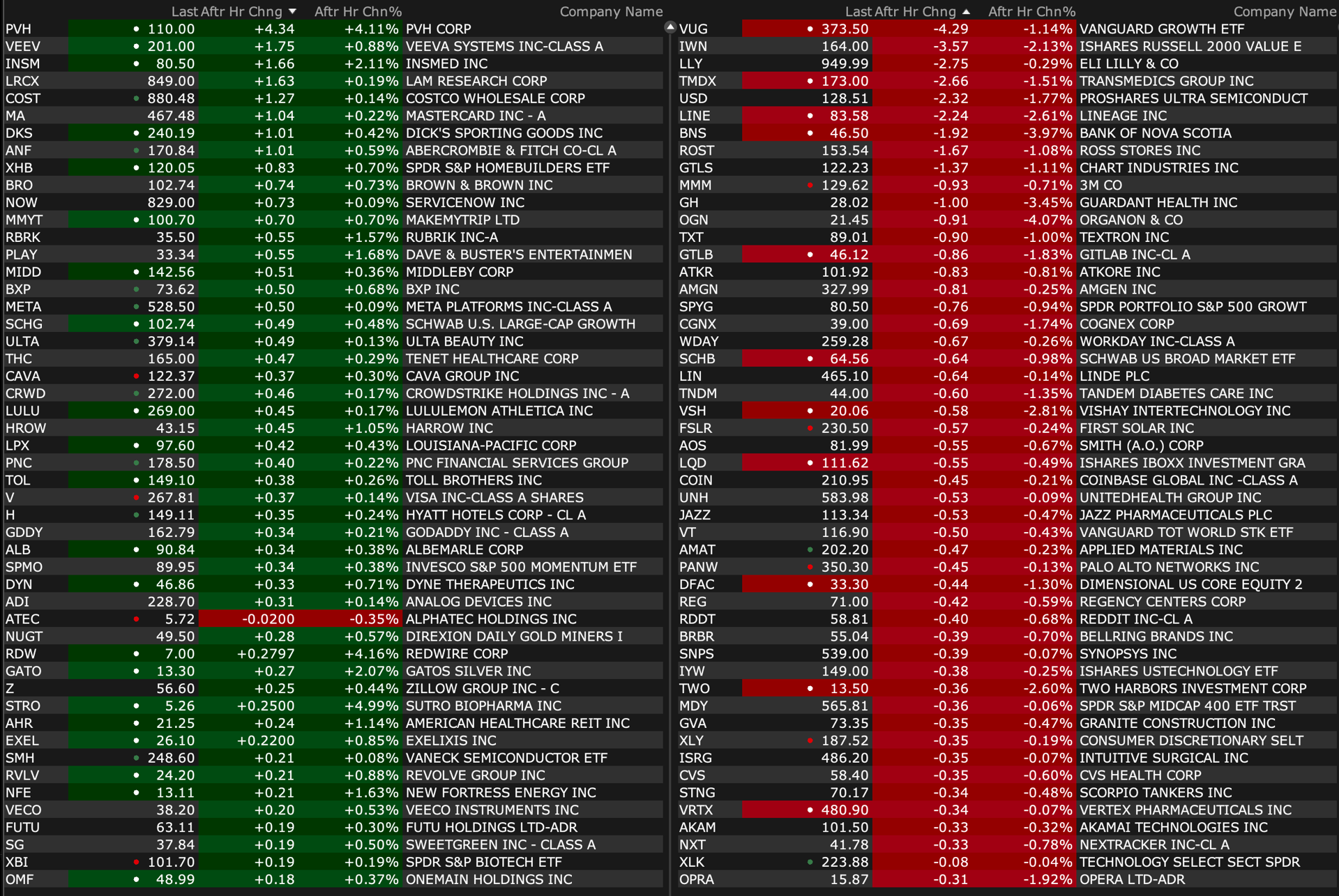

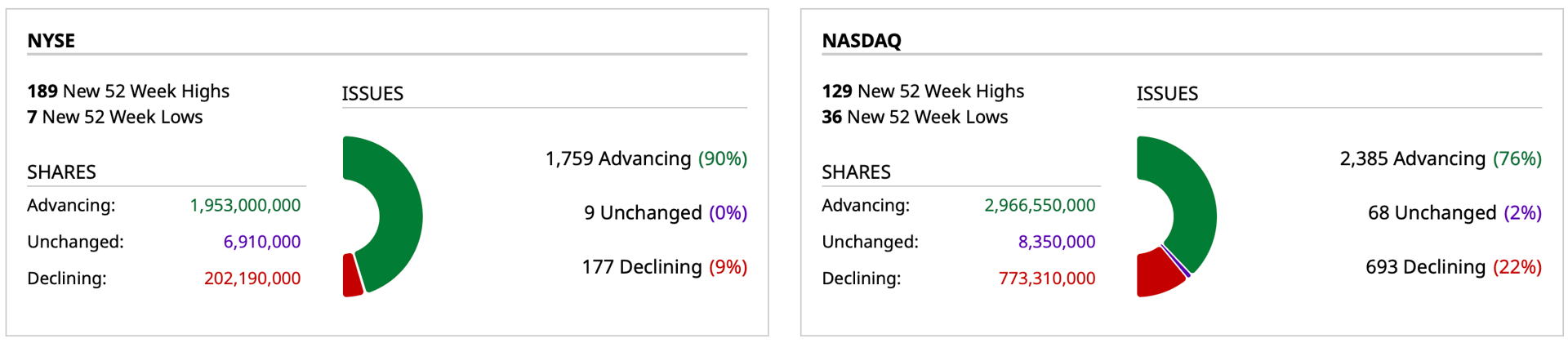

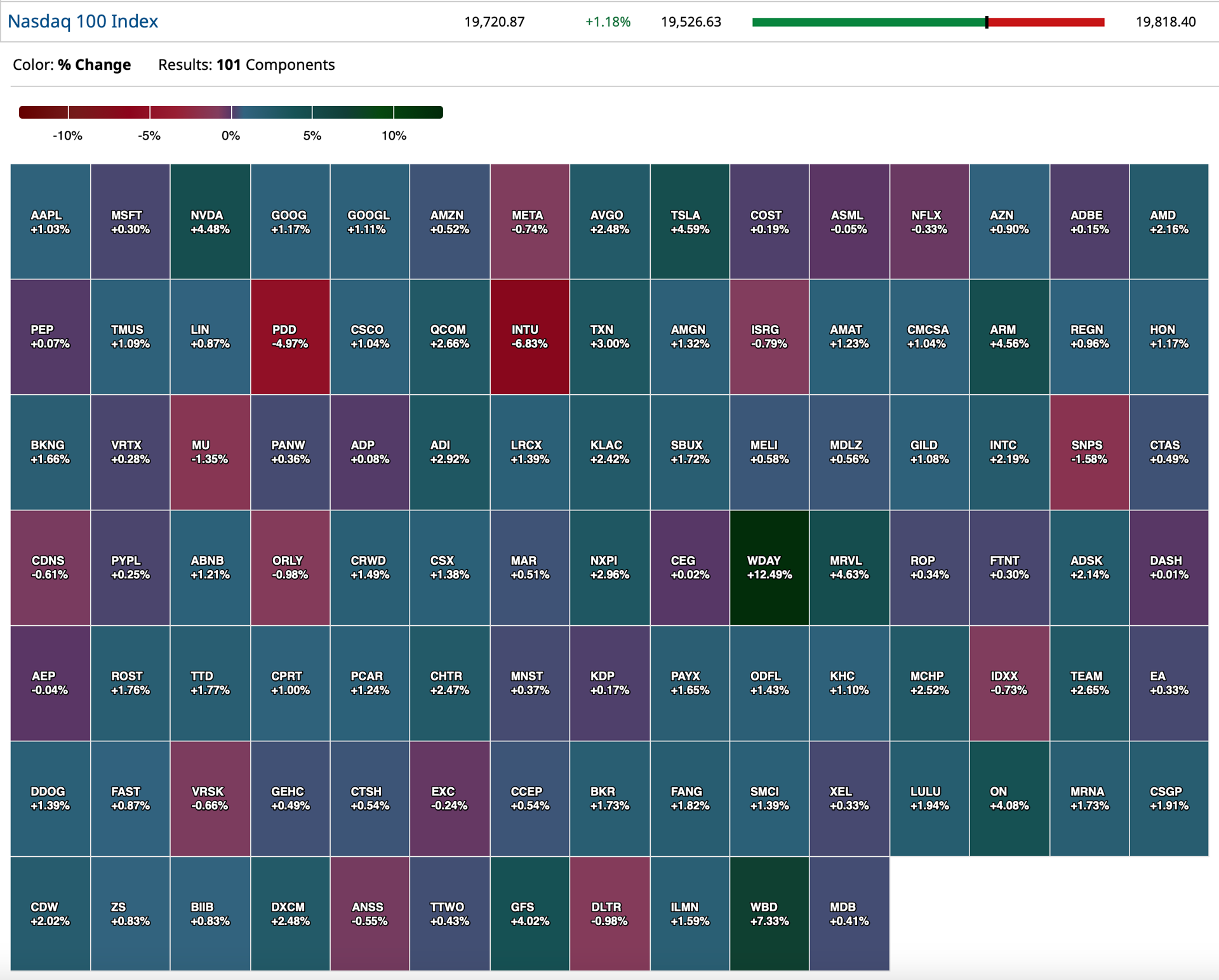

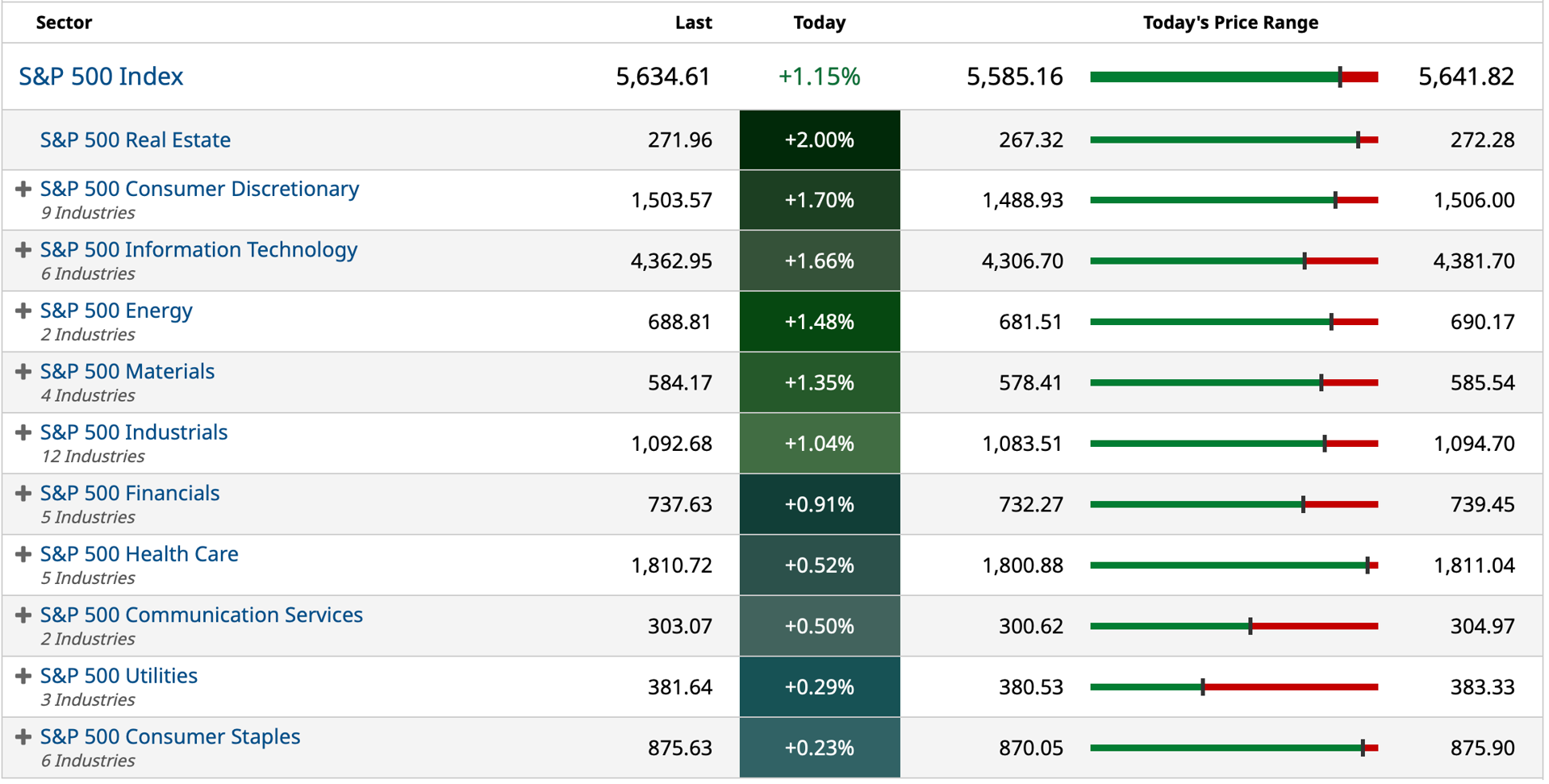

After Hours Movers as of 4:22PM

BY Doug Kass · Aug 23, 2024, 4:31 PM EDT

BY Doug Kass · Aug 23, 2024, 4:31 PM EDT

BY Doug Kass · Aug 23, 2024, 4:29 PM EDT

I am going to leave a bit early to get some rest as I am still jet lagged.

Thanks again to the lynx-eyed Sarge, Chris, Mesh and Bret who filled in my absence.

It is nice to be back and I hope you enjoyed reading my Diary over the last three days.

Enjoy the weekend.

Be safe.

BY Doug Kass · Aug 23, 2024, 3:12 PM EDT

BY Doug Kass · Aug 23, 2024, 2:57 PM EDT

BY Doug Kass · Aug 23, 2024, 2:05 PM EDT

BY Doug Kass · Aug 23, 2024, 1:50 PM EDT

BY Doug Kass · Aug 23, 2024, 1:34 PM EDT

For the third straight day I am seeing a large buyer in Occidental Petroleum OXY.

Just...

*All you gotta do is...

Wishin' and hopin' and thinkin' and prayin'

Plannin' and dreamin' each night of his charms

That won't get you into his arms

So if you're lookin' to find love you can share

All you gotta do is hold him, and kiss him and love him

And show him that you care

-"Just Wishin' and Hopin'," Dusty Springfield

Volume is now coming into Occidental Petroleum.

BY Doug Kass · Aug 23, 2024, 1:22 PM EDT

BY Doug Kass · Aug 23, 2024, 1:00 PM EDT

From Peter Boockvar:

Positives

Negatives

BY Doug Kass · Aug 23, 2024, 12:42 PM EDT

So far, so good...

BY Doug Kass · Aug 23, 2024, 12:20 PM EDT

BY Doug Kass · Aug 23, 2024, 12:04 PM EDT

On the rally (S&P cash now +59 handles), I added to my short SPY/QQQ calls.

BY Doug Kass · Aug 23, 2024, 11:49 AM EDT

I am further reducing my GOOGL, AMZN, JOE and ARM longs now.

BY Doug Kass · Aug 23, 2024, 11:20 AM EDT

Covers on SPY and QQQ were $558.44 and $476.73, respectively.

BY Doug Kass · Aug 23, 2024, 11:05 AM EDT

The S&P cash has dipped by over 30 handles in the last 15 minutes.

I have taken my profit in my SPY and QQQ common short.

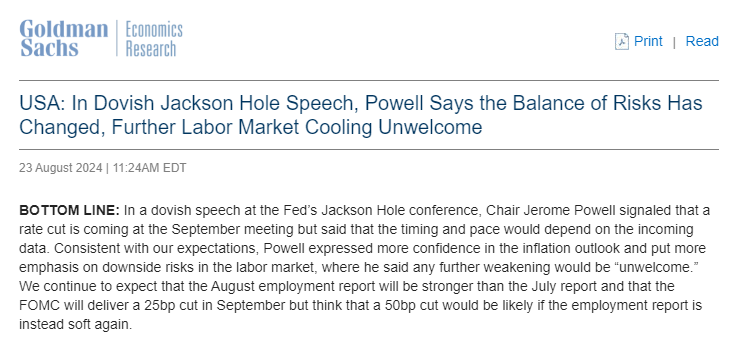

BY Doug Kass · Aug 23, 2024, 11:00 AM EDT

The bottom line to the Powell speech: “The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.”

Emphasizing their shift in attention to the labor market, this was then followed by, “We will do everything we can to support a strong labor market as we make further progress toward price stability… The current level of our policy rate gives us ample room to respond to any risks we may face, including the risk of unwelcome further weakening in labor market conditions.”

In other words, any aggressive rate cutting cycle from here, rather than methodical and measured, will be because the economy and labor market deteriorates. Either way, with 100 BPS of cuts priced in through year end followed by another 100 BPS priced in through next August, nothing here should be a market surprise, though we see the initial stock market reaction is excitement. The two-year yield, however, is little changed in response.

BY Doug Kass · Aug 23, 2024, 10:40 AM EDT

BY Doug Kass · Aug 23, 2024, 10:33 AM EDT

With S&P cash up by over 65 handles, I am entering my second tranche of shorts now.

BY Doug Kass · Aug 23, 2024, 10:21 AM EDT

I am building up my short book on this morning's gap higher.

Adding to the following shorts:

* AAPL $227.21

* TOL $145.14

*DHI $189.01

* SPY $559.63

* QQQ $479.12

New trading short rentals:

* JPM $217.57

* BRK.B $452.19

BY Doug Kass · Aug 23, 2024, 10:01 AM EDT

BY Doug Kass · Aug 23, 2024, 9:25 AM EDT

BY Doug Kass · Aug 23, 2024, 9:20 AM EDT

BY Doug Kass · Aug 23, 2024, 9:15 AM EDT

From Peter Boockvar:

I try to put myself in Powell's shoes and I don't expect anything special today from him. It could be a non-event in terms of market moves. He'll reaffirm market expectations of a September rate cut by again highlighting their shift in focus to the labor market but with more data to absorb before then, he'll have no interest in leaning into what extent they will cut. As for market expectations, past that of a full 100 BPS by year's end and 200 BPS by next year's Jackson Hole confab, why would he pre-commit to anything today? "Play it by ear from here," I believe is his thought process.

This all said, if he talks down the odds of 50 BPS next month by reinforcing his confidence in the economy, regardless of the CPI and payroll data he'll see soon, we'll get a selloff in the short end and likely in stocks.

More relevant maybe for the markets is what BOJ Governor Ueda said overnight to a parliamentary session in Japan. Notwithstanding the market earthquake a few weeks ago, Ueda blamed worries about the U.S. economy for the selloff, and not the BOJ rate hike, as it came coincident with the rise in U.S. jobless claims and weak July payroll print. He also said there is "no change to the BOJ's basic stance to adjust the degree of monetary easing if it became convinced that economic and price developments were moving as forecast... Japan's short-term rates are very low. If the economy is in good shape, they will move up to levels deemed neutral."

He did, though, acknowledge the markets response to their rate hike and yen rally and said, "We will watch financial markets with an extremely high sense of urgency for the timebeing."

So, the BOJ remains a maybe factor I believe and is looking to raise rates again likely this year. The yen is up and JGB yields are lower in response. The Nikkei, though, is up too, by .4%.

Also a factor was the July Japan CPI figure where the headline gain held at 2.8% year over year, one-tenth more than expected. Boosting it was the lack of utility subsidies which resulted in a jump in electricity prices. The core/core rate was higher by 1.9% year over year as expected. With a benchmark rate of just .25%, Ueda does need to raise again, however slow and measured the pace might be. The 10-year inflation breakeven was up by 1 BP to 1.37%, but below where it was right before the rate hike when it was around 1.50%.

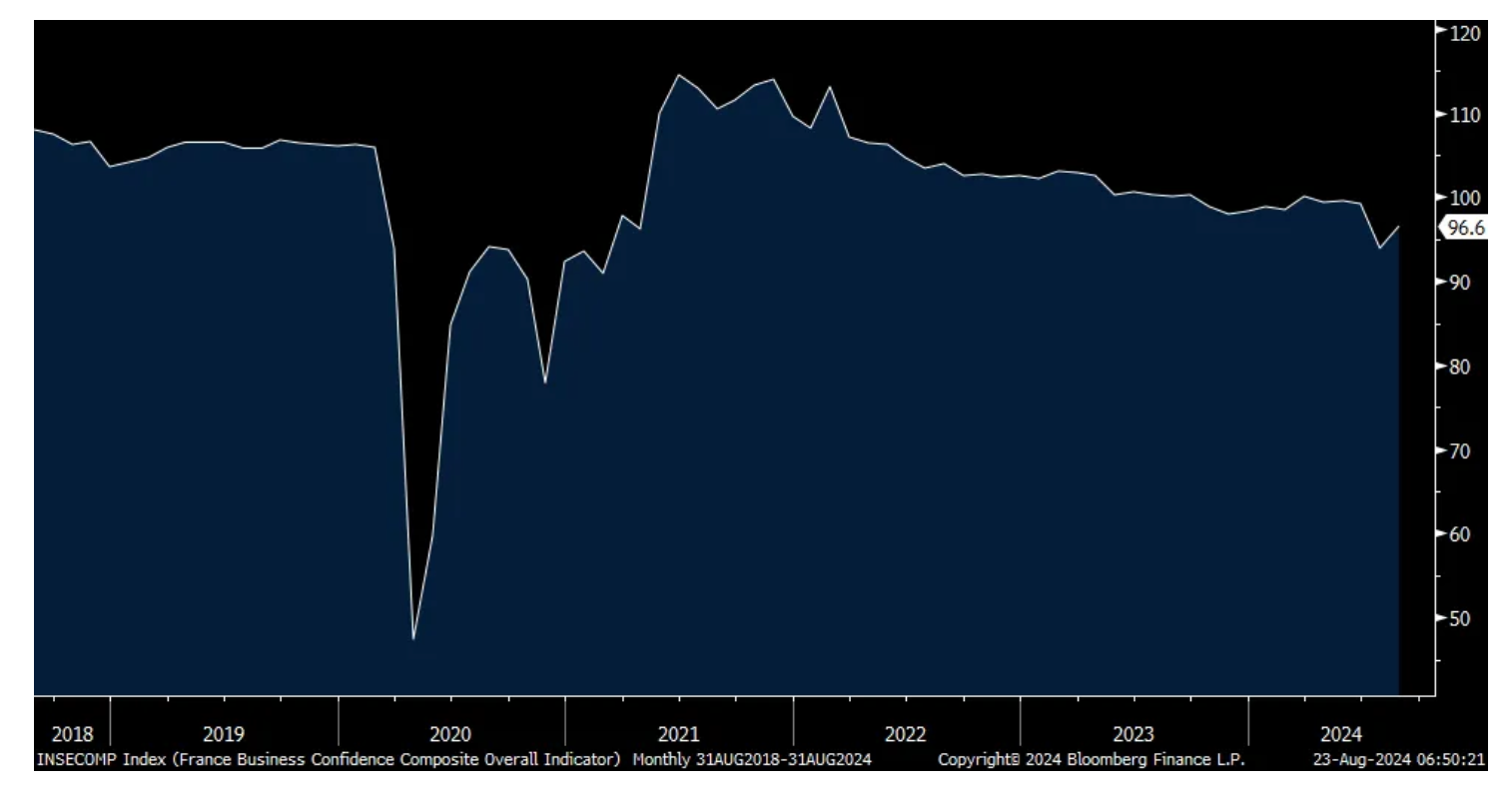

French Business Confidence

Likely capturing the Olympics' sugar high, French business confidence in August rose to 97 from 94 (influenced by the election chaos) and that was one point above the estimate. But, it was 99.1 in June. All components rose month over month, including manufacturing, services, retail, employment and construction. While not market moving, the euro and European stocks are higher while bond yields are little changed.

Earnings Calls

On to the earnings calls, where the unevenness and fragility in the U.S. economy remains apparent and at least in retail, "value" is the hot buzzword, as said yesterday.

From Ross Stores ROST, where comps grew by 4%:

The comp was "driven by a combination of higher traffic and basket size."

"Cosmetics and children's were the strongest merchandise areas during the quarter, while geographic performance was broad based."

On the outlook, "our low to moderate income customers continue to face high costs for necessities, pressuring their discretionary spending. Looking ahead, our prior year sales comparisons also become more challenging during the second half of the year amidst an external environment that is highly uncertain. As a result, we continue to maintain a cautious approach in forecasting our sales."

"We recognize that delivering the great values that our off-price customers have come to expect from us is more important than ever, especially given the continued pressures they face from the high cost of necessities."

From Williams Sonoma WSM, whose comps fell 3.3%:

"There is no doubt that the home furnishings market is challenged due to the uncertainty in the economy, coupled with slow housing. This leads us to believe that we may not see the back-half acceleration that we expected, despite all of the hard work we've done to improve our product offer and our customer experience. Therefore, we believe it is prudent to reduce our top-line outlook for the balance of the year while continuing to deliver on our commitment to profitability, and in fact, we are raising our bottom line guidance."

From Cava CAVA, who continues to perform with a similar model as Chipotle that includes generous portions where a customer $1 goes a long way relative to other QSR peers:

"CAVA was one of just a handful of publicly traded restaurant brands with positive traffic growth in the second quarter, and we believe our performance is a reflection of our unique and compelling value proposition."

"At a time when consumers are increasingly feeling the pressure of an uncertain economy, and are more discerning about where and how they spend their money, they are choosing to dine at CAVA."

"Consumers have been frustrated and fatigued by higher prices over the past few years. In this post-high inflationary environment, traditional full-service chains are struggling to deliver a compelling value proposition, while conventional fast-food chains have raised prices at a faster rate, driving the perception that they have become too expensive... Our value proposition lies in the quality of our food, the relevance of our differentiated Mediterranean cuisine ... the convenience with which our guests can access that cuisine in our multi-channel format, and the experience they have when they engage with our brand and our hospitality."

From Advance Auto Parts AAP, whose comps rose .4%:

"During the second quarter, our frontline team navigated a weak demand environment as consumers continued to feel the weight of an uncertain macroeconomic climate."

"DIY remained pressured but improved sequentially... The macro environment is challenging, retailers are lowering expectations, and we're starting from a lower baseline relative to the industry."

"In terms of cadence for the second quarter trends started off soft and improved as we moved through the quarter with the benefit of the tailwind from hot weather related sales and our strategic actions to drive growth among the pros."

On guidance, "We expect consumer related headwinds related to maintenance deferrals, lower discretionary spending to impact our trajectory in the short-term. With respect to quarter-to-date trends, both our pro and DIY businesses have started off weaker, driven by the overarching macro pressure on the consumer, tougher prior year comparisons, and diminishing weather related tailwinds exiting Q2."

With regards to Workday WDAY, whose stock is rallying sharply after earnings, I pulled this macro comment out of its call as we all watch the labor market with greater scrutiny right now:

"We continue to see the macro environment consistent with our last quarter, including moderated headcount growth within our customer base. And, as we discussed last quarter, we expect these trends to continue."

BY Doug Kass · Aug 23, 2024, 8:28 AM EDT

* Market interpretations will vary

* Whether Thursday's market reversal was a change in market character will only be known with the benefit of hindsight

* Goldilocks thinking may be wrong-footed — that fairy tale's outcome (like a further continuation of the bull market) may not occur with the ease in which so many investors now posit

* I am of the view that downside market risks now dwarf upside market rewards

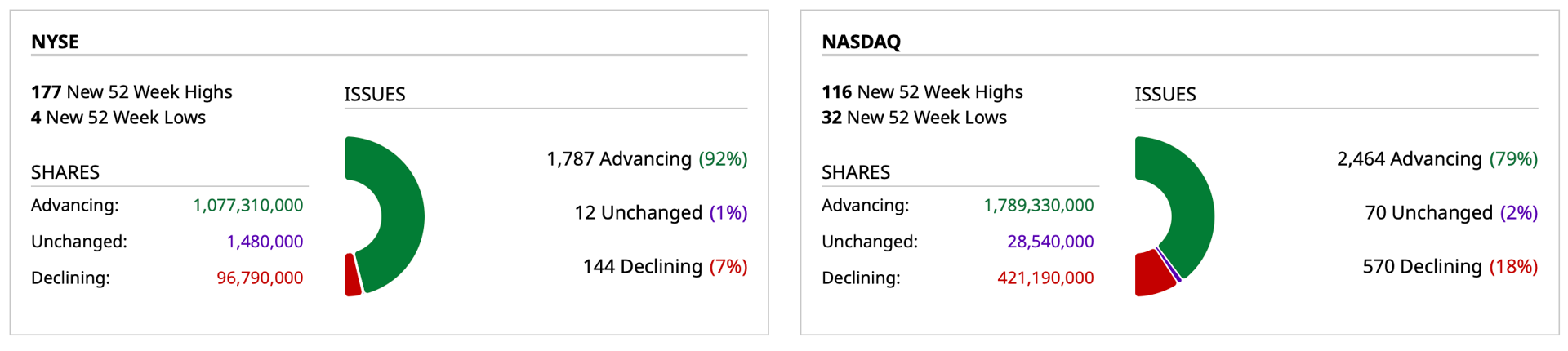

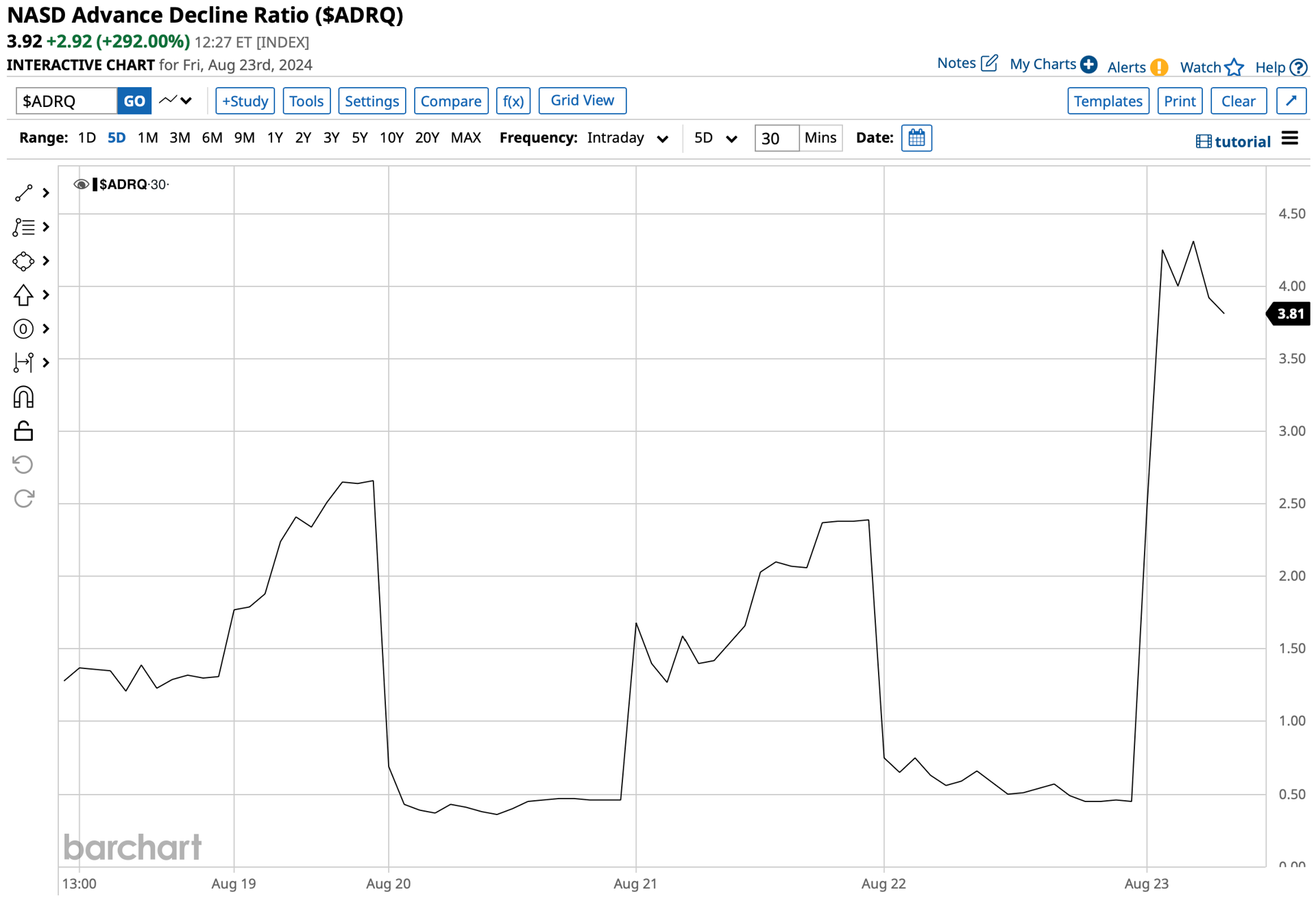

We will only know with the benefit of hindsight whether yesterday's price action was a change in market character.

Nonetheless, today (in the business media) we will watch "talking heads" state with confidence their views as to the significance of the market's recent volatility and downside action on Thursday.

As for me, I am often wrong and always in doubt — I will not pretend that I have a special stock market crystal ball.

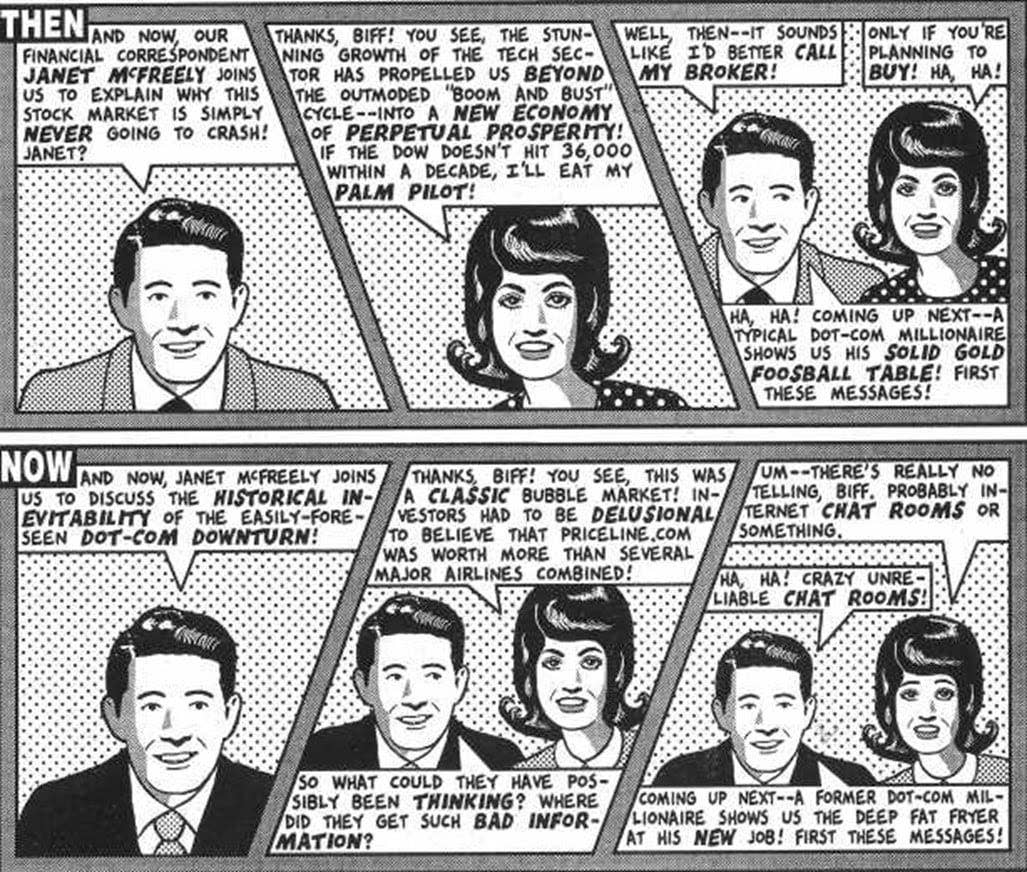

As we learn from reading Howard Mark's recent commentary, "Mr. Market Miscalculates":

"The non-linear nature of this process suggests something very different from rationality is at work. In particular, as in many other aspects of life, cognitive dissonance plays a big part in investors’ psyches. The human brain is wired to ignore or reject incoming data that is at odds with prior beliefs, and investors are particularly good at this."

Howard goes on:

"Further complicating things in terms of rational analysis is the fact that most developments in the investment world can be interpreted both positively and negatively, depending on the prevailing mood.

"Another classic cartoon sums up this ambiguity in fewer words. It’s highly applicable to the market tremor that inspired this memo."

As seen by the above cartoons and witnessed by us daily, market interpretations can vary.

I can't tell you whether the market reversal yesterday represented a bearish engulfing candle:

Or whether Thursday's reversal represented resistance near previous market highs:

Or whether a short-term change in momentum (with several key ETFs [the S&P 500, Nasdaq 100, Semiconductors and Biotech indices] all violated their five-day moving averages on Thursday) has developed.

Or whether Mr. Market was simply overbought and demand for equities were sated:

Or whether yesterday represented a brief respite from a powerful market advance that started in late 2023.

That said, for the multiple reasons mentioned in my Diary over the last few months I continue to view the market as overvalued — a market that has likely already well discounted the likely reduction in interest rates by the Federal Reserve.

In keeping with these views (and given the rise in stock futures overnight) I re-shorted the indices (after covering some of my position in yesterday's schmeissing) in premarket trading:

* SPY at $588.87

* QQQ at $478.26

I am of the view — after the market's recent gold rush — that the upside reward is now dwarfed by the downside risk.

I will end with more pearls from my pal Howard Marks' recent commentary, "Mr. Market Miscalculates":

"Charlie Munger, Warren Buffett’s late partner, routinely quoted the ancient Greek statesman Demosthenes, who said, 'Nothing is easier than self-deceit. For what each man wishes, that he also believes to be true.' One great example is 'Goldilocks thinking': the belief that the economy will be neither strong enough to bring on inflation nor weak enough to lapse into recession. Things sometimes work out that way – as may be the case right now – but not nearly as often as investors posit. Expectations that incline toward the positive encourage aggressive behavior on the part of investors. And if this behavior is rewarded in good times, still more aggressiveness usually ensues. Rarely do investors realize that (a) there can be a limit to the run of good news or (b) an upswing can be so strong as to be excessive, rendering a downswing inevitable.

"For years, I quoted Buffett as having warned investors to temper their enthusiasm: 'When investors lose track of the fact that corporate profits grow at 7% on average, they tend to get into trouble.' In other words, if corporate profit growth averages 7%, shouldn’t investors begin to worry if stocks appreciate by 20% a year for a while (as they did throughout the 1990s)? I thought it was such a good quote that I asked Buffett when he said it. Unfortunately, he answered that he hadn’t. But I still think it’s an important warning.

"That inaccurate recollection reminds me of John Kenneth Galbraith’s trenchant reference to one of the most important causes of financial euphoria: 'the extreme brevity of the financial memory.' It’s this trait that allows optimistic investors to engage in aggressive behavior, untroubled by knowledge of what such behavior led to in the past. Further, it makes it easy for investors to forget past errors and invest blithely on the basis of the newest miraculous development."

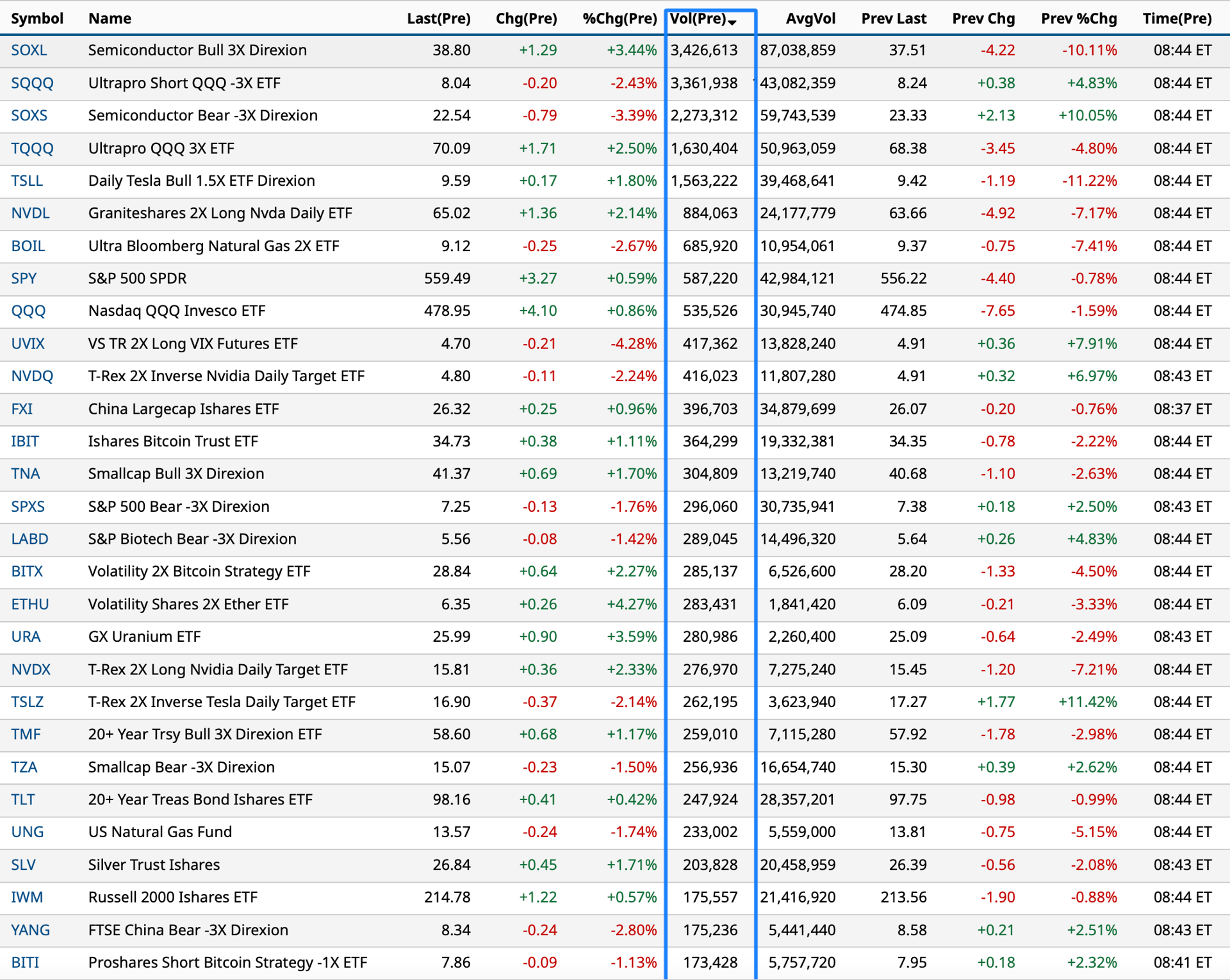

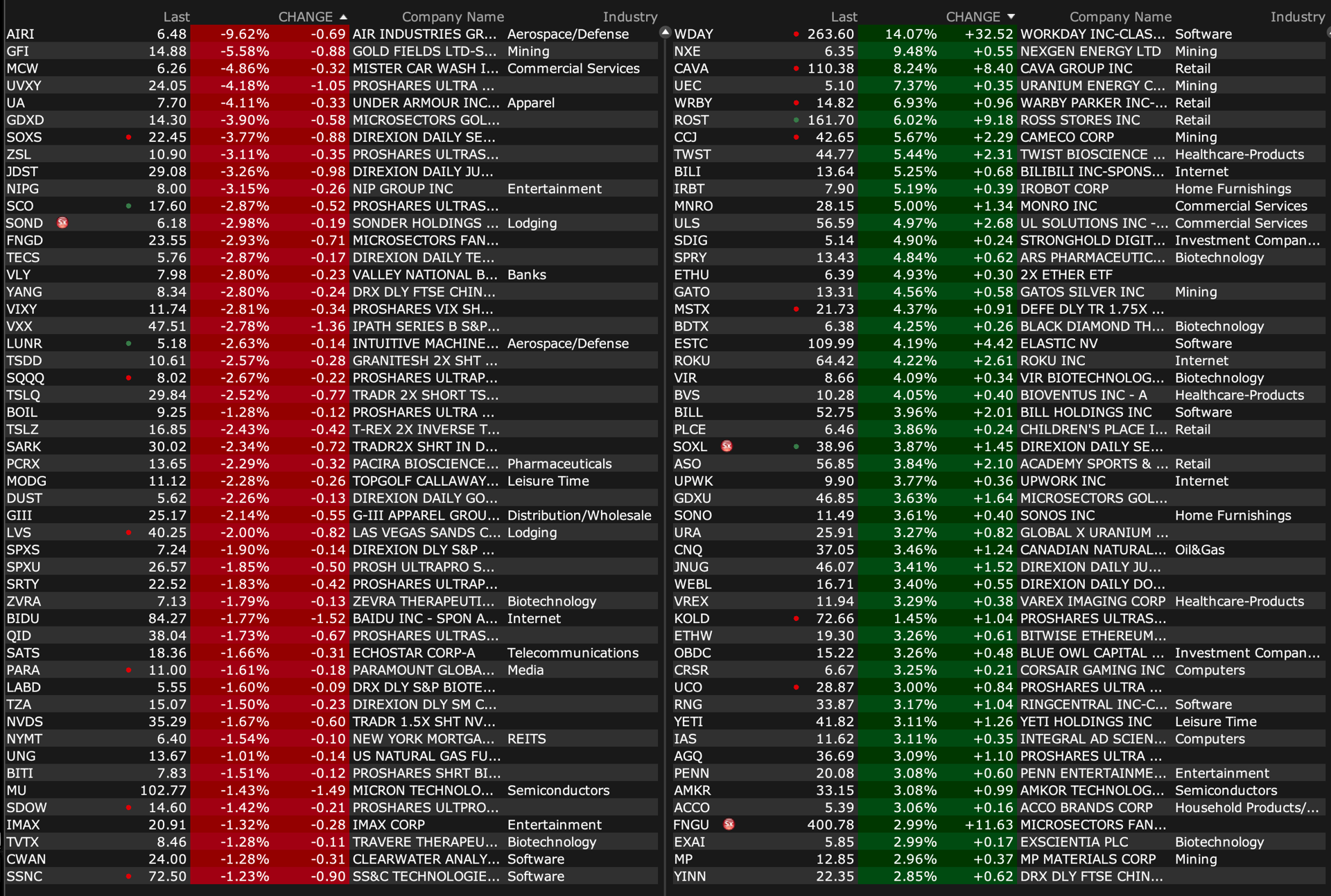

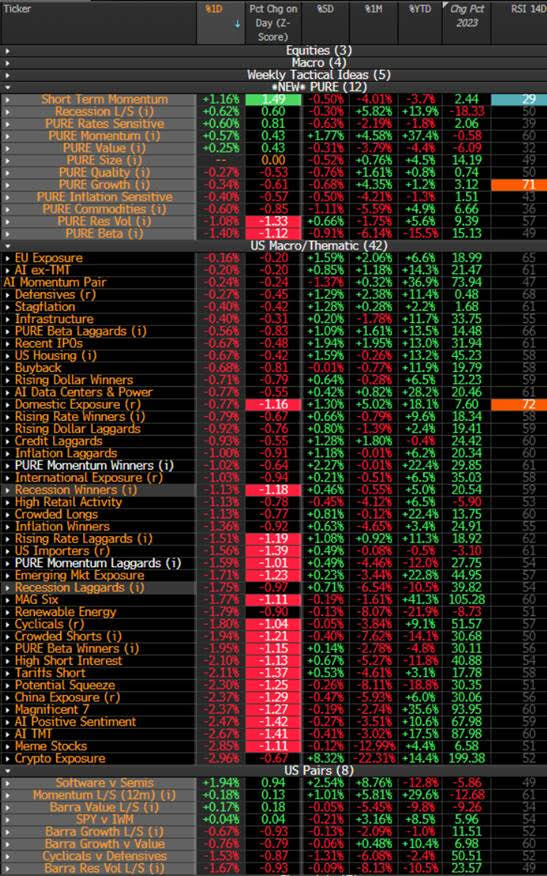

BY Doug Kass · Aug 23, 2024, 7:34 AM EDT

This table is a valuable resource for momentum-based short-term traders:

BY Doug Kass · Aug 23, 2024, 7:04 AM EDT

From JPMorgan:

U.S.: Futs are higher with tech leading. Top performers in mega-cap tech are TSLA (+1.5%), NVDA (+1.2%) and AMZN (+69 bp). Bond yields are higher, and USD is lower; 2-, 5-, 10-year yields are 2 bp, 5 bp, 10 bp higher. Commodities are mixed with oil and precious metals higher, while base metals are lower. Today, the main focus will be Powell’s speech at Jackson Hole (10 a.m. ET).

and...

Equity and Macro Narrative: Yesterday, equities failed to hold 5600 again after the flash PMI and claims releases. On the surface, PMIs is a mixed result with the better-than-expected services prints offsetting some weakness in mfg. Claims prints were largely in line with expectations and the stabilization in claims numbers should be a welcome sign for growth. Tech and consumers were the biggest laggards, while energy, RE and financials outperformed. Investors are waiting for Jackson Hole tomorrow (Powell’s speech at 10 a.m. ET). While it seems unlikely that Powell will offer much new information on rate cut expectations, given the lack of macro catalysts this week, we may still see some price action around hawkish/dovish tilt from Powell. In addition, after Monday’s rally, the SPX is now inching towards its ATH and trying to stay above 5600. While we still remain our bullish stance, upside could be more limited than before ahead of September 6 NFP as it will be the determinant factor for rate cut and key to assess growth risks.

BY Doug Kass · Aug 23, 2024, 6:53 AM EDT

"There is nothing more deceptive than an obvious fact."

-Sherlock Holmes

Bonus — Here are some great links:

"Bulls Take Off," Bespoke

"The Fed Should Be Forceful Next FOMC Meeting, Says Strategas' Chris Verrone," YouTube

"New Kids on the Blockchain," All Star Charts

"15 Ways to Lose Money in the Markets," A Wealth of Common Sense

BY Doug Kass · Aug 23, 2024, 6:36 AM EDT

My first recommendation to a young person trying to learn the investment business is to read everything you can:

BY Doug Kass · Aug 23, 2024, 6:15 AM EDT