DEA to Delay Final Ruling on Marijuana

This is a blow to the cannabis space.

DEA Schedules Hearing On Marijuana Rescheduling Proposal, Delaying Final Rule - Marijuana Moment

BY Doug Kass · Aug 26, 2024, 5:16 PM EDT

This is a blow to the cannabis space.

DEA Schedules Hearing On Marijuana Rescheduling Proposal, Delaying Final Rule - Marijuana Moment

BY Doug Kass · Aug 26, 2024, 5:16 PM EDT

BY Doug Kass · Aug 26, 2024, 5:10 PM EDT

- NYSE volume 321M shares, 23% below its one-month average;

- NASDAQ volume 4.24B shares, 8% below its one-month average

- VIX: up 0.44% or 15.94

BY Doug Kass · Aug 26, 2024, 4:28 PM EDT

Thanks for reading my Diary today.

Enjoy the evening.

Be safe.

BY Doug Kass · Aug 26, 2024, 4:08 PM EDT

I have a research call at 2:15 p.m.

Will be back by 3 p.m.

Radio silence.

BY Doug Kass · Aug 26, 2024, 2:17 PM EDT

BY Doug Kass · Aug 26, 2024, 1:15 PM EDT

* A lesson (sic transit gloria) from history...

From my lynx-eyed friend, Larry McDonald:

BY Doug Kass · Aug 26, 2024, 12:56 PM EDT

venuv

23 minutes ago

This is either the sign of a hard landing to come for the US ( to the extent that MBA hires are a signal on health of SP500) or just a hard landing for B-schools (which I have a hard time sympathizing with) -

BY Doug Kass · Aug 26, 2024, 12:20 PM EDT

While I am not a fan of directional options bets, based on my hope that Berkshire BRK.A BRK.B is upping its stake in Occidental Petroleum OXY, I have purchased the following OXY Sept 6 call options (I also own October calls):

Exercise Prices (and Call Prices)

$57 ($1.12)

$58 ($0.60)

$59 ($0.28)

$60 ($0.12)

But be prepared to rip up these speculative and short dated call options — so weight accordingly (PLEASE!)

BY Doug Kass · Aug 26, 2024, 12:00 PM EDT

I moved to uber large on OXY (under $57.40) on the weakness from the morning's highs.

I remain hopeful (and have my toes and fingers crossed) that Berkshire BRK.A BRK.B refiles tonite or tomorrow.

BY Doug Kass · Aug 26, 2024, 11:53 AM EDT

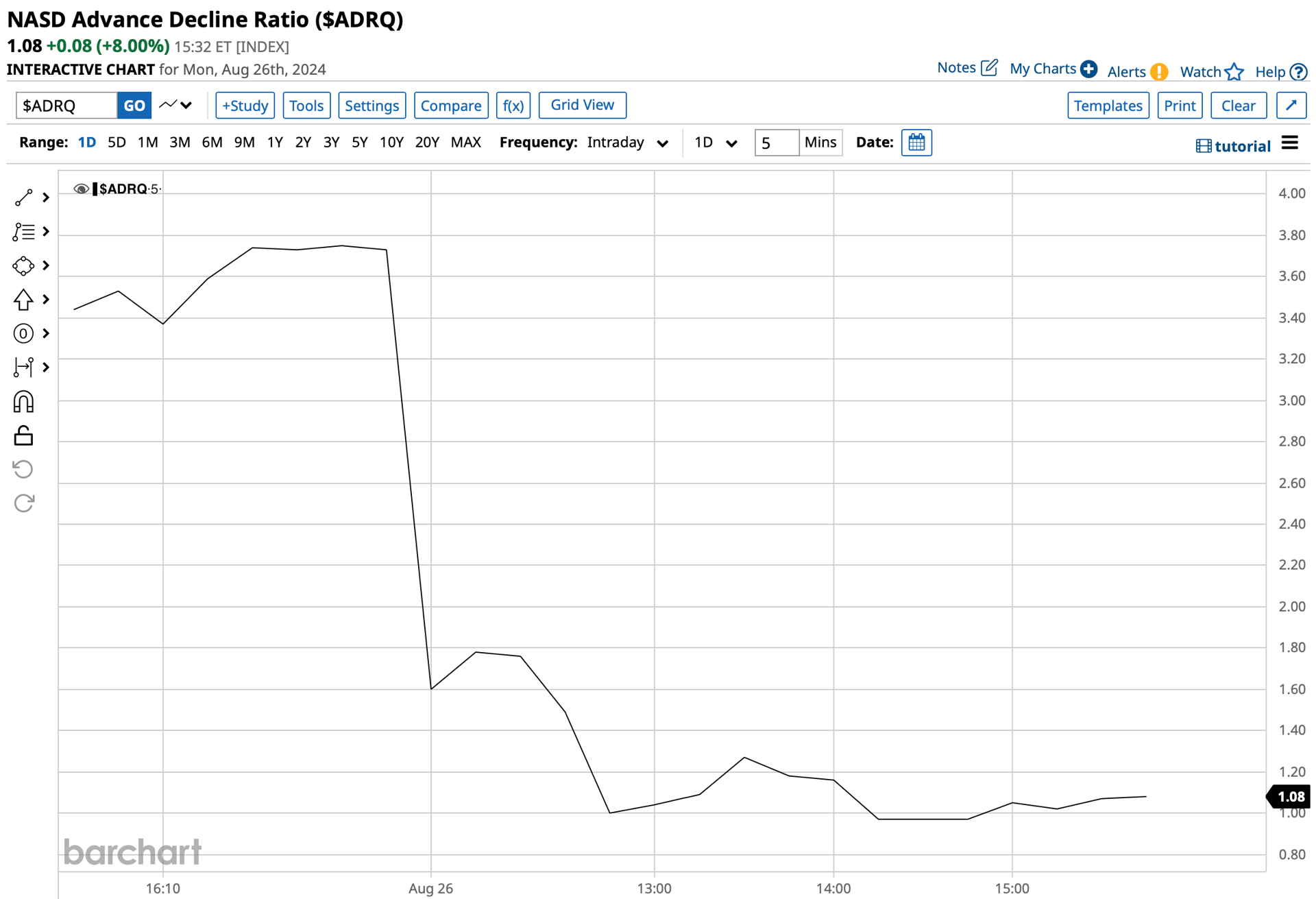

As of 11:00 a.m.:

BY Doug Kass · Aug 26, 2024, 11:40 AM EDT

First thing was a big rotation out of technology into financials.

Then tech recovers a bit and money comes out of financials (look at the intraday of Berkshire BRK.A BRK.B and JPMorgan JPM as an example).

Above-average cash reserves are recommended to home gamers in this swiftly changing complexion.

BY Doug Kass · Aug 26, 2024, 11:26 AM EDT

Adding to shorts - FRHC and SBUX.

BY Doug Kass · Aug 26, 2024, 11:10 AM EDT

Wolf Street howls about the data mess: "The Data Mess. Markets, Interest Rates & Inflation and There’s Still No Recession; Risks of Financialization & Overleverage | Wolf Street"

BY Doug Kass · Aug 26, 2024, 11:00 AM EDT

There is a massive rotation out of technology today - with algos and machines on overdrive.

I remain short QQQ.

BY Doug Kass · Aug 26, 2024, 10:55 AM EDT

I added to my Apple AAPL short this morning.

BY Doug Kass · Aug 26, 2024, 10:41 AM EDT

Adding back to private equity shorts after having reduced on weakness recently:

* Moved from small sized to very small sized...

* (BX) (-$6.28) at $135.85

* (KKR) (-$4) at $119.51

* (APO) (-$9) at $116.30.

I plan to reshort on any strength!

Position: Short BX (VS), KKR (VS), APO (VS)

Aug 1, 2024 1:54 PM EDT

BY Doug Kass · Aug 26, 2024, 10:25 AM EDT

I am converting my short SPY/QQQ common (put on in premarket trading) into short calls for October.

BY Doug Kass · Aug 26, 2024, 10:13 AM EDT

I shorted more BRK.B, TOL, DHI and SBUX this morning - mostly on the opening.

BY Doug Kass · Aug 26, 2024, 9:43 AM EDT

Opco not ready to 'jump on the bandwagon' and pitch Starbucks shares CMG Oppenheimer says shares of Starbucks (SBUX) are up 22% since announcing Brian Niccol as its new CEO. The "prompt re-rating" is justified even though the near-term share performance is likely to be dislocated from fundamentals, the analyst tells investors in a research note. While Niccol brings an "all-star track record," there are "stark contrasts" between the challenges and opportunities he inherited at Chipotle (CMG) versus Starbucks, contends the firm. Opco is now "more positively biased" on Starbucks, but isn't ready to "jump on the bandwagon" and pitch the stock at current levels on Niccol's history alone, particularly with risks to Street's 2025 estimates "still lurking." As such, it keeps a Perform rating on the shares.Note: I plan to move from small sized to medium sized in SBUX short - at prices higher than $94-$95.

Chewy price target raised to $30 from $28 at Morgan Stanley Morgan Stanley raised the firm's price target on Chewy to $30 from $28 and keeps an Overweight rating on the shares. While being "tactically balanced into the print," as material margin upside is offset by elevated revenue expectations, the firm says in its preview that it sees clear upside opportunity on the EBITDA path and expects "another material beat & raise." Pet ownership appears to be stable quarter-over-quarter, but not yet inflecting, notes the firm, which continues to expect net adds to return positive in Q3 and raised its FY24 and FY25 EBITDA estimates by 3% and 2%, respectively.

BY Doug Kass · Aug 26, 2024, 9:35 AM EDT

BY Doug Kass · Aug 26, 2024, 9:18 AM EDT

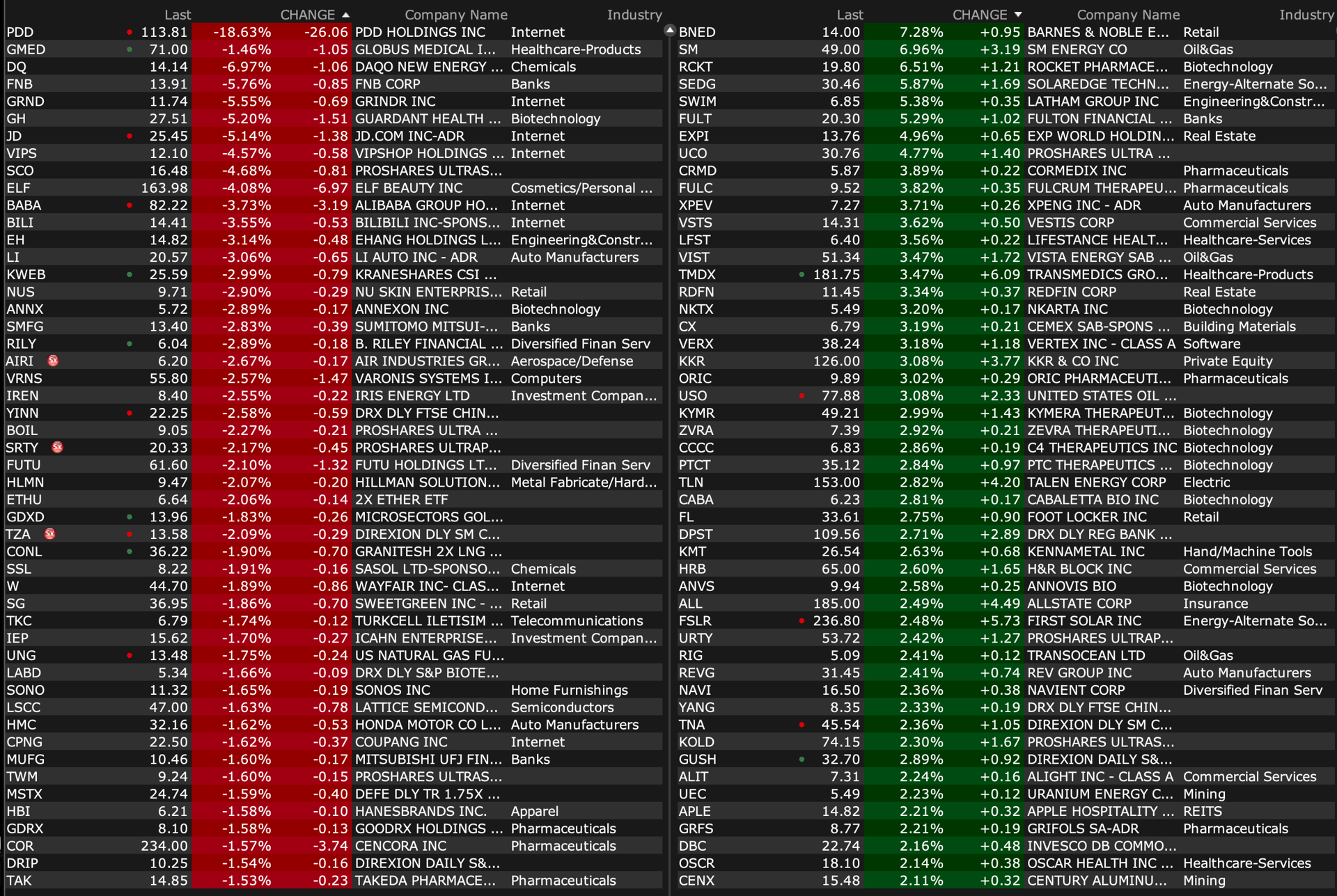

Upside:

-MIRA +48% (achieves 100% reversal of neuropathic pain with Oral Ketamir-2)

-TNXP +18% (to collaborate with Bilthoven Biologicals on advancing development of Tonix’s Mpox vaccine, TNX-801)

-ALZN +6.8% (plans to replace a 300 mg TID lithium carbonate dose for treatment of BD with a 240 mg TID AL001 lithium equivalent, which represents a daily decrease of 20% of lithium given to a patient and anticipate ALZN002 Phase I/IIA study will resume in 4Q24)

-SEDG +6.0% (Zvi Lando steps down as CEO, effective immediately)

-VCEL +5.5% (announces FDA approval and commercial availability of MACI Arthro)

-XPEV +4.3% (Chairman Xiaopeng He purchases 1M Class A shares at average price HK$27.13/shr)

-BGNE +4.2% (BGB-16673 receives U.S. FDA Fast Track Designation for CLL/SLL)

-RDHL +4.1% (receives US FDA Orphan Drug Designation for Opaganib for treatment of neuroblastoma)

-RYTM +4.0% (US FDA accepts for Priority Review IMCIVREE (setmelanotide) sNDA in patients as young as 2 years old)

-ML +2.8% (announces $20M share repurchase program)

-PBR +2.3% (Morgan Stanley Raised PBR to Overweight from Equal Weight, price target: $20 from $18)

-NSSC +2.0% (earnings)

Downside:

-PDD -17% (earnings, color; Company says it is not a time for share repurchases or dividends)

-DQ -6.5% (earnings, guidance)

-GH -6.1% (files for $400M common stock offering)

-RILY -3.0% (discloses Nasdaq's Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard)

-BABA -2.6% (lower in sympathy following PDD earnings)

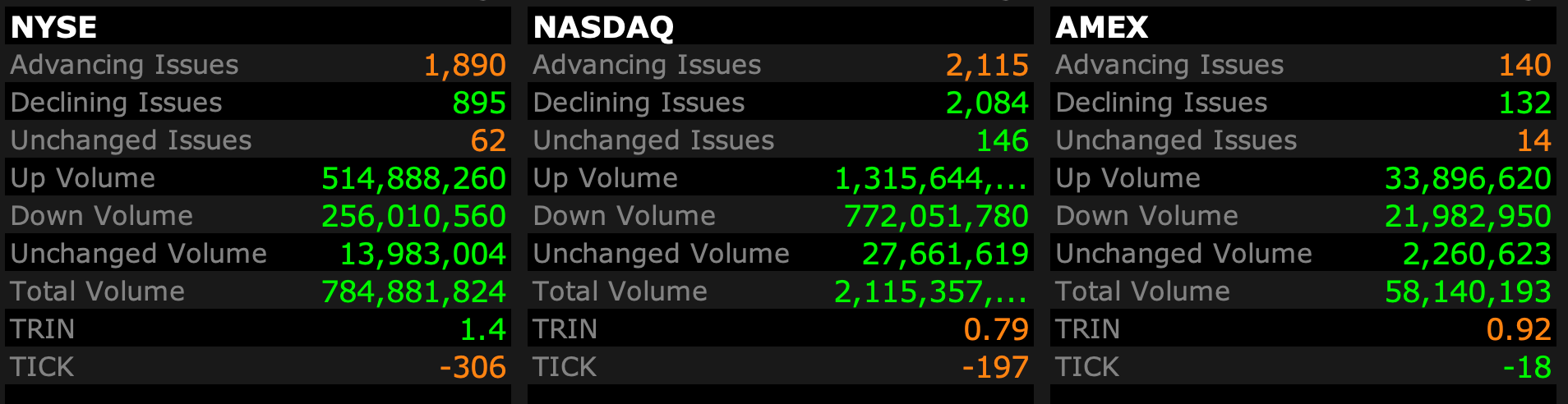

BY Doug Kass · Aug 26, 2024, 9:08 AM EDT

As of 8:55 a.m.:

BY Doug Kass · Aug 26, 2024, 9:00 AM EDT

BY Doug Kass · Aug 26, 2024, 8:45 AM EDT

From Peter Boockvar:

As still a shareholder (we and I) of Live Nation, I decided to do some due diligence Friday night and drove to Philly with my son to see Bruce Springsteen. According to my channel check, the live music business continues to be a solid contributor to the growth of the US economy, and globally as well, in what I continue to refer to as a very mixed and uneven economic situation.

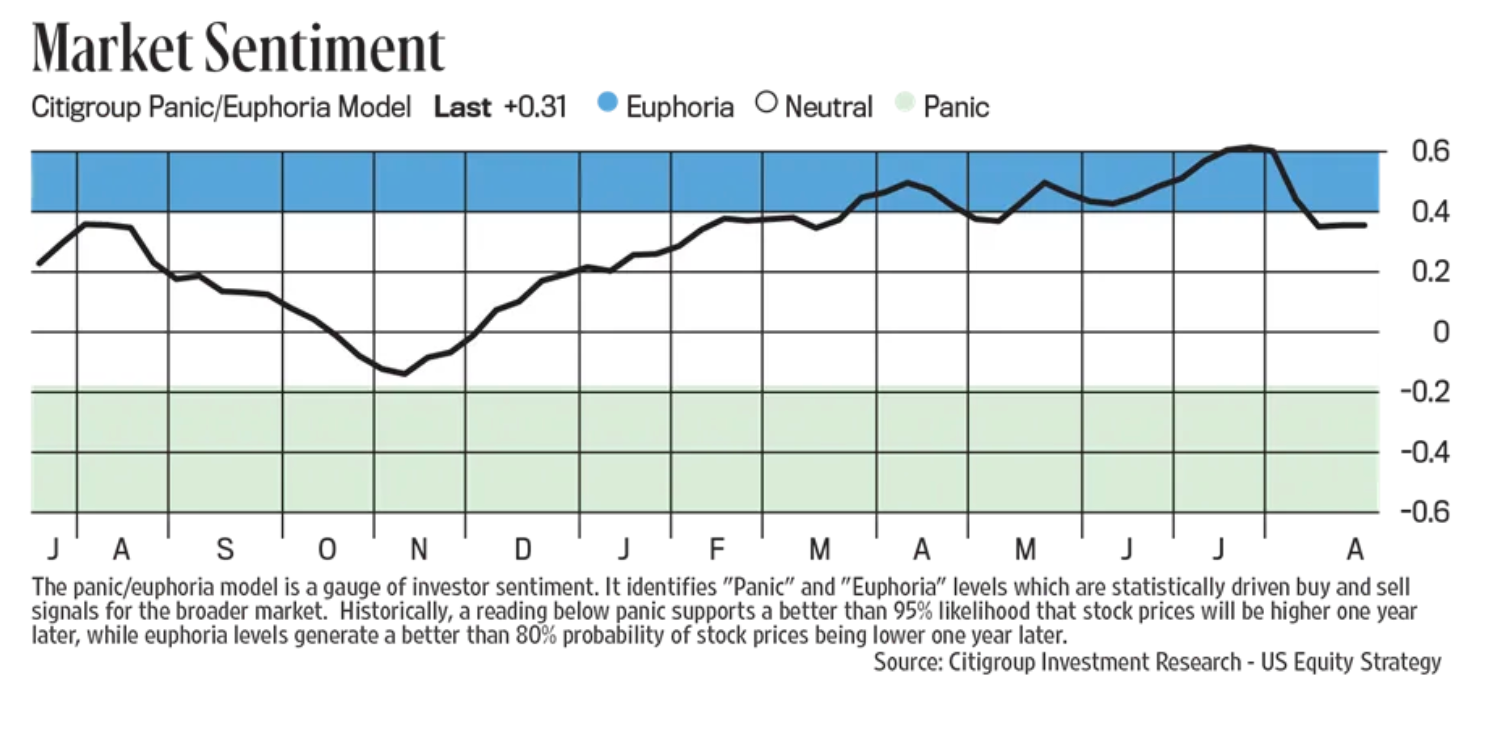

Here is an update on the Citi Panic/Euphoria index that I saw over the weekend which reflects some cooling from the extreme Euphoria seen in the mid part of July. With the rebound in stocks, I expect it to tick up again this week just as the II and AAII sentiment gauges have.

The August German IFO business confidence index fell to 86.6, the lowest since February from 87 in July but that was a touch above the estimate of 86. Both components were down slightly m/o/m. The IFO sounded pretty dour by saying “The German economy is increasingly falling into crisis.” The manufacturing component fell to the lowest level since soon after Covid hit and the services side declined to the weakest since February. Trade was up a bit while construction was unchanged.

Nothing market moving here as we know the German economy is under pressure, seeing no growth. The ECB next meets on September 12th and rate cut odds for another 25 bps are 100%.

BY Doug Kass · Aug 26, 2024, 8:30 AM EDT

And energy stocks are rallying in the premarket — with OXY (the recent object of my affection) now trading at $58. (I anticipate an amended Berkshire filing tonite or tomorrow).

BY Doug Kass · Aug 26, 2024, 8:17 AM EDT

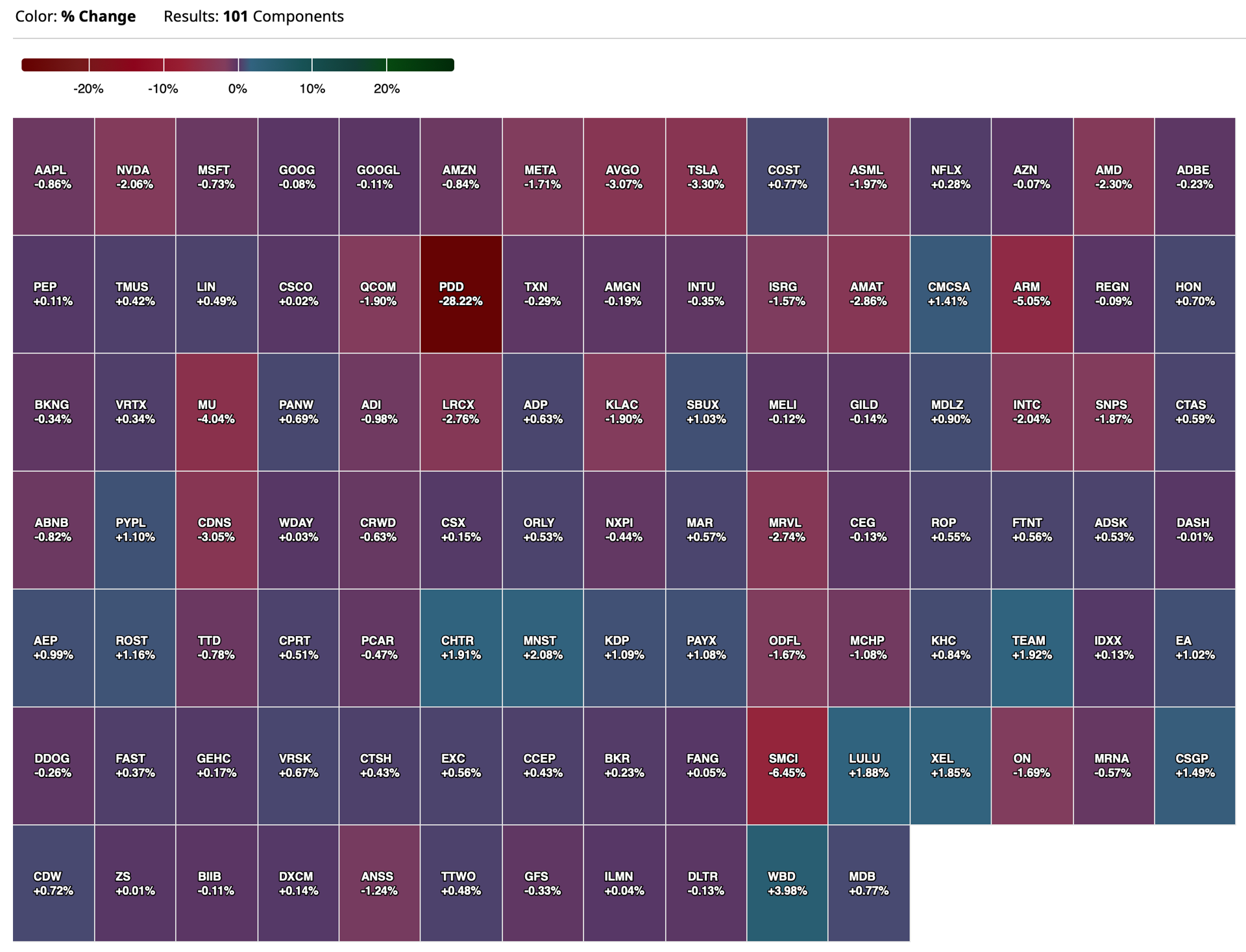

A Chinese company, PDD Holdings PDD, reported poor results.

Its shares are -15%.

PDD represents about 5% of Meta's META ad business.

This helps to explain the modest weakness (-$3/share) in META shares in premarket and the slight fall back in Nasdaq futures.

BY Doug Kass · Aug 26, 2024, 7:20 AM EDT

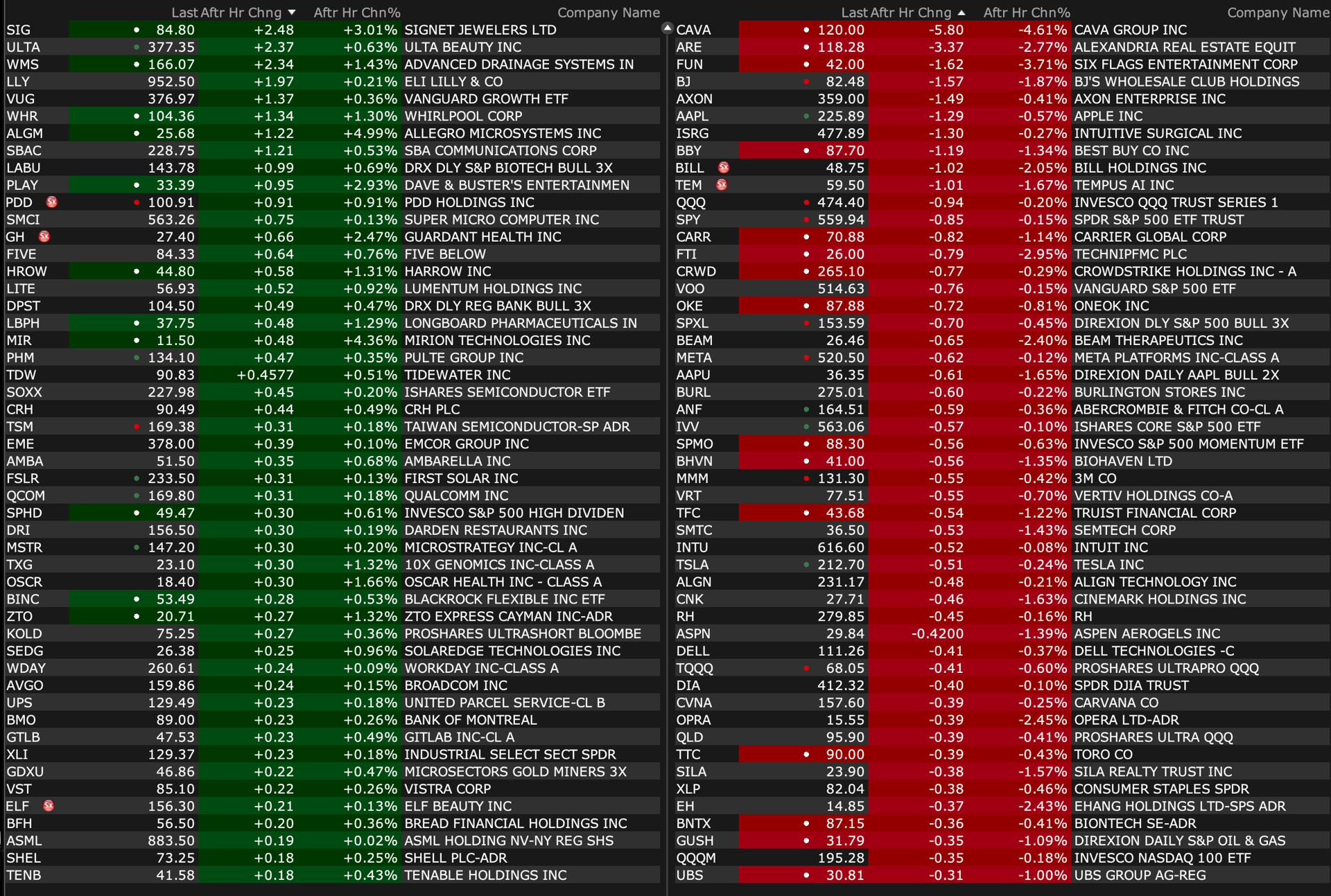

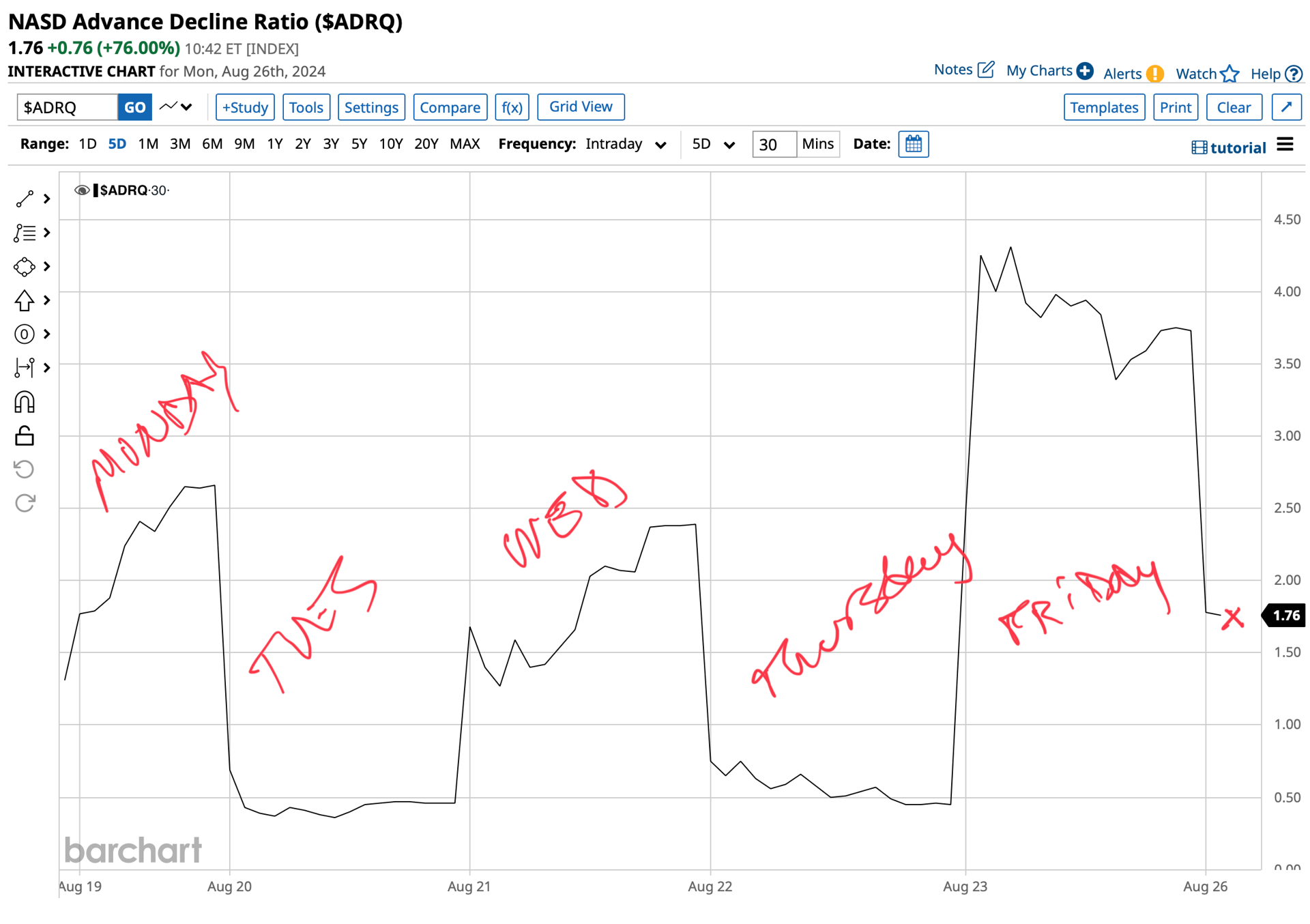

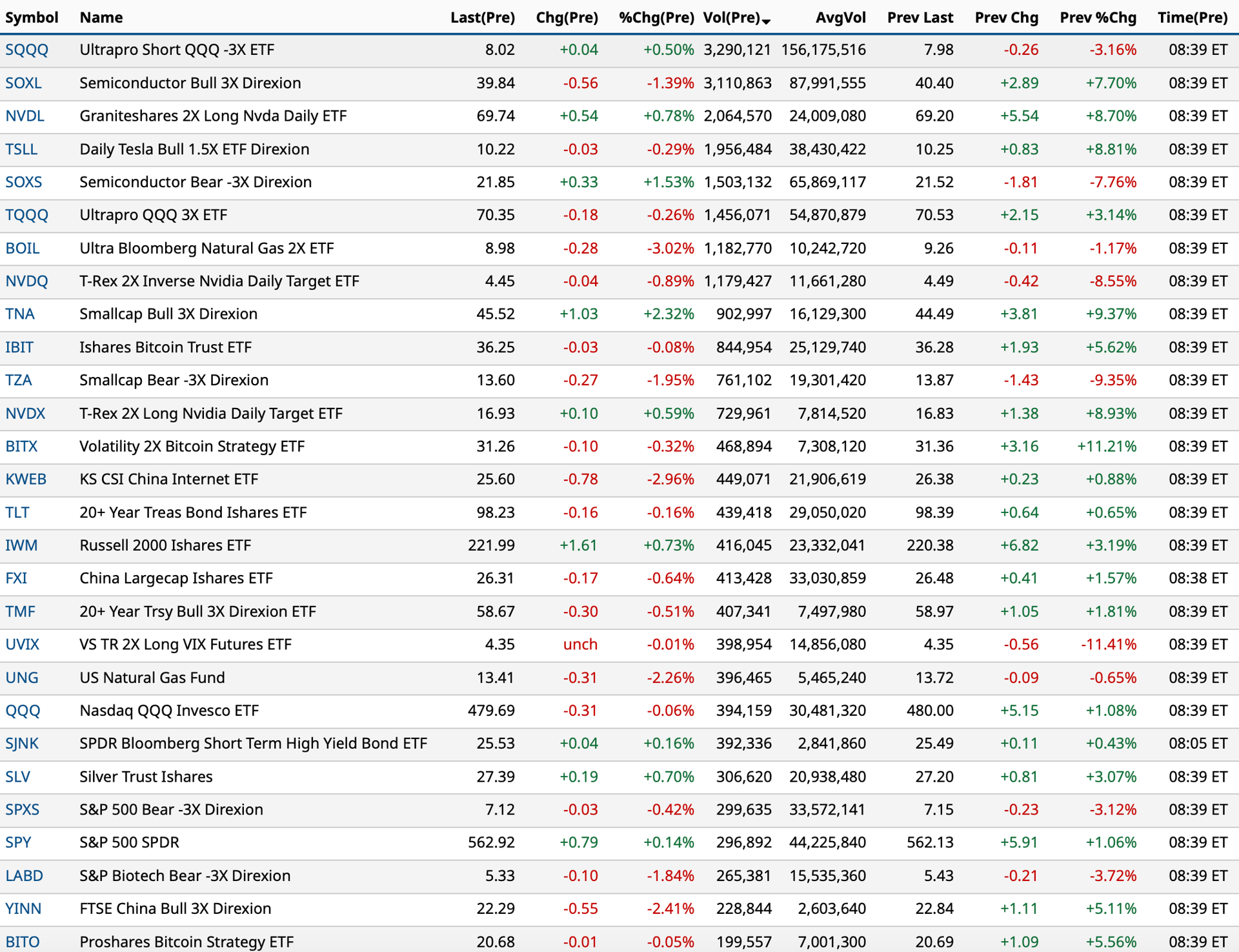

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Aug 26, 2024, 7:12 AM EDT

BY Doug Kass · Aug 26, 2024, 7:02 AM EDT

I am back short Index common (SPY/QQQ) — albeit a very small amount:

* Shorted SPY $563.18

* Shorted QQQ $481.21

BY Doug Kass · Aug 26, 2024, 6:50 AM EDT

Another tweet from the lynx-eyed Larry McDonald:

BY Doug Kass · Aug 26, 2024, 6:40 AM EDT

From JPMorgan:

US: Futs are higher to start the week with small-caps outperforming. Pre-mkt, NVDA (+94bps) is leading both Mag7 and Semis higher as bond yields continue to decline as yield curve bull steepens. USD is flat and commodities are bid with both Energy and Metals stronger, some of this may be a response to a spike in geopolitical tensions over the weekend. The macro data focus is on Durable/Cap Goods but NVDA earnings on Weds is the key event. Powell’s dovish Jackson Hole speech should give a tailwind to risk assets this week.

and...

EQUITY AND MACRO NARRATIVE: Last week, SPX added 1.5% given the consumer earnings releases and macro data (PMI-Srvcs and Claims) were supportive of growth trends but the biggest catalyst was Powell’s presentation at Jackson Hole confirming that September will begin the easing cycle. The market responded positively to Powell’s message and Friday’s price action was representative of a short squeeze with things such as ARKK, KRE, and JPM High Short Interest all moving multiple standard deviations and the SPX adding 1.2%. The index is now 0.6% below all-time highs but has been unable to hold the 5,600 level in previous attempts. In terms of all-time highs, NDX is 4.8% away and RTY is 10% away after adding 1.1% and 3.6% last week, respectively. These prices moves occurred with low liquidity, as last week was the lowest volume week of the year.

Powell’s speech is an important pivot for the markets and has re-installed the Fed Put. The quote that stood out to me the most, “It seems unlikely that the labor market will be a source of elevated inflationary pressures anytime soon. We do not seek or welcome further cooling in labor market conditions.” I interpret this as the Fed is now solely focused on full employment and with the unemployment rate at 4.3%, the market may need to look at 4.5% as being the line of demarcation between the predicted easing cycle and a far more aggressive Fed. With Fed Funds at least 200bps above the Taylor Rule-implied neutral rate, Feroli sees the Fed easing 125bps this year and then a 25bps cut cadence into summer 2025. Does inflation matter? No. Core inflation is mostly linked to a strong labor market and with loosening there and declining wage growth the Fed has told us it no longer considered that a concern even if we have 1-2 months of elevated inflation over the medium-term. Some additional color is in the Jackson Hole section below.

· US MKT INTEL – we sent the below to IB chats immediately after Powell’s speech

o This feels like the Fed’s current concern is one-sided and that is for the labor markets. The 25bps or 50bps debate may make markets choppy over the next few weeks but the direction is higher for Equities. The focus should be on real yields which are roughly in line with levels experienced last summer at the end of the hiking cycle. While some cracks began to form in the economy, the Fed may be able to fix those and get growth to resume higher. Why? The consumer still sits on a significant amount of cash. While the consumer is getting choosier with its spending patterns, that consumption is not declining [I have a lot of info on this topic for clients who care].

o Where from here? I think new ATHs and could get a significant boost from NVDA next week with all Mag7 names below their ATH highs and the group about 8% below ATHs. The biggest risk comes from the negative Sept seasonality and the traditional vol increase/market weakness witnessed in Sept/oct for election years. Neither candidate represents an unknown so maybe we see less of that phenomenon this year.

o What would I own? Barbell and I know that this is a broken record. Mag7, Semis, Banks, Credit Cards, Autos/Suppliers, Homebuilders, and Transports are my core thinking. Long IWM as a ‘Texas hedge’. I think it is difficult to see small-caps outperform for more than a 4-8 week basis [I am aware you can drive a truck through that spread] but foresee a near-term environment that makes RTY more attractive that SPX; 40% of RTY are unprofitable companies and think they squeeze from here plus spicier parts of the market. Keep an eye on international names, too as USD weakness will invite geographic diversity. DXY made a 52-week low on Friday.

o ADDITIONAL THOUGHTS (Aug 25) – What are the risks from here? NVDA, Positioning, Seasonality, and the US Election. (i) NVDA – there is color in the remaining sections. (ii) Positioning – it does not appear that we have re-grossed to level seen before the downturn from mid-July to early-Aug and across the Street it appears that aggregate TMT positioning is UW the sector which may mean that the risk/reward from NVDA is skewed to the upside. (iii) Seasonality – this century, September has been the worst month of the year averaging -1.7% return (54% hit rate) followed by Q4 being the best time of the year averaging +4.2% (79% hit rate) but if you look at only the last five years, the SPX averages -4.2% (80% hit rate) and Q4 averages +9.8% (100% hit rate). 2024 has not followed 5-year nor 10-year seasonal trends with each month ex-January delivering either a directional or magnitude surprise; (iv) US Election – election years tend to extend the negative September seasonality into October due to policy uncertainty. With both candidates known to markets, it is possible that this effect is muted this year and if the polls/betting markets support either a Blue Wave or Red Wave then look for markets to pre-trade this but would think it wise to withhold until after the Sep 10 Presidential Debate and subsequent polling. Our team will have more details on the election in early September but do let us know if there topics you would like to see addressed. (v) Geopolitics – the situations in both the Middle East and Ukraine have been largely ignored by Equity markets but keep an eye on events that draw either the US or Turkey (NATO) into either conflict. Bullish commodity bets may be the most prudent hedges.

BY Doug Kass · Aug 26, 2024, 6:29 AM EDT

"A bad day for the ego is a good day for the soul."

- Robin Sharma

Bonus — Here are some great links:

BY Doug Kass · Aug 26, 2024, 6:17 AM EDT

Monday

Tuesday

Wednesday

Thursday

Friday

BY Doug Kass · Aug 26, 2024, 6:05 AM EDT

From Charlie:

BY Doug Kass · Aug 26, 2024, 5:55 AM EDT

BY Doug Kass · Aug 26, 2024, 5:45 AM EDT

The embedded tweet could not be found…