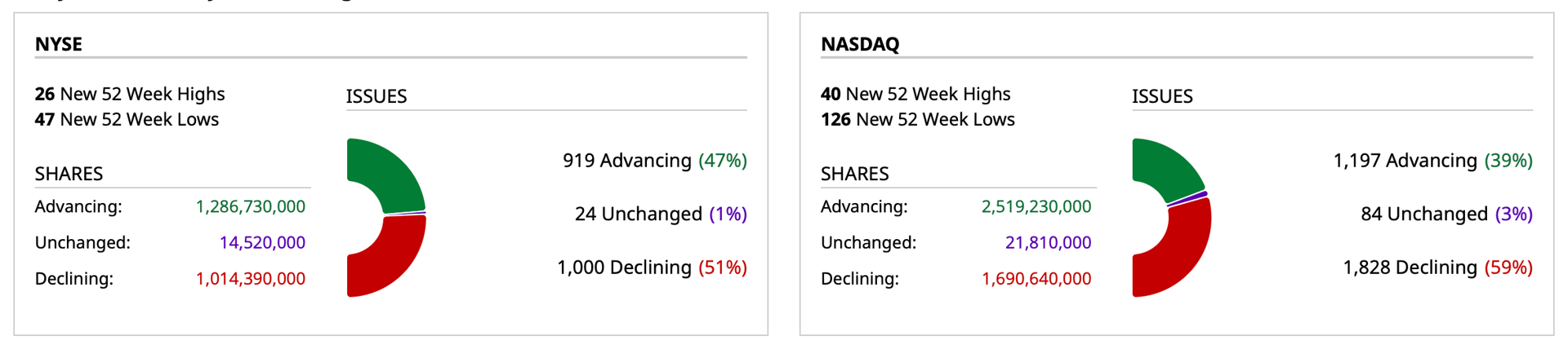

Closing Market Internals

Same as before. Averages higher breadth weak.

Closing Breadth

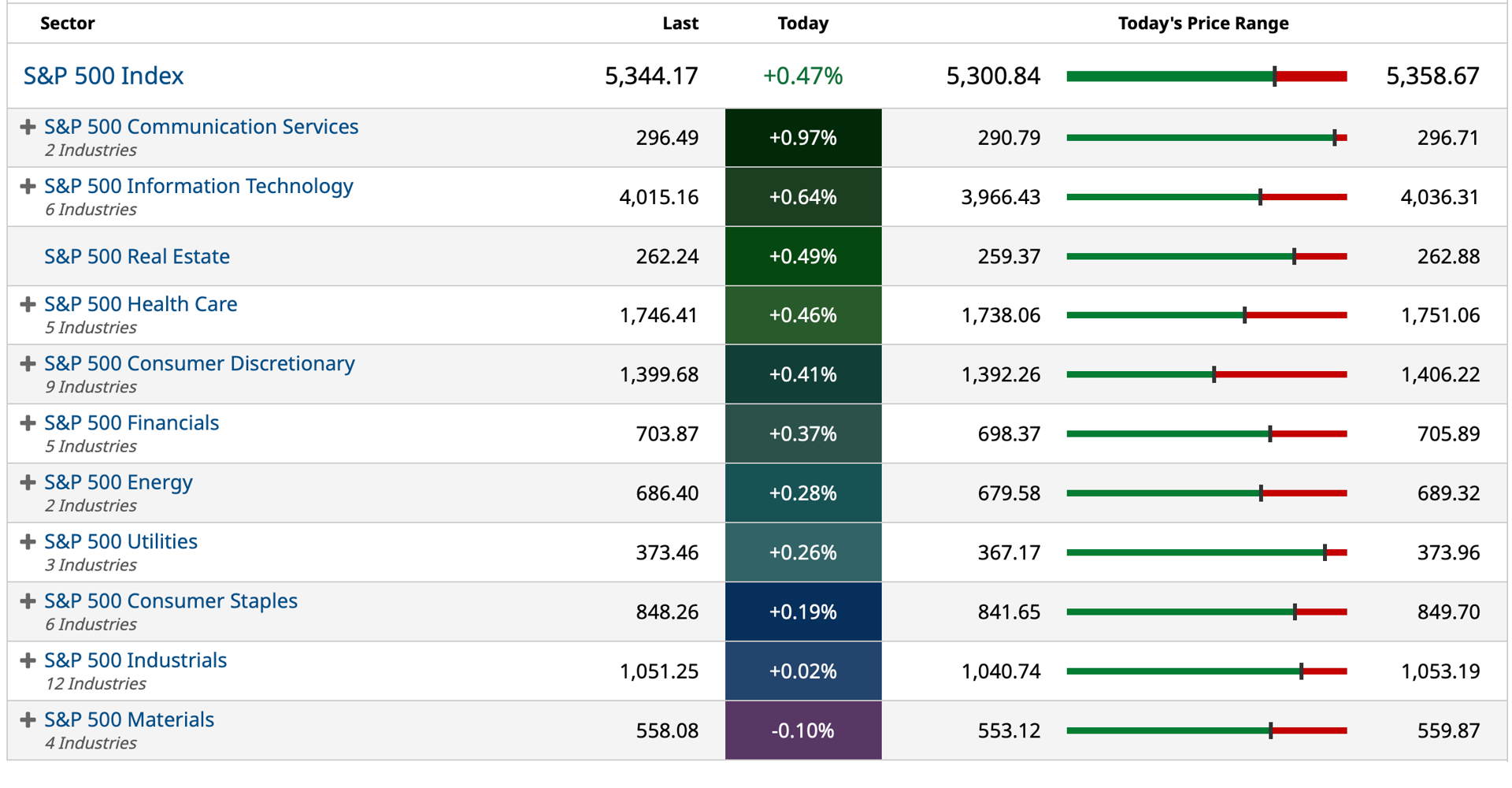

S&P 500 Sectors

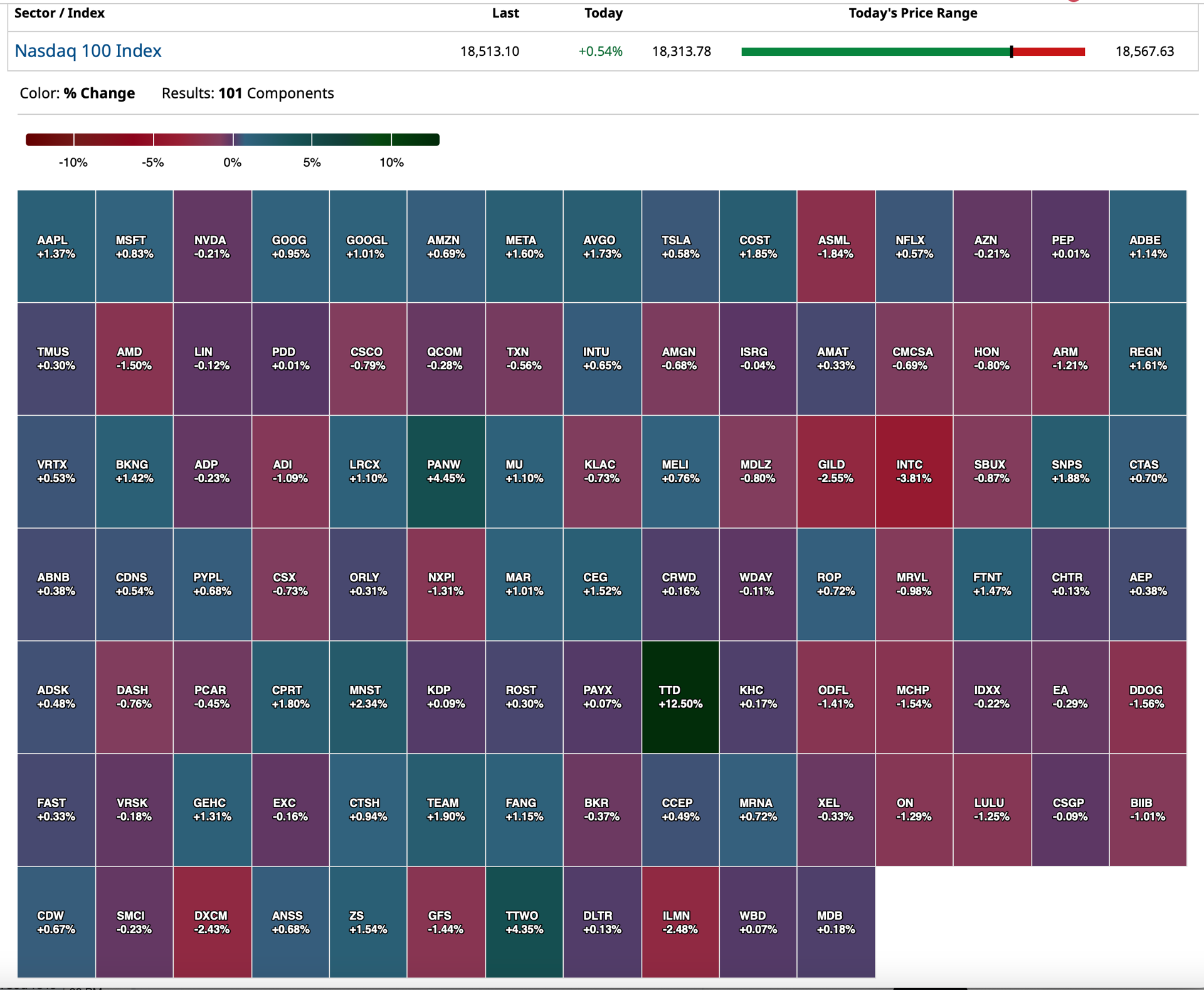

Nasdaq 100 Heat Map

BY Doug Kass · Aug 9, 2024, 4:37 PM EDT

Same as before. Averages higher breadth weak.

BY Doug Kass · Aug 9, 2024, 4:37 PM EDT

I am outta here early.

Thanks for reading my Diary today and all week.

Enjoy the weekend.

Be safe.

BY Doug Kass · Aug 9, 2024, 3:05 PM EDT

Professor Scott Galloway's No Mercy No Malice: "Weapons of War: Higher Ed".

BY Doug Kass · Aug 9, 2024, 1:35 PM EDT

This has been one of those uncommon days in which I have not made a trade as I prepare for my excursion to Europe.

BY Doug Kass · Aug 9, 2024, 1:06 PM EDT

From The Credit Strategist:

BY Doug Kass · Aug 9, 2024, 12:10 PM EDT

Lilly's LLY market cap is up by another +$50 billion today.

If Merck MRK bought Viking Therapeutics VKTX for $15 billion+, its shares would rise by +$25 billion. (imho).

BY Doug Kass · Aug 9, 2024, 11:47 AM EDT

BY Doug Kass · Aug 9, 2024, 11:25 AM EDT

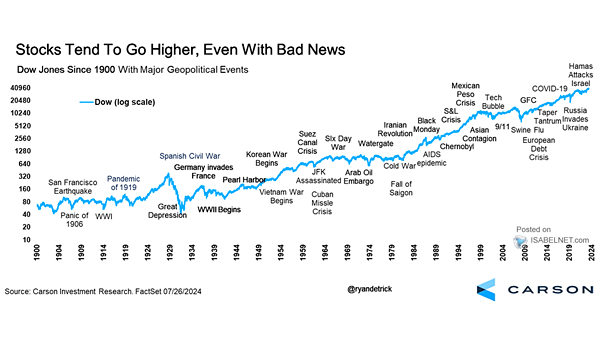

* Stocks tend to rise over time.

* But with rising volatility and (possible) limited market upside (a trading range?) and the short term influence of machines/algos - trading provides an opportunity to supplement investing.

"In the 20th century, the United States endured two world wars and other traumatic and expensive military conflicts; the Depression; a dozen or so recessions and financial panics; oil shocks; a flu epidemic; and the resignation of a disgraced president. Yet the Dow rose from 66 to 11,497."

- Warren Buffett

Yesterday, one of our lynx-eyed subscribers (JSR1111) asked a valid and pointed question:

JSR1111:

Doug I have a question that is meant with the utmost respect….you often mention that you meet with corporate mgt teams in your research endeavors and I wonder why. In recent years you’re much more of a trader (and a good one) than a long term investor. Even when you take positions you initially label as an investment and not a trade, they’re rarely held for very long esp if they appreciate quickly. Unless you find mgt insights that enlightening which I doubt.

JSR's point was well taken as the longer one goes out in time (as an investor), the more likely equities will be rewarding. Stocks tend to recover from adversity and rise over most timeframes:

It is my strong view and investment methodology to combine investing and trading in order to deliver superior investment returns. The benefit of this dual process is to increase your odds for success.

No doubt, during discrete periods of time, investing may produce undesirable results. For example owning/buying Mag 7 and other "compounders" in late 2021, turned out to be a virtual disaster 12 months later. But owning/buying the same in late 2022 delivered extraordinary returns (up to several weeks ago). Where we will be one year from now is anyone's guess!

When of the view that the market is vulnerable, in a trading range or even in a bull market, trading can be a profitable endeavor. It does require a dispassionate approach (e.g. buying stocks earlier this week into the abyss has provided out-sized and quick returns).

To emphasize, I have owned and held short stocks for years but I also try to ring the cash register through trades.

As Warren Buffett famously said, "the stock market is a manic depressive." Indeed, with the proliferation of passive products and strategies market volatility (even on an intraday basis) is likely to rise - providing numerous opportunities for opportunistic traders. And when one has a bonafide sense of "intrinsic value" (with solid security analysis) the disparity between the current stock price (when valued under intrinsic value) provides opportunity to produce excess returns for the courageous and analytically-informed.

Consider, for example, my profitable trading in both Twitter's shares (several years ago before Elon Musk took it private) and over the last 1 1/2 years my profitable trading in Occidental Petroleum OXY (in total nine profitable "swing" trades). This also applies, when executed properly, with my SPY/QQQ Index trading. This all adds up!

To our observant sub (JSR1111) and to the rest of our subscribers I will end by writing that TheStreetPro contributors (and that includes myself!) serve different masters. Some of those masters are investors and many are traders.

I/we try to appeal to both!

BY Doug Kass · Aug 9, 2024, 10:12 AM EDT

BY Doug Kass · Aug 9, 2024, 9:55 AM EDT

Several stocks I am short or long highlighted on the sell side:

Occidental Petroleum price target lowered to $65 from $68 at Wells Fargo Wells Fargo analyst Roger Read lowered the firm's price target on Occidental Petroleum OXY to $65 from $68 and keeps an Equal Weight rating on the shares. Occidental delivered a solid quarter and is on the right track with debt reduction plans post-CrownRock, the analyst says. The company gave an operationally solid outlook, and reducing leverage is a key focus, the firm says.

Warner Bros. Discovery price target lowered to $8 from $10 at JPMorgan JPMorgan lowered the firm's price target on Warner Bros. Discovery WBD to $8 from $10 and keeps a Neutral rating on the shares post the Q2 report. The firm likes the company's mix of assets and improving cost structure, but remains on the sidelines due to a challenged advertising environment and elevated domestic video subscriber declines.

Freedom Holding reports Q1 EPS 57c vs. $1.15 last year Freedom Holdings FRHC Reports Q1 revenue $450.72M vs. $316.21M last year. Timur Turlov, the company's founder and chief executive officer, provided commentary on the quarter by stating, "As has been our process for the past number of years, we continue to direct our profits into the further expansion of our business and the first quarter of fiscal 2025 was no exception. With a $177 million increase in total expenses as compared to the same period last year, we managed to contribute over $34 million to the bottom line during the quarter. Our investments in people, systems, and the expansion of our fintech ecosystem continues to bear fruit, which is evidenced by a 188% increase in insurance underwriting income, a 51% increase in interest income, and a 17% increase in fee and commission income, with these three being our largest sources of revenue for the quarter."

BY Doug Kass · Aug 9, 2024, 9:45 AM EDT

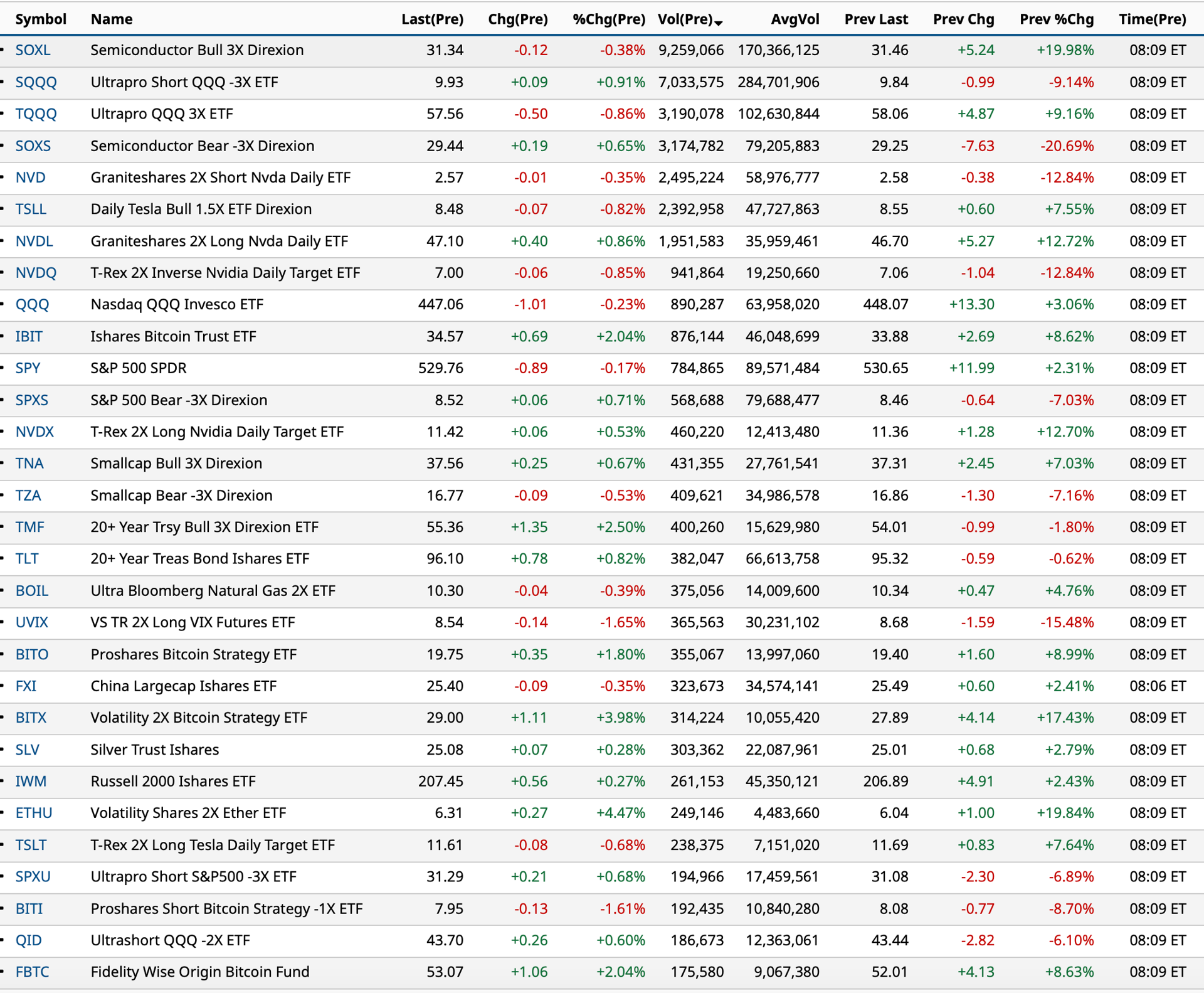

Chart as of 8:09 a.m.:

BY Doug Kass · Aug 9, 2024, 9:20 AM EDT

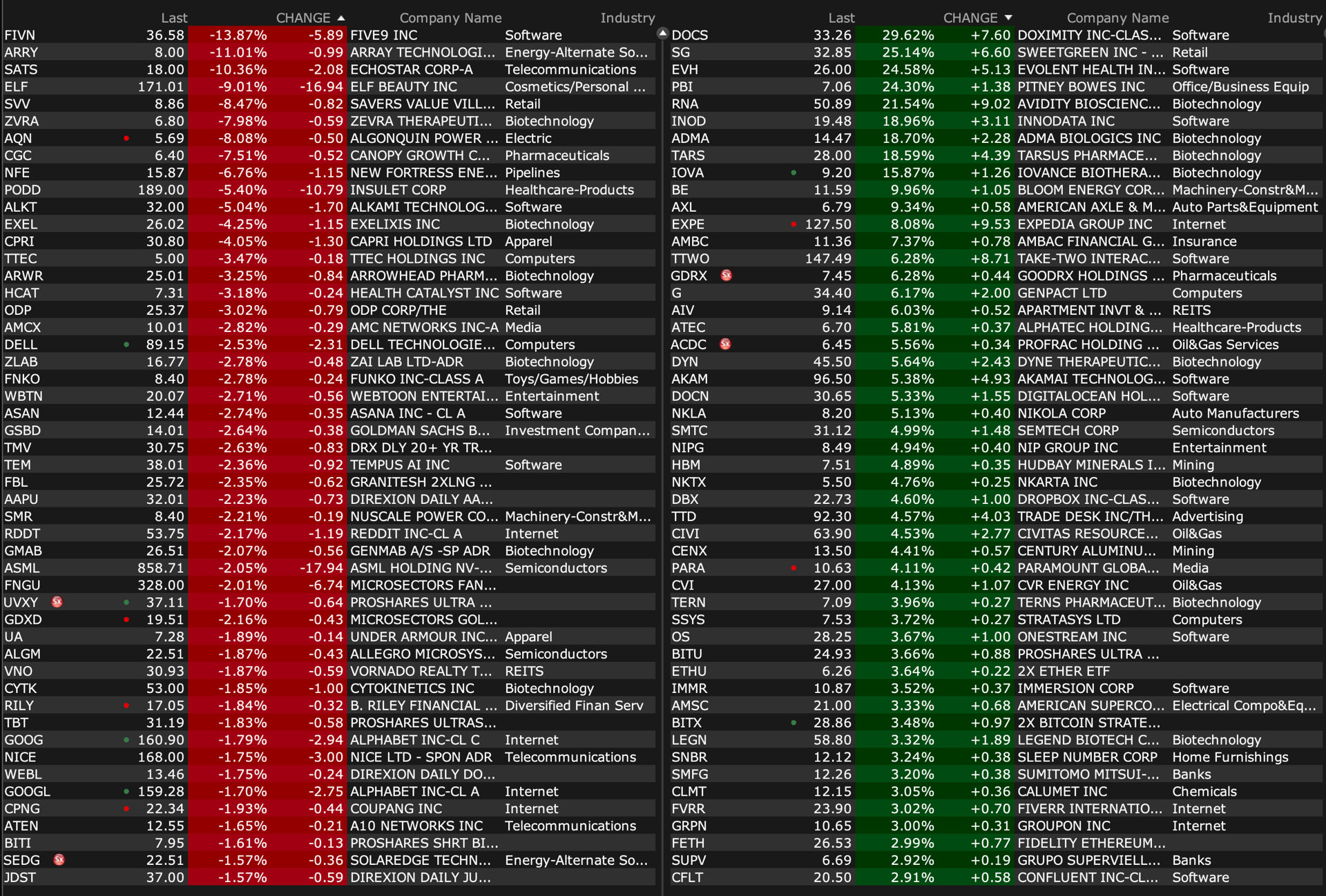

Chart as of 8:26 a.m. ET:

BY Doug Kass · Aug 9, 2024, 9:13 AM EDT

As of 8:19 a.m. ET:

-PARA +5% earnings

-EXPE +8% earnings

-PBI +25% earnings/asset sale

-SG +24% earnings

-TTWO +7% earnings

-BW +20% earnings

-DOCS +30% earnings

-INOD +18% earnings

-ADMA +7% earnings

-CARG +10% earnings

-AKAM +5% earnings

-TTD +5% earnings

-BLND +11% earnings

-DBX +5% earnings

-PGY +11% earings

-ELF -4% earnings

-CPRI -4% earnings

-SKIN -20% earnings

-MITK -11% earnings

-PUBM -20% earnings

-FIVN -20% earnings

-EB -21% earnings

-SATS-10% earnings

-TUSK -5% earnings

BY Doug Kass · Aug 9, 2024, 9:00 AM EDT

From Peter Boockvar:

Let's remind ourselves from Monday that those who were calling for the Fed to slash and burn the fed funds rate and even before the next meeting was not because there was an economic meltdown going on but because we had a lot of FX volatility and a sell off in stocks. I get it, the Fed has trained us all too well. That said, I do believe the Fed should start gradually cutting rates, even 50 bps in September, but to believe that right now the Fed is going to start freaking out, it's not happening.

However, if the S&P 500 is instead at 3500-4000 instead of just above 5000, then we also assume credit markets have notably tightened up and the Fed then needs to start taking into account their 3rd mandate, the wealth effect as higher end spend is helping to hold the US economy on its shoulders.

Voting member Tom Barkin said yesterday, "It's hard to make the case that something has just happened that is monumental on the equity side." On the economic side, "It think you've got some time in a healthy economy to figure out whether this is an economy that's gently moving into a normalizing state that will allow you to, in a steady deliberate way, normalize rates or...is this one where you really do have to lean into it." On prices, "all the elements of inflation seem to be settling down and I'm relatively hopeful based on the conversations I'm having that that's going to continue."

With very little data out there, addressed below, here are some of the noteworthy earnings comments.

From Under Armour, a stock we own and I believe an exciting turnaround story:

Specifically in North America, sales fell "due to softer full-price wholesale demand and lower sales to the off-price channel. Our DTC business was also down during the quarter, driven mainly by a decline in our e-commerce business resulting from proactive strategies to reduce promotional activity and a decline in our retail store sales."

From Restaurant Brands, the owner of Burger King, Popeye's, and Tim Horton's:

"While we still delivered solid global comparable sales growth this quarter, there's no denying that the environment has been tough. As such, we believe systemwide sales will be a bit lighter this year compared to our stated long-term growth algorithm."

"We clearly saw softer sales than expected across our businesses in Q2 and it's not yet clear when we'll see the category strengthen."

In the US, "The absolute sales and traffic results at Burger King were clearly softer than we aspired to, but the business continued to outperform Burger QSR sales and traffic."

Outside the US and Canada, "Burger King saw positive results in markets like Brazil, Japan, Australia and Mexico. This strength helped to partially offset moderating price trends in many of our Western European markets, challenging consumer dynamics in China and the conflict in the Middle East."

Tim Horton's always seems to do well.

From Six Flags, the amusement park company in the heart of their season, and benefiting from the strong experiential side of the US economy, similar to concerts:

They had record attendance in the quarter of 8.6 million guests vs 8.3 million in the same quarter last year. But, "The increases in attendance and out-of-park revenues were partially offset by a 3% decrease in in-park per capita spending." Their Knotts's hotel business is included in 'out-of-park' spend.

The color on 'in park' spend and the drop "is due to a planned reduction in season pass pricing at several parks and a higher mix of season pass visitation, somewhat offset by improved guest spending on food and beverage and extra-charge products."

On the latter, "Food and beverage spending during the quarter was up 3% vs the comparable 3 month period last year. The improved F&B spending was driven by an increase in average transactions per guest and an increase in the average transaction value, reflecting the guest willingness to buy up for higher quality offerings."

"The increase in attendance was the direct result of several factors, including a larger season pass pace; the continued recovery of the group channel, including our school and youth business, which has now recovered back to pre-pandemic levels; and lastly, stronger general demand in the markets where we introduced impactful new rides and attractions for the 2024 season."

Back to the food business with Papa John's:

"the challenging sales trends we experienced in the 1st quarter within our North America restaurants have persisted into the 2nd quarter and while our core product, pizza, and the quality of our brand remained in demand, the macro environment continues to be challenging as consumers pull back on their spend and increasingly focus on value."

Their Q2 North America comps fell 4% y/o/y, similar to Q1 and "was primarily driven by lower transactions."

"In this current economic cycle, consumers have become more deliberate in managing their overall ticket and are showing preference for brands that are offering compelling value."

Sweetgreen continued to see strong comp growth of 9% in Q2 with 5% benefit from menu price and 4% positive traffic and mix."

"Sweetgreen's high quality offering and compelling value is clearly resonating with consumers in today's industry backdrop."

They raised their full year guidance because of a strong first half but "We remain cautious for the 2nd half of the year, given what we are reading about the uncertain US economic backdrop."

From Capri, the owner of brands like Versace, Jimmy Choo and Michael Kors:

In their earnings release, "Overall, we were disappointed with our 1st quarter results as performance continued to be impacted by softening demand globally for fashion luxury goods."

Back to experiential with travel and from Expedia where they are also seeing a slowdown in their travel business in the current quarter:

"The travel environment was healthy in the 2nd quarter, and like the last few quarters, we saw stronger demand internationally relative to the US. Compared to last year, we grew room nights mid-single digits in the US, low double digits in Europe, and in the high teens for the rest of the world. Prices held up for both hotel and vacation rentals, but we saw continued pricing pressure for air and car."

On guidance, "While we accelerated our gross bookings throughout Q2, entering the 3rd quarter we have seen a more challenging macro environment and a slowdown in travel demand, consistent with recent commentary from others in the travel industry." They specifically saw "consumers trading down to lower priced properties. And we have also seen more continued softness in air ticket prices."

To the overseas economic data, China said its July CPI rose .5% y/o/y, two tenths above the estimate but obviously modest and stable. Prices ex food and energy rose .4% y/o/y vs a .6% gain in the month before. With the Chinese consumer reluctant to spend, a low cost of living is a good thing. When home prices stop going down, I expect a resumption of healthier Chinese spending.

July PPI fell .8% y/o/y, the same pace as seen in June and compares with the estimate of down .9%. As July 2023 saw a price drop of 4.4% y/o/y, the comps have become easier. Either way, we know the Chinese economy has its pluses and minuses with the biggest challenge being the continued drop in home prices as they continue to work through their residential real estate recession.

BY Doug Kass · Aug 9, 2024, 8:45 AM EDT

BY Doug Kass · Aug 9, 2024, 8:32 AM EDT

Google is down in premarket trading apparently because former President Trump says Google could face a shutdown.... “Google Close to Being Shut Down,” Donald Trump Takes on Tech Giant | Firstpost America

BY Doug Kass · Aug 9, 2024, 8:15 AM EDT

Taiwan Semiconductor's TSM July upbeat sales announcement: Taiwan Semiconductor's July sales surge nearly 45% amid AI chip demand | Seeking Alpha should buoy (or at least stabilize the shares of several leading tech companies that have catapulted from Monday's lows - that I recently purchased: AMZN, ARM and GOOGL.

BY Doug Kass · Aug 9, 2024, 8:05 AM EDT

I post this because I see a number of subs (in comments section) are bottom fishing in this name:

Moffett Nathanson cuts price target of Paramount Global PARA from $12 to $10.

As I have written, an extended period of "profitless prosperity" lies ahead for streamers.

I have profitably covered my PARA short, but remain short Warner Brothers Discovery WBD.

On WBD from yesterday:

I remain short Warner Bros. Discovery (WBD) :

From Goldman Sachs:

8 August 2024 | 12:24AM EDT

WBD’s EBITDA of $1.80 bn missed GS/consensus (Visible Alpha Consensus Data) of $2.0/$2.1 bn with a miss across all three segments. Within Networks, Distribution revenue declined 9% yoy (-5% excluding AT&T SportsNet RSN disposition), accelerating from -7% yoy in 1Q24, on accelerating cord cutting, seasonal cord cutting post the NFL season (pronounced in vMVPDs), and fee step-downs internationally on linear to support DTC. Advertising declined 10% yoy, improving from the -11% yoy realized in 1Q24. Although DTC EBITDA of -$107 mn missed, KPIs were strong with 103.3 mn subscribers (+3.6 mn qoq) with WBD guiding to accelerating net adds in 3Q24 driven in part by the Olympics and continued international expansion (GSe +6.0 mn in 3Q24). WBD reiterated its outlook for DTC EBITDA profitability in 2024 and >$1 bn of EBITDA in 2025. Although we’re encouraged by WBD’s DTC momentum as well as investments in Linear Networks sports programming (e.g., Big East, college basketball, Mountain West, CFP, French Open), the loss of the NBA and uncertainty from the litigation to pursue matching rights creates mid-term uncertainty in the outlook for Linear Networks profitability (~90% of consolidated EBITDA).

From The Credit Strategist:

Wed, Aug 7 at 6:39 PM

Warner Brothers Discovery (WBD) is turning into a melting ice cube. The company announced this afternoon a $9.1 billion non-cash write down of its television networks, a terrible sign of how severely the value of legacy media is deteriorating. The company will try to downplay this but the merger between Warner and Discovery is turning out worse than the one between Time-Warner and AOL. And while shareholder value is being destroyed, WBD is still paying its CEO huge amounts of compensation every year which simply isn’t deserved.

Something is seriously wrong with this company. Actually many things are wrong. For one, its board of directors is totally out-to-lunch. It rewards non-performance which is a sign that board is not independent and not serving shareholders. Second, company lacks a viable strategy to compete in today’s media world. It lacks the scale and financial strength to compete against DIS (which has its own problems), AMZN, AAPL, etc. Even though it bid to keep NBA rights, the league favored AMZN which has much deeper pockets and much broader consumer and global reach. WBD is trying to compete in today’s world with yesterday’s assets and tools. Streaming - which is in a price war squeezing profits - won’t save it.

With way too much debt & a shrinking equity market cap, WBD is looking at a credit downgrade if the credit rating agencies are paying attention. That will raise its cost of capital and make things worse. Something needs to be done quickly to reverse the downward slide.

Position: Short WBD (S)

By Doug Kass Aug 8, 2024 6:20 AM EDT

BY Doug Kass · Aug 9, 2024, 7:50 AM EDT

“When deciding to sell, people have control over whether to give themselves pleasure or give themselves pain, and they tend to give themselves pleasure. In other words, they tend to sell winners and hang on to losers. It turns out to be a bad idea.”

- Daniel Kahneman

Bonus - here are some great links:

Why Sentiment Changes so Rapidly Why Sentiment Changes So Quickly - Joe Fahmy

A Deeper Dive into the Carry Trade A Deeper Dive Into the Carry Trade (lpl.com)

Opportunities That Lie Ahead Opportunities in today's market with Jay Woods, Chief Global Strategist at Freedom Capital Markets | FINTECH.TV

New Blackstone ETF May Mark The Top New Blackrock ETF Marks the Top - All Star Charts -

BY Doug Kass · Aug 9, 2024, 7:25 AM EDT

Wells Fargo cuts OXY price target from $68 to $65.

BY Doug Kass · Aug 9, 2024, 7:10 AM EDT

The market has grown increasingly unpredictable and volatile.

Indeed, it is not only the Olympics that has a number of contact sporting events like wrestling — so, too has trading become a contact sport this week.

I am looking forward to travelling next week!

BY Doug Kass · Aug 9, 2024, 7:00 AM EDT

BY Doug Kass · Aug 9, 2024, 6:50 AM EDT

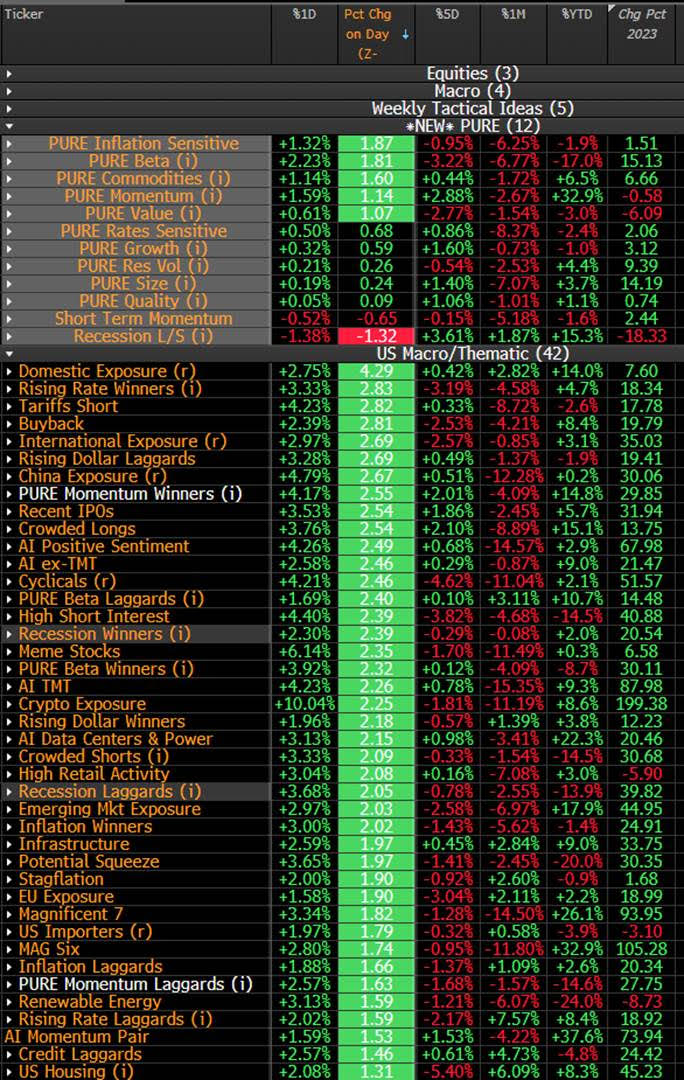

This table is a valuable chart for momentum-based short-term traders:

BY Doug Kass · Aug 9, 2024, 6:40 AM EDT

From JPMorgan:

US: Futs are higher with broad-based gains across indices. MegaCap Tech outperformed pre-market: the top three movers are NVDA (+2.5%), TSLA (+1.6%), and MSFT (+1.1%). TSMC reported strong revenue growth in July, indicating robust AI chip demand. Yields are lower and USD is lower; 2-, 5-, 10-yr yields are 1bp, 3bp, 3bp lower. Commodities are mixed with oil slightly higher, base metals mixed, and precious metals mostly flat.

and...

EQUITY AND MACRO NARRATIVE: Yesterday, markets rallied after the modestly lower jobless claims that eased some fears on recession risks. While this decline in jobless claims (233k vs. 240k survey vs. 250k prior) seems to be a small magnitude, the lack of further macro catalysts this week led to a more pronounced equities reaction. The rally was broad-based across all sectors: 8 out of 11 sectors gained over +1.5% today, with 91% of SPX stocks in green. Thematically, most of D1 baskets rallied over +2z today, indicating a rapid shift in risk sentiment fueled by improved macro data this week (ISM-Srvcs and Claims), carry unwind near completion, less technical headwinds post correction.

POSITIONING INTELLIGENCE

Tactical Takes | Latest Thoughts on Positioning as TPM Suggests "Attractive" Set-Up

Summary: While our view is that the recent decline in equity positioning has been mostly attributable to shifts in futures (rather than direct selling of stocks), we think the positioning set-up is turning more attractive with a few additional signs of risk-off behavior (e.g., 1.8z net selling in N. Am. on Wed across PB mostly due to equity ETF shorts added). Prior to yesterday, HFs had been buying the dip in Tech stocks (Mag7 in particular) over the past week.

As we alluded to in last week’s note, our US Tactical Positioning Monitor (TPM) has once again hit our threshold for an attractive set-up for the S&P 500, based on the fact that it dipped to -1.5z over the past 4 weeks (-2.2z on non-averaged basis and -1.5z based on 3d average). This is due to most metrics turning more negative vs. a week ago. It also includes our estimate for what we think Asset Mgr positioning will be once we get the CFTC data tomorrow. From a level of positioning standpoint, we think we’re now back at neutral (0z, 51st %-tile).

While the decline in positioning suggests the market could rebound, the set-up still seems a bit uncertain due to other signals that point to a less bearish buildup than in the past (e.g. magnitude of HF shorting in single-stocks not as extreme, Credit/FI ETF metrics less extreme, Retail investors still buying ETFs). More generally though, if macro data continues to be OK, we could see the market continue to recover. We also think the current dynamic has similarities to Feb ’18…i.e., in both periods there was no big HF de-gross in stocks right around the VIX spike, HF performance turned out OK, and the market bounced (though the SPX did hit the 200dma back then and was choppy over the next few months).

BY Doug Kass · Aug 9, 2024, 6:30 AM EDT

BY Doug Kass · Aug 9, 2024, 6:16 AM EDT

Wolf Street howls about Blackstone's BX "mop up" of Bumble BMBL.

BY Doug Kass · Aug 9, 2024, 6:05 AM EDT

The S&P Short Range Oscillator is down to -0.63% vs. -1.11%.

BY Doug Kass · Aug 9, 2024, 5:55 AM EDT

Wolf Street howls about autos and loans.

BY Doug Kass · Aug 9, 2024, 5:45 AM EDT