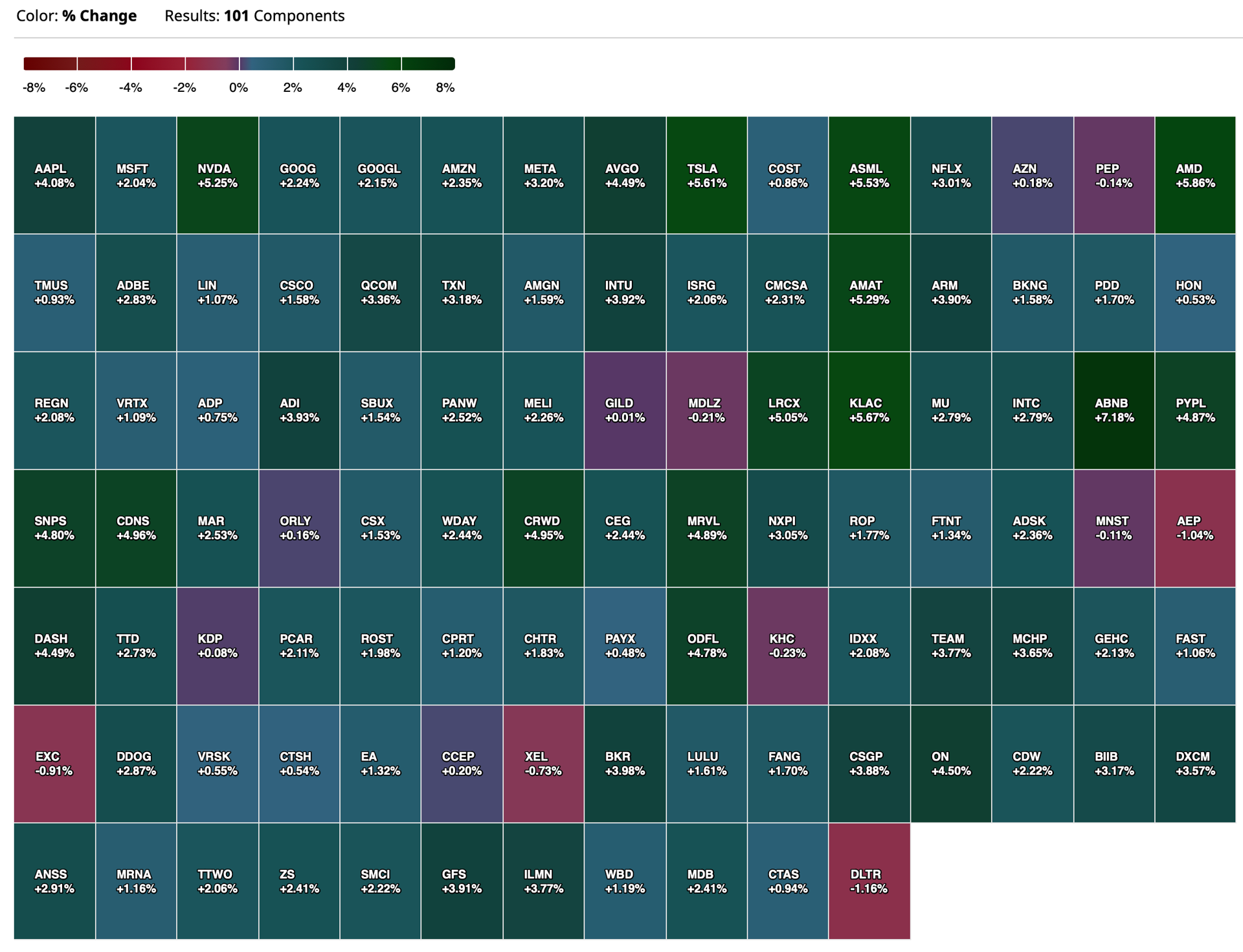

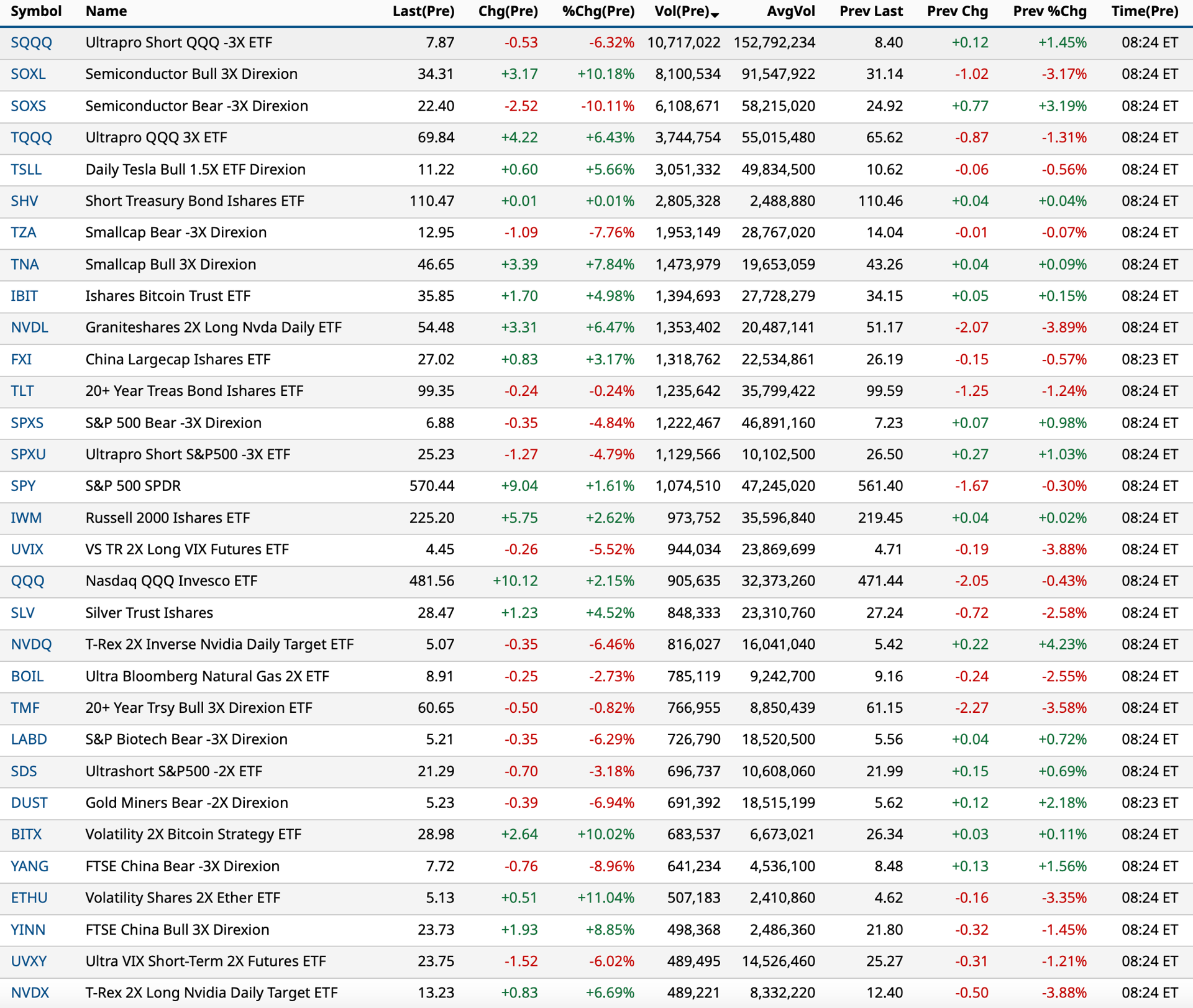

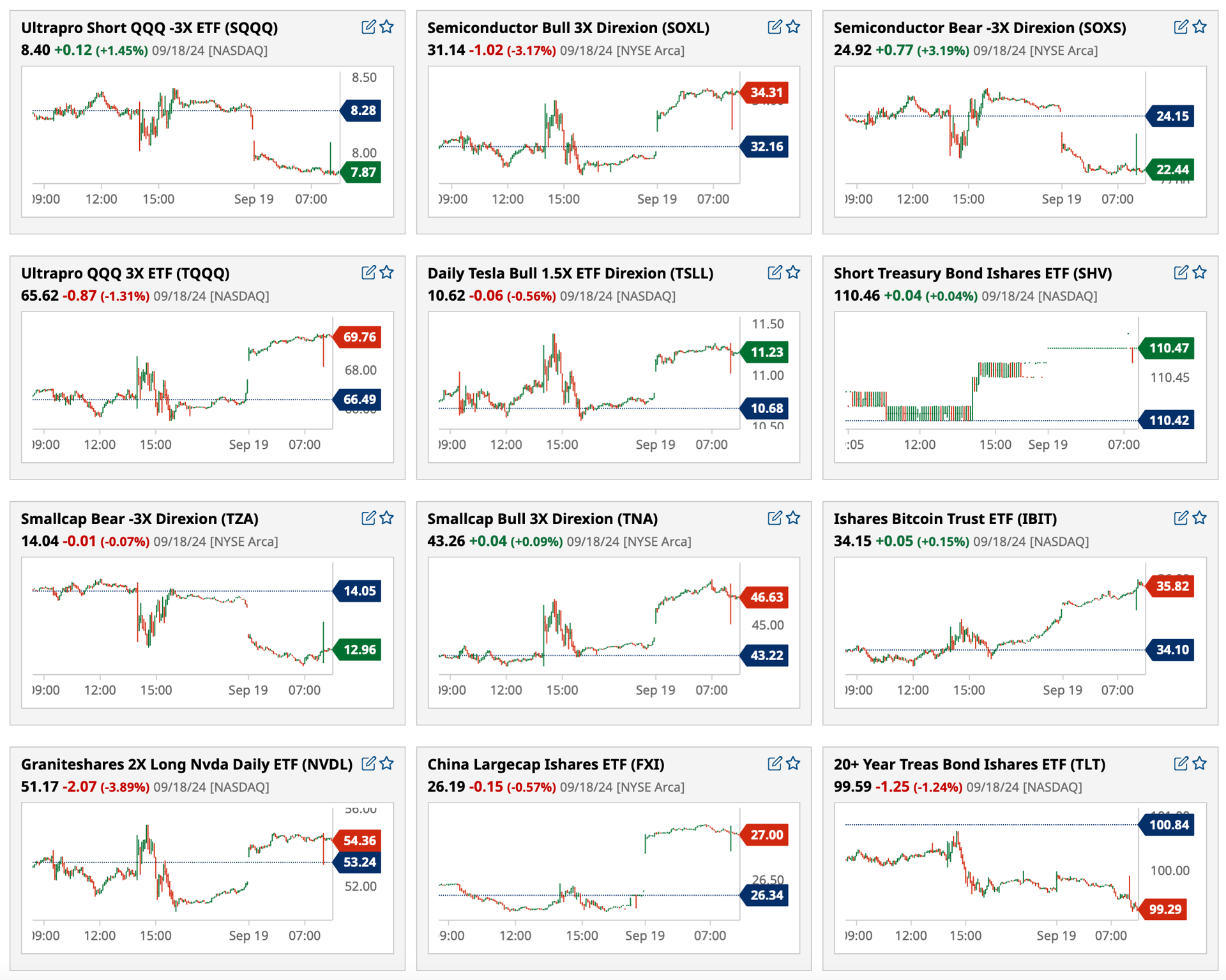

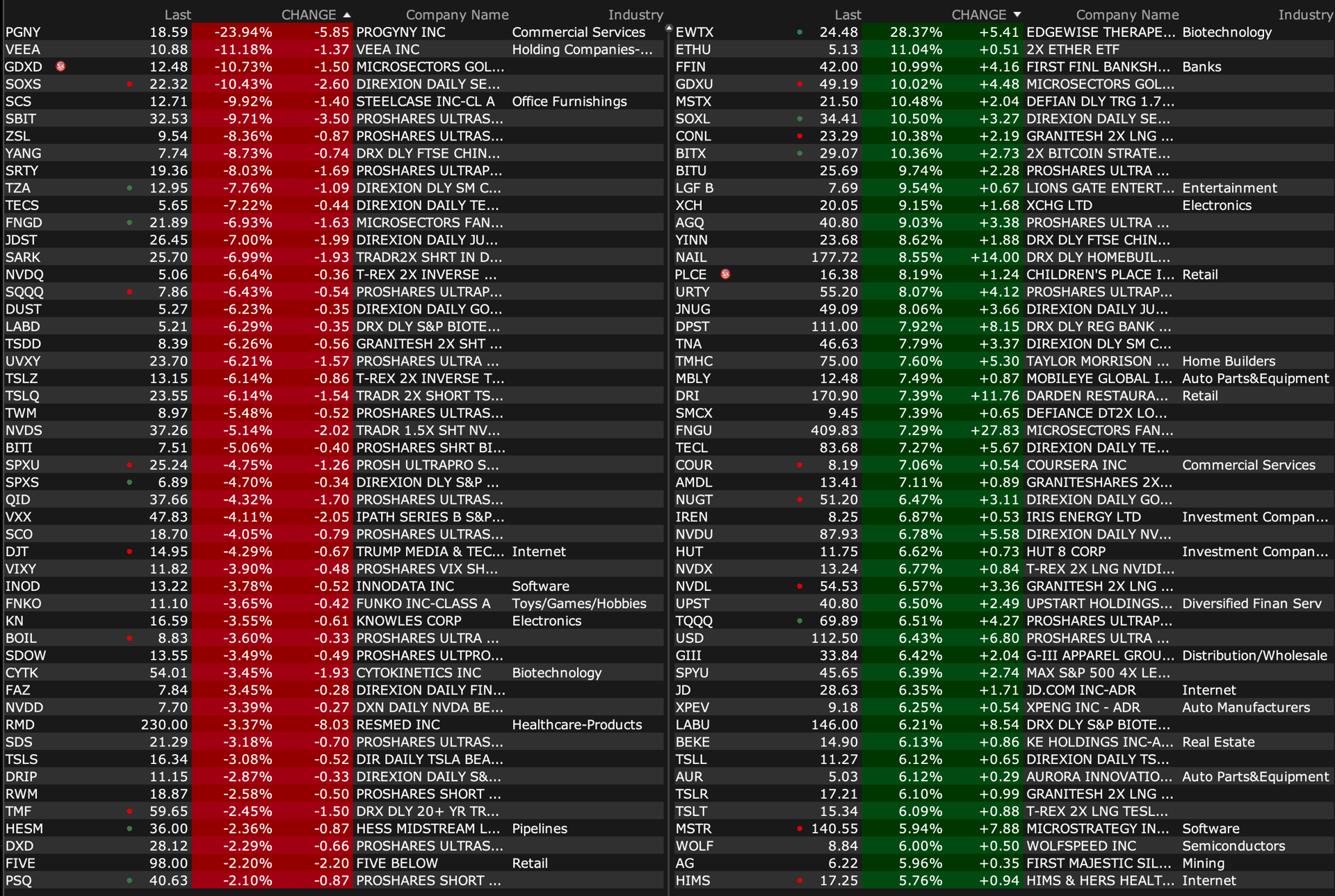

US: Futs are ripping as part of a global risk-on trade; tip of the cap to Mike Feroli for his excellent call on the Fed yesterday. Similar to past rate cuts in strong macro environments, NDX and RTY are outperforming. Pre-mkt, Mag7 names are all higher by at least 1.6%, Semis are stronger too with NVDA +3.3%. The yield curve is bull steepening though 30Y is unchanged and USD is flat. Cmdtys are higher led by the Energy complex with precious metals outperforming base (Gold +1.3%, Silver +4.0%). The macro data today will be ignored given the dovish press conference from Powell; expect multiple indices and sectors to make ATHs today.

and...

EQUITY AND MACRO NARRATIVE: These bullets were posted into IB chats yesterday morning and the balance of the note is color designed to give additional context to the current trading environment. The TL: DR version is this: the economy is growing above trend, this should have a positive impact on earnings, so the drivers of stocks are stronger than historic trends which should yield more upside to the bull market.

· JPM TRADING DATA (Craig Cohen) – Over the past 40 years, the Fed has cut rates 12 times with the S&P 500 within 1% of an all-time highs. The market was higher a year later all 12 times with an average return of around 15%.

o Aligns with the US Mkt Intel view that this easing cycle will be most similar to the 1995 version where SPX was +2.1% one month after the first cut and +6.3% three months after the first cut. Nasdaq outperformed NDX on both a 1-month and 3-month basis; interestingly NDX underperformed SPX on a 3-month basis. RTY outperformed SPX in both time periods.

o A copy of my team's Trading the Easing Cycle note may be found here.

POWELL SNIPPETS – sourced from Bloomberg

· US economy is in a good place, cut is to keep it there

· Labor market conditions pretty close to max employment

· Retail sales, GDP show economy growing at solid pace

· It feels to me that neutral rate is probably significantly higher than it was pre pandemic

· Don't see anything suggesting downturn chances elevated

· Housing inflation is one piece that is dragging a bit

· Going to take some time, direction of travel is clear

· US MKT INTEL – Our economic hypothesis has been that the US Consumer is in a position of significant strength, certainly there are some that are constrained by cumulative inflation, but overall spending remains robust. The unemployment rate is higher YTD primarily due to increases in labor supply and not due to layoffs meaning that spending will remain higher than expected. There is a strong credit impulse in the market place with additional pent-up demand that can manifest itself in both stronger business formation, hiring, and housing demand. Powell’s press conference supported this hypothesis and the comments on the higher neutral rate mean that the bond market’s expectation for 250bps of cuts by YE25 is too many. Given this context it is not surprising to see bond yields reprice higher and for the intra-day move in stocks to move defensively (see Manish’s comments in the next section). In our view, this macro environment remains supportive of stocks and after this short-term volatility, we expect stocks to move higher, materially so.

o The most pertinent client question may be, “what do we do in October?”. Many clients agree with the macro outlook described in the previous bullet but acknowledging negative seasonality that may last into the Election, this is one of the most common questions. I do not have a strong view on seasonality so for others of the same view, perhaps the best course of action is to do some incremental buying each week into the Election, such that one is fully positioned just before the date as we expect markets to rip higher into year-end with the latest start date the day after the Election.

o MONETIZATION MENU – We favor the barbell with a heavier tilt to the Value/Cyclical side. TMT side = Mag7, Data Centers, and Semis. Value/Cyclical side = Banks, Homebuilders, Autos, Transports ex-Airlines, and RTY. We like using factor hedges of both Beta and Momentum. From a pairs trade perspective gold vs. base and DM EU vs. EM. In derivatives, we like Energy Equity upside and using downside in Chinese ADRs.