Jay Powell sounds like he has verbal constipation with respect to a September rate cut. He so wants to say today "let’s do it" but at the same time knows he doesn’t have to commit just yet before he gets more time and data until September 18.

As the "talking heads" rejoice in a likely easing later in the year (that everyone expects) and repeat the same observation they all do — check out homebuilders that gave up $4-$5/share in the last 90 minutes.

Before I retire to bed I wanted to mention that so far the algos have told Chair Powell to screw off. (I am editing this to be PC as that is not the word I would normally use in conversation!)

The markets clearly believe the Fed is their candy and for good reason based on how the Fed has historically behaved.

The FOMC statement nudges, doesn't push us to a Sept rate cut but Powell likely will

Again, the FOMC is leaving it to Jay Powell’s press conference in order to glean where the lean is on the timing of rate cuts as the statement had only modest changes, though still of note. The set up for that September cut was some tempering of the wording on the labor market. In June they said, “Job gains have remained strong, and the unemployment rate has remained low.” This was replaced with “Job gains have moderated, and the unemployment rate has moved up but remains low.”

Also, there was a very modest tweak to the inflation comments but also a set up for a cut. In June they said, “there has been modest further progress toward the Committee’s 2% inflation objective.” Today that line reads, “there has been some further progress toward the Committee’s 2% inflation objective.”

Bottom line, the Fed in the statement slightly sowed the seeds for a cut at the next meeting as they gather more evidence that substantiates one. Powell at his presser though will be able to give more tone and body language on whether that’s a lay up or not, which it likely is but something the market has already priced in.

As there was nothing more in the statement of substance, yields ticked up somewhat with the 2 yr yield at 4.38% vs 4.36% just prior. The 10 yr yield of 4.12% was at 4.10-.11% just before.

Following its "year of efficiency" in which META kept a tight lid on expenses, fueling robust earnings growth, the social media and VR company is shifting back into investment mode as it invests in IT infrastructure to support the launch of AI technology. As such, META raised its FY24 capex guidance last quarter to $35-$40 bln from $30-$37 bln, creating some disappointment among investors who became accustomed to the company cutting its capex forecast.

META also raised its FY24 total expense guidance last quarter to $96-$99 bln from $94-$99 bln due to higher infrastructure and legal costs. Along with the higher expected capex, the new opex forecast played a major role in the stock's weakness in the wake of the Q1 report. With that in mind, META's updated FY24 capex and opex guidance will be closely monitored tonight.

The jump in estimated capital expenditures and costs weren't the only disappointment last quarter, though. META's Q2 revenue guidance of $36.5-$39.0 bln was also modestly below expectations at the midpoint of the range, creating some concern that advertising spending was starting to soften following a strong recovery over the past few quarters.

Those concerns have been validated over the past week. On July 24, Alphabet (GOOG) reported Q2 results that edged past EPS and revenue estimates, but advertising revenue growth slowed a bit to 11% from 13% in Q1. Additionally, Pinterest (PINS) issued a disappointing Q2 earnings report last night that included downside revenue guidance for Q3.

We expect META to spend plenty of time discussing its AI projects during the earnings call. Indeed, the company's AI investments have already had a positive impact on its financials. For instance,AI is helping to drive stronger app engagement metrics, leading to stronger ad impression growth (+20% in Q1) and higher average price per ad (+6%) as advertisers see greater returns on META's platforms. Furthermore, CEO Mark Zuckerberg noted during the Q1 call that for the first time ever, more than 50% of the content that people see on Instagram is now AI recommended.

Looking at META's two primary segments -- Family of Apps and Reality Labs -- there continues to be a huge divide in performance, most notably, in terms of profitability. Fueled by a 7% increase in Family daily active people (DAP) to 3.24 bln, a 20% increase in ad impressions, and a 6% increase in average ad prices, revenue climbed by 27% to $36.46 bln in Q1 for Family of Apps. Operating income surged by 57% to $17.7 bln. On the flipside, Reality Labs posted an operating loss of ($3.8) bln, barely budging from the ($4.0) bln loss in the year-earlier period.

Lastly, litigation and regulatory issues continue to lurk in the background for META. On July 25, Reuters reported that the company will likely be fined by the EU within the next few weeks for linking Marketplace and Facebook. That fine, which could be as high as $13.4 bln, could factor into META's operating expense guidance. (PVIEW).

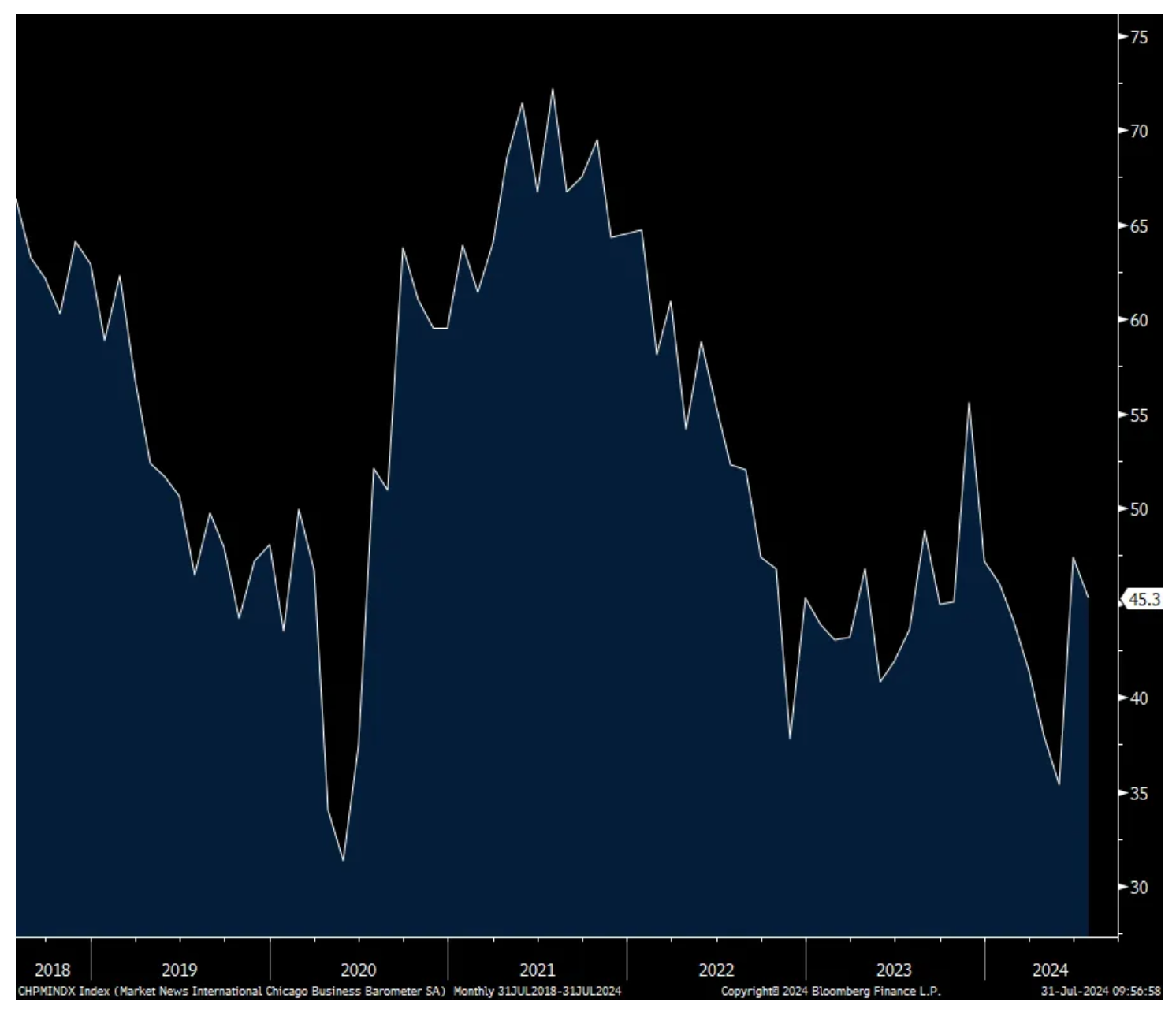

Chicago mfr'g joins others in contraction/Housing sales lift in June

Joining NY, KC, Richmond and Dallas in the contraction camp, still, the Dallas July manufacturing PMI fell to 45.3 from 47.4. It’s been above 50 once since August 2022. I don’t have the internal details. The estimate for tomorrow’s ISM manufacturing index is for it to remain below 50 at 48.8.

Chicago PMI

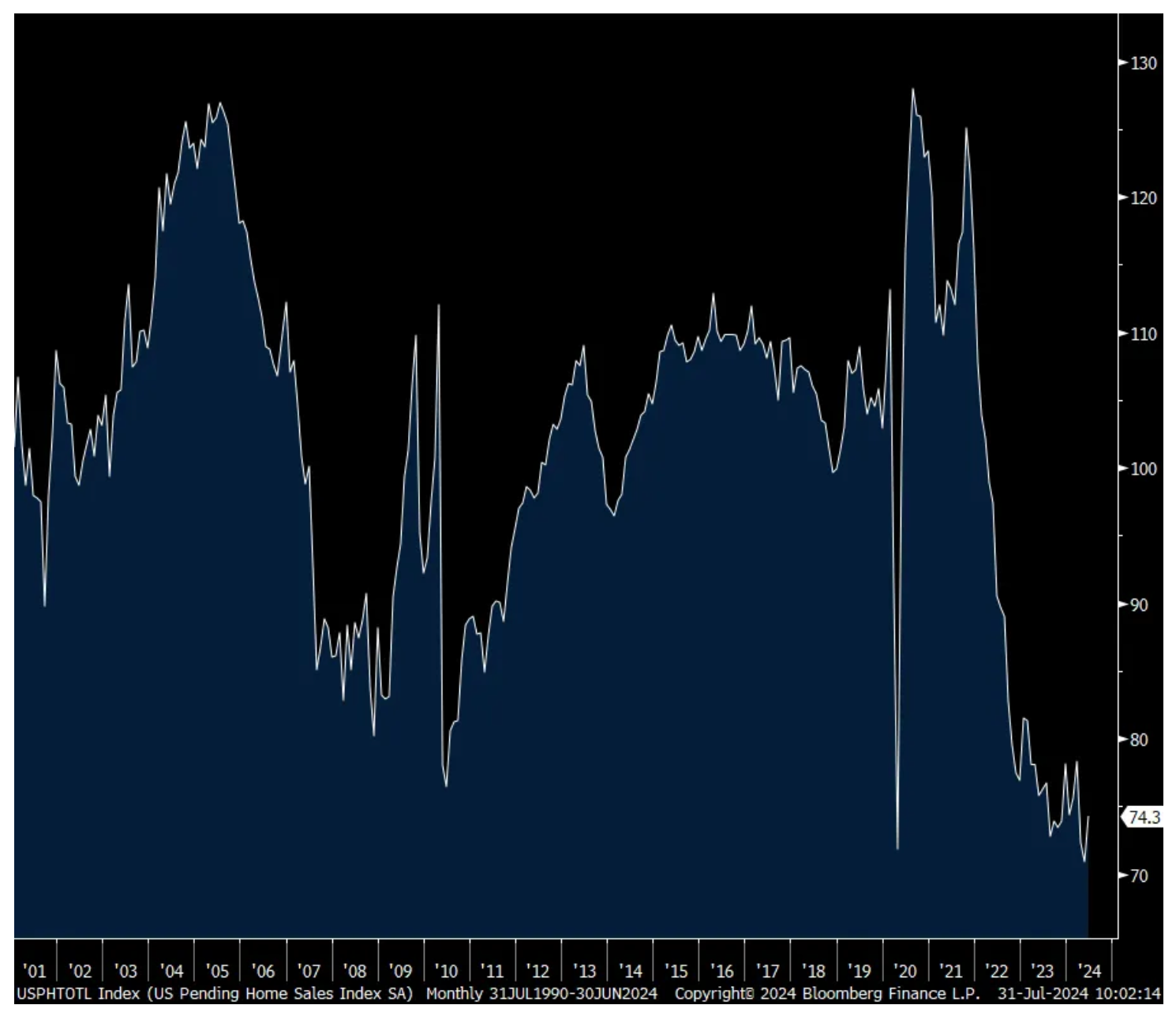

Pending home sales in June rose 4.8% m/o/m, better than the estimate of up 1.5%, though still down 7.8% y/o/y. All four regions saw increases vs May.

The NAR attributed the bounce to a lift in supply, “The rise in housing inventory is beginning to lead to more contract signings. Multiple offers are less intense, and buyers are in a more favorable position.”

Bottom line, the index lift in June was off the lowest level since this data started in 2001 so some perspective on the rebound. The average 30 yr mortgage rate was 7.28% in June vs 7.22% so far in July and which compares to 7.14% as of yesterday according to Bankrate. While ever higher home prices is certainly good for those who currently own, it remains a stumbling block for that first time buyer who is a key part of the housing transaction chain as the move up buyer needs to sell to someone.

"I am going to write a good Diary on TheStreet Pro today... and I am going to help people. Because I am good enough, I am smart enough and doggone it, people like me."

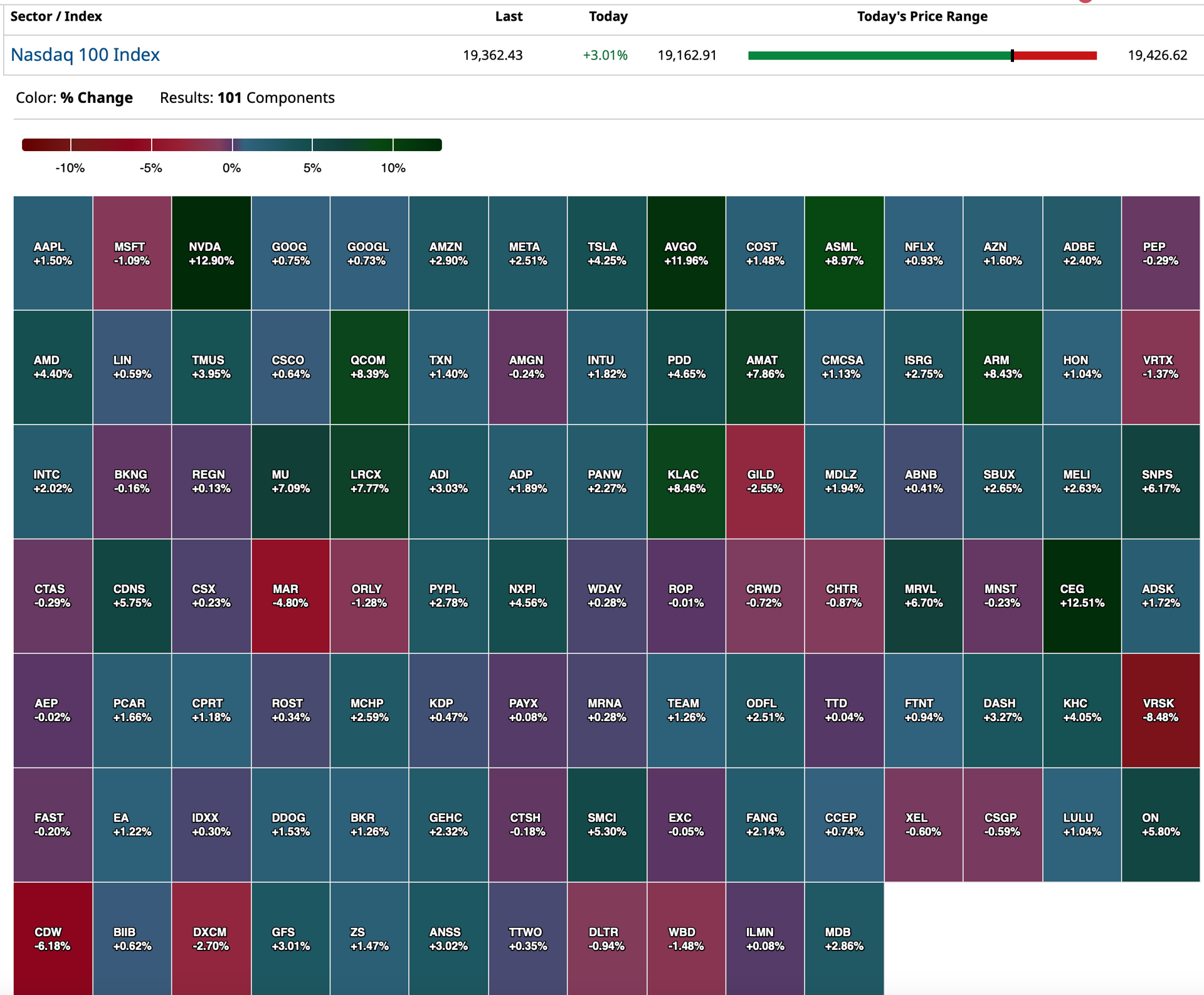

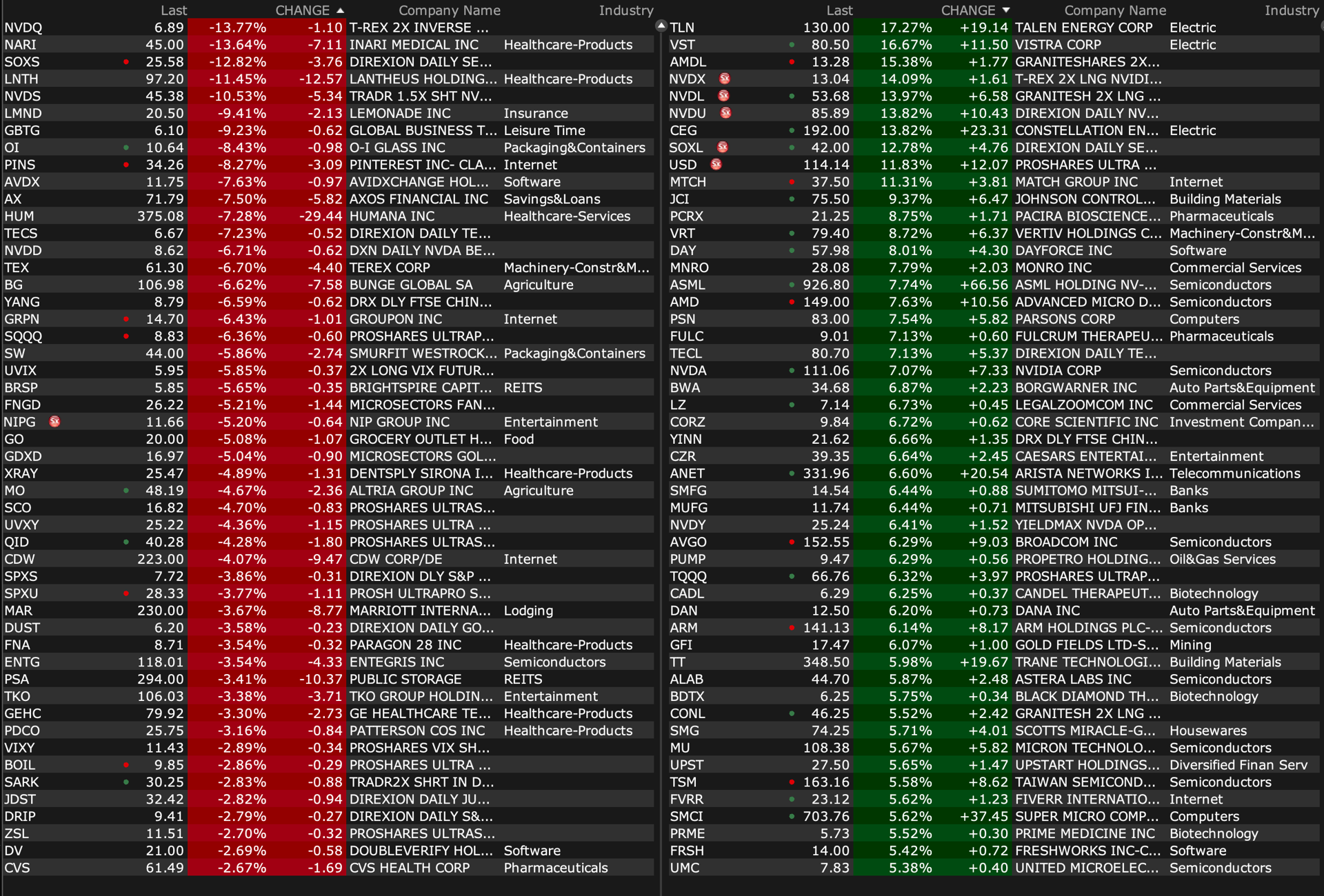

If I could only figure out the machines and algos ... Meanwhile, if I could only figure out what the computers do, I would be a trillionaire. NVDA down 7% yesterday, up 10% today. Could have made 17% if had both moves right. In normal times, that is 2 to 3 years of returns.

AMD up 10% in part because people are optimistic about their ability to take share in AI. Why is that good for NVDA? Why is MSFT cloud business slowing good for NVDA?

Fed will signal they will cut in September when they speak today, but the market has known that for about 2 weeks, and been assuming that forever, and been assuming more cuts than the Fed will deliver because inflation is pretty sticky.

Back to my original point, if I only knew how the algos think.

I never understand what makes them go in one direction or the other. The thing that has the algos going crazy today is not new news.

That said, an understanding of intrinsic value helps in times of extreme volatility - to take advantage of price swings.

Broockvar: Bank of Japan Turns Hawkish, the World Turns Dangerous, Live Nation Rocks

From Peter Boockvar:

A lot of good stuff here

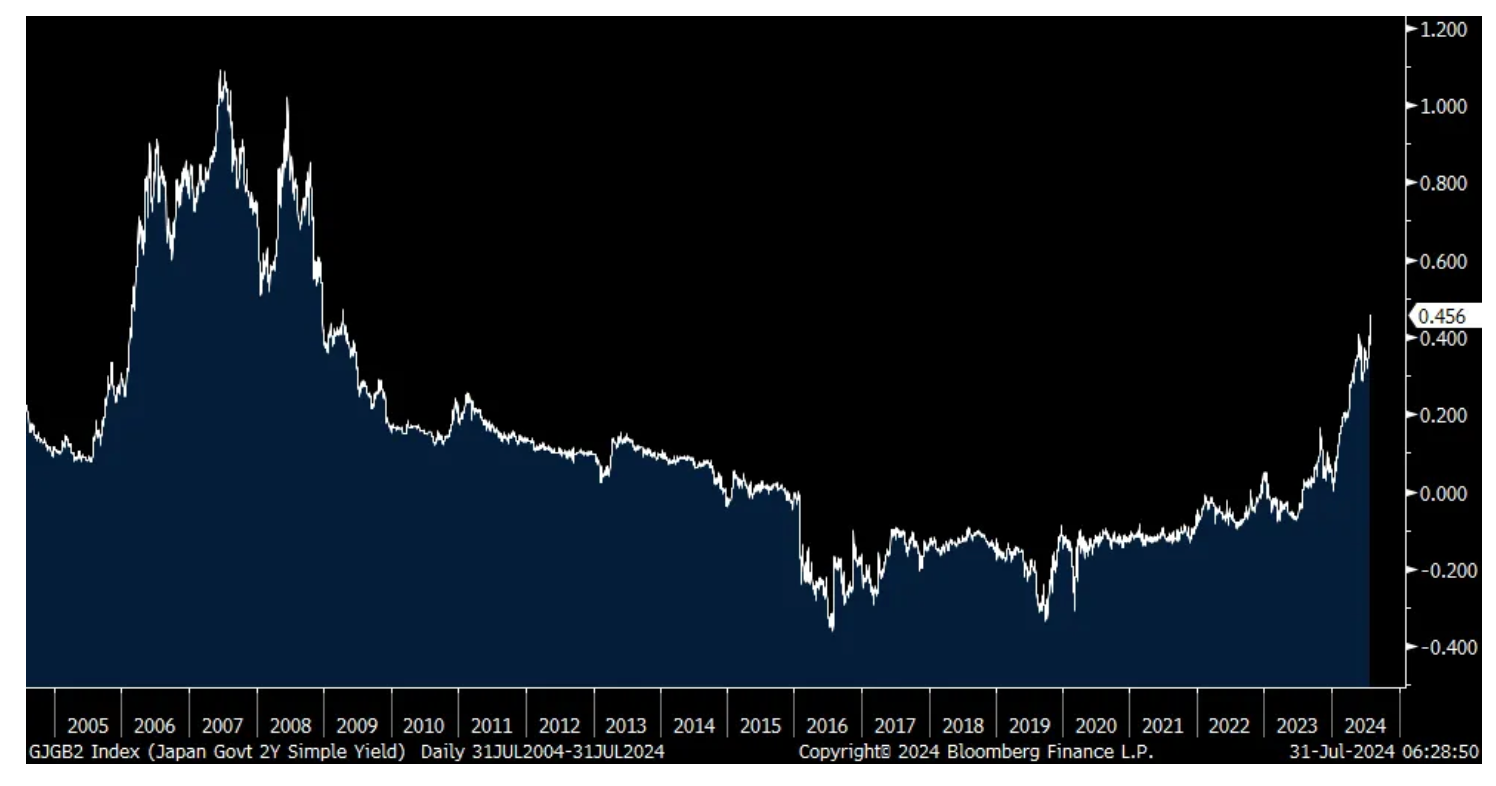

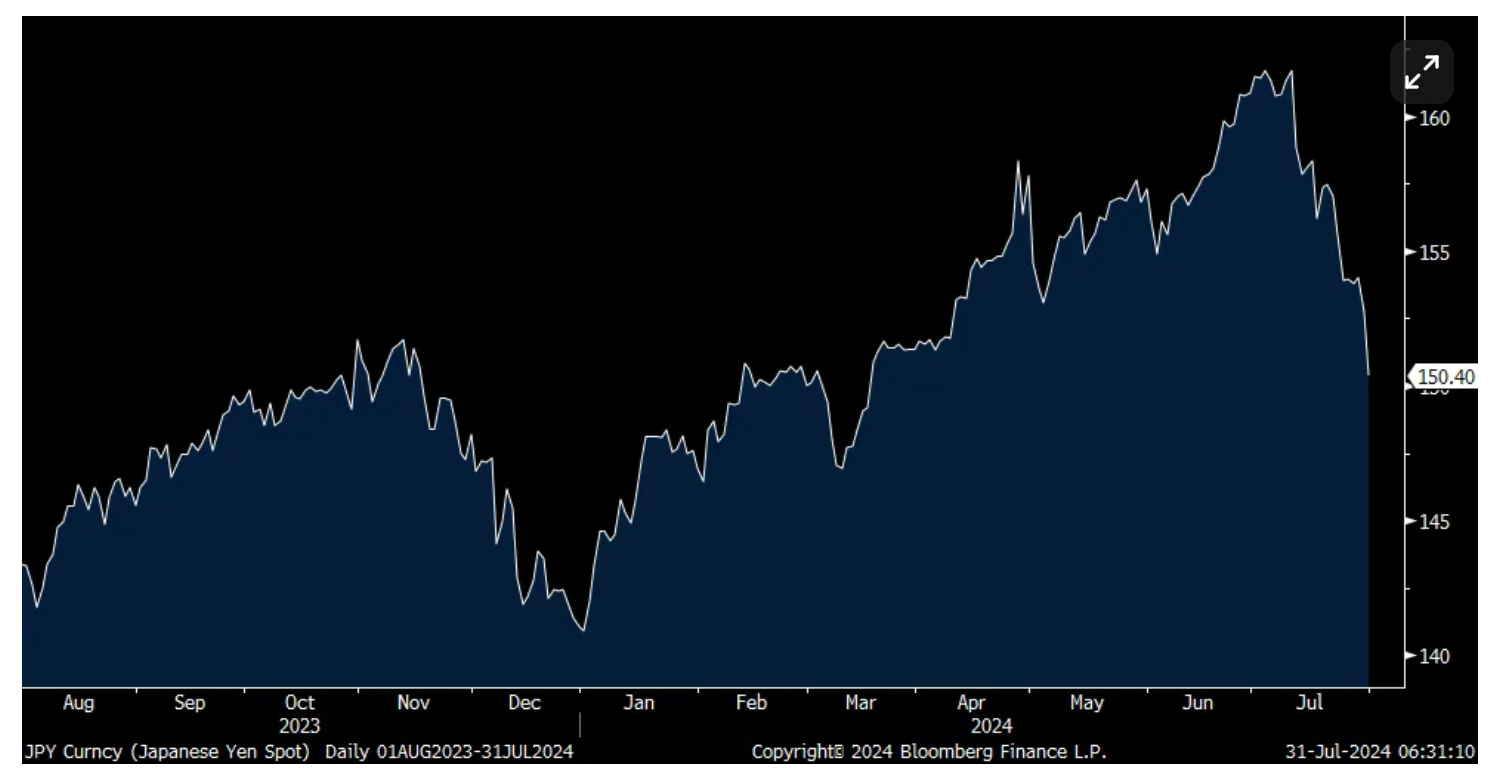

The BoJ and hawkish are never two things that end up in the same sentence but overnight changed that as the BoJ gave us both a rate hike to .25% from a range of 0-.10% and a cut in half in their QE bond buying program to 3 trillion. Inflation is what the BoJ wanted for years, inflation is what they got and now the people and the government are not happy that it's here and the BoJ is finally doing something about it. The 2 yr JGB yield jumped by almost 8 bps to .46%, the highest since 2009. The 10 yr yield rose 5 bps to 1.06% and the yen is ripping higher again with another big move of 1.6% to the 150ish level, the highest since March. The Nikkei was higher too as cooling inflation and giving the Japanese people some more purchasing power is good for their economy. We remain bullish and long Japanese stocks and the yen as well.

Here were some comments from Governor Ueda:

"We've also confirmed rises in services prices. We expect a moderate cycle of rising wages and inflation to continue. The weak yen is also pushing up import prices, so we need to be vigilant to the risk of an inflation overshoot...Even though we raised rates, real interest rates remain low. Our move won't affect the economy much."

As for what is to come, "If the economy and prices move in line with our projection, we will continue to raise interest rates. In fact, we haven't changed much our projection from April. We don't see .50% as any key barrier when raising rates...If conditions move in line with our forecast, or overshoot our forecast, we could raise interest rates further...By raising rates from very low levels and adjusting the degree of stimulus gradually, we can avoid the risk of having to make big adjustments in a short period of time."

The weak yen to 160 really put the screws to the BoJ as the complaints from the government and the citizenry really left the BoJ no more choices. On the yen Ueda said, "The yen has weakened since the start of this year, but we haven't changed our consumer inflation forecasts that much...But there's quite a significant risk of the weak yen leading to an overshoot of inflation."

My bottom line, finally.

2 yr JGB Yield

Yen

In contrast to the JGB yield move, Australian bond yields are plunging after we saw Q2 CPI in line relative to expectations but the trimmed mean calculation rose two tenths less than forecasted q/o/q. The 2 yr yield is down by 22 bps and the 10 yr yield fell by 16 bps. A big move as the RBA has some breathing room.

The crude oil move higher in response to the Israeli killing of the Hamas official in Iran is a reminder that geopolitics this time around is a big thing we can't ignore as opposed to most geopolitical backdrops which are usually fleeting in terms of its market impact. We continue to be positive and long oil and gas stocks.

Hong Kong's economy grew more than estimated in Q2, by .4% q/o/q and 3.3% y/o/y vs the estimate of up .3% and 2.7% respectively, helped by exports which offset weakness in consumption. Hong Kong stocks rallied by 2%. The mood is so dire with China and Hong Kong, where it's rare to see sentiment this awful. We remain bullish and long some stocks that trade there.

China's July PMI was little changed m/o/m. The manufacturing index remained below 50 at 49.4 vs 49.5 in June as expected. Non-manufacturing slipped to 50.2 from 50.5. The estimate was 50.3. Combining the two has the composite index at 50.2, reflecting flattish growth with the residential real estate challenges the biggest economic issue they need to work through.

Taiwan's economy grew by 5% y/o/y in Q2.

The July Eurozone CPI exceeded expectations by a tenth for both the headline and core. The headline rose 2.6% y/o/y and the core rate was up by 2.9%. Service inflation remains persistent, up by 4% y/o/y. Non-energy industrial goods prices grew by .8% y/o/y and has been slightly below 1% for a 4th straight month. While data like this will keep the ECB in a rate tweaking cycle rather than aggressive cutting, inflation expectations aren't changing much today and sovereign bond yields are actually lower by 2-3 bps across the region.

On to the earnings comments of note.

From Live Nation, a stock we still own:

"We continue to see strong demand globally, with a growing variety of shows attracting both casual and diehard fans who are buying tickets at all price points, which speaks to the unique experience only live concerts can provide."

"Year-to-date ticket sales for 2024 Live Nation concerts are 118 million, higher than 2023 with double digit increases for arena, amphitheater, and theater and club shows. Confirmed shows for large venues (stadiums, arenas and amphitheaters) up double digits."

"seeing very strong casual demand...And finally, once they go to the show, what's their behavior? And again, we're seeing no issues and that we continue to be on track for a couple dollars in spend at our amphitheater. So, I think it's all consistent with our concerts being seen as very good value for money, 2/3rds less than $100, a third of them less than $50. It's a much more memorable event than a lot of other experiences you can get at that price point. So, we continue to feel very good about the strong level of consumer demand we're seeing."

From Starbucks who saw a 2% drop in comps in North America, down 14% in China, "partially offset by strong performance in Japan":

The overall 3% drop in comps came from a 5% drop in transactions and a 2% rise in average ticket "as we continue to navigate through a value-driven consumer environment."

"we are operating in a challenging consumer environment. You see the impact of that in away from home consumption. If you look at our business at home, for grocery stores with our brands, you're seeing volume increase, you're seeing share increase in a category that's in decline, but we're seeing volume increase at home."

"Looking outside the US, we continue to see weakness in parts of our international business and strength in others. Headwinds persist in the Middle East, Southeast Asia, parts of Europe, driven by widely discussed misperceptions about our brand. In some European markets, consumers are stretched. At the same time, we see significant strength in markets like Japan and parts of Latin America. China is one of our most notable international challenges...The competitive market dynamics in China are reflected in our recent results. We continue to face more cautious consumer spending and intensified competition."

Marriott is lowering is full year 2024 guidance:

"primarily as a result of a weaker operating environment in Greater China, as well as marginally softer expectations in the US & Canada."

From Paypal:

"we see the US environment being very consistent right now with what we've seen over the first half. International is a real strength for us."

From Proctor & Gamble, volume was up 2%, pricing was up 1%:

"As we enter fiscal '25, we continue to expect the environment around us to remain volatile and challenging from input costs, currencies, to consumer, competitors, retailers, and geopolitical dynamics."

"85% of the business is performing right in line with expectations and right in line with what we would have expected throughout the year."

Specifically in North America, "We have strong growth...4% volume growth in the quarter." Europe saw 3% volume growth.

They talked about weakness in China, "We have highlighted that we expect the China recovery to be slow and to take time And I think that's playing out in the results we see in the 2nd half."

Also, "The Middle East situation has not really improved, so we continue to see developing stronger impacts on western retailers in some of these markets."

To a specific question on the consumer in the US and Europe, "So from a consumer standpoint, we generally don't see the dynamic that some are describing. And I'm not meaning to discredit their descriptions. But if you look at a couple of dynamics, private label shares as an example, which typically would be increasing during a time of significant consumer pressure, that's not what we're seeing. Private label shares generally, both in North America and Europe, are in line with pre-Covid levels."

With respect to volumes and the consumer, "Is unit growth declining? And that's, again, not what we're generally seeing. Now, certainly there are some consumers that are I'm sure under increased pressure and are probably modifying their behaviors and purchases accordingly. But in our categories, these are less discretionary categories. These are daily use categories where performance drives brand choice."

Something we've seen from a bunch of credit institutions, tighter lending standards have kept a lid on loan losses after the recent increases and Sofi said:

"Specifically looking at the Q4 2022 vintage, soon after we made material cuts to credit, at roughly 40% of remaining unpaid principal, net cumulative losses of 5.02% are well below the 6.07% observed in the 2017 vintage at that same point of 40% remaining principal balance. In addition, you can see that more recent vintages are performing as well or better than the Q4 2022 loans at similar levels of remaining unpaid principal."

"On the personal loan side, we're going to stay relatively conservative compared to our balance sheet ending assets there, primarily because we want to see how the year trends in terms of unemployment. There's a big number coming out on Friday. We're at 4.1% and a move to 4.2% could signal a recession."

From Benchmark Electronics, a contract manufacturing for many OEM's in a variety of industries:

"We were pleased with the sequential and y/o/y strength in aerospace and defense and semi-cap, which, despite anticipated softness in industrials, medical and advanced computing and communications sectors, allowed us to outperform on revenue."

From Microsoft who reported 15% revenue growth and 10% EPS growth:

On Copilot, "The number of people who use Copilot daily at work nearly doubled q/o/q as they use it to complete tasks faster, hold more effective meetings, and automate business workflows and processes."

And a reality check on Generative AI, "at the end of the day, GenAI is just software."

On why Azure grew at the lower end of expectations at 30%, "distinguishing between being at the higher end or at the lower end really was some softness we saw in a few European geos (geographies) on non-AI consumption really made the difference in that number." Growth from here they estimate at 28-29%.

With respect to Office 365, "Seat growth was again driven by our small and medium business and frontline worker offerings, although both segments continued to moderate." I'll add, here is where the direction of the unemployment rate from here even matters for Microsoft too.

Cap ex in the quarter was $19b, "in line with expectations" and "Cloud and AI related spend represents nearly all of our total capital expenditures. Within that, roughly half is for infrastructure needs where we continue to build and lease data centers that will support monetization over the next 15 years and beyond. The remaining cloud and AI-related spend is primarily for servers, both CPUs and GPUs to serve customers based on demand signals."

They expect FY '25 cap ex to be higher than FY '24.

From AMD:

"second quarter revenue increased 9% y/o/y to $5.8b as significantly higher sales of our data center and client processors more than offset declines in gaming and embedded product sales."

I have been following, trading, and mainly profiting off of the AI phenomena for a while now, strictly as an amateur. I have a non-technical appreciation of the field, with some input from a few people, but no real exclusive knowledge. Like everyone else, I am attempting to decide whether the technology is the second coming of steam power or electricity, or just another flash in the pan like cold fusion. On one side are many technology leaders, the heads of MSFT, GOOG etc. Doug K is making the case here for the skeptics side.

My natural cynical side sees the huge financial incentives for the purveyors of AI to overhype the product and it's potential. We have all been inundated with the science fiction view of super intelligence, and can envision the impacts it might make on society. Such potential can sway even the most hardheaded of thinkers. Stripping the hype from the product might be very difficult, especially when trillions of dollars are involved.

However, the doubters, no matter how keen their analysis, must also be doubted. I have previously posted many quotes by established scientists and others questioning everything from quantum mechanics, to computers, to airplanes. Looking at the Wright brothers first flight it is quite difficult to envision SpaceX. The failures of early AI deserve the same deference.

My conclusion is a bit of a letdown, although I hope realistic. I think too many smart people in tech have become believers to consider this a mass delusion. At this point I would be surprised if there was a true "emperor has no clothes moment". I must think that there is some truth beyond the hype.

That said, many, if not most predictions will be diminished, delayed, modified or forgotten. I think a good analogy might be autonomous driving. The delays seem endless, the hype continues, but so does the development, and it is probably eventually going to happen. I see AI the same way. As I have said before, the impacts will be slower than expected in coming. Cutting workers will probably take longer than the most optimistic are predicting. Betting on rapid productivity increases is probably a longshot.

I think the main benefits will be personal assistant type products, as these are much further along in development, and a natural addition to the smartphone and search applications we use every day.

How to invest is another conundrum. My risk control has markedly cut back my large NVDA position, and I am reluctant to buy it back. As great as a company it might be, the growth is bound to slow, and with it the PE. I see AAPL and GOOG, and maybe AMZN as the real beneficiaries of AI, as they will have products they can sell for money to people, at a slightly lower valuation. JMHO

Jobs and wage data/Purchase apps not lifting yet with drop in mortgage rates

ADP said in July that the private sector added a net 122k jobs, 28k less than anticipated and down from 155k in June (revised up by 5k). The service sector in particular added just 85k jobs with gains in trade/transportation/utilities of 61k, leisure/hospitality of 24k, education/health services of 22k, financial activities of 14k and ‘other’ of 19k, partly offset by declines of 18k in information and 37k in professional/business services.

The goods producing side was mixed too as construction added 39k but manufacturing shed 4k.

Medium and large companies drove almost all of the hiring. Small businesses with 20-49 employees lost 22k jobs, mostly offset by a gain of 15k for those with 1-19.

With respect to the wage side, for ‘job stayers’, wages rose 4.8% y/o/y vs 4.9% in June. For ‘job changers’, wages were up 7.2% vs 7.7% last month. While further decelerating, these are still big gains.

Smoothing out the monthly volatility points to the moderation in the rate of hiring with the July print in particular the slowest since January. The 3 month average is 145k vs the 6 month average of 168k, the 12 month average of 147k and vs the 2023 average of 209k.

Bottom line, the softening of the labor market in terms of slackening demand for new workers and the modest pick up in the pace of hiring’s seems to be happening in slow motion but happening nonetheless and gives the Fed some reason to tweak its interest rate policy.

Treasury yields are at the lows of the morning in response to the jobs miss.

Also helping was the Q2 Employment Cost Index which rose .9% q/o/q, one tenth less than expected. Specifically with the private sector, wages/salaries rose .8% q/o/q, down from 1.1% in Q1. On a y/o/y basis, private sector wages and salaries grew by 4.1% vs 4.3% in the two prior quarters and vs 4.5% in the one before that.

Bottom line, wage growth continues to slow but some of this is just base effects, along with the greater supply of labor at the same time demand is lessening.

Finally, the weekly MBA mortgage application data saw a drop of 3.9% w/o/w with purchases lower by 1.5% and down for a 3rd straight week. Refi’s fell 7.2% w/o/w. Bottom line, even as mortgage rates have moderated, at least in this data we’ve seen no improvement in purchase applications just yet.

-BDTX +3.6% (Raymond James Initiates BDTX with Outperform, price target: $20)

-BWA +3.2% (earnings, guidance)

-COR +3.0% (earnings, guidance)

-MA +3.0% (earnings, guidance)

-KKR +2.1% (earnings)

Downside:

-FGEN -45% (Pamrevlumab arm of Precision PromiseSM study in metastatic pancreatic cancer did not meet primary endpoint of overall survival; to reduce U.S. workforce by approximately 75%)

-PEPG -36% (announces data from Low-Dose Cohort of PGN-EDO51 in ongoing CONNECT1-EDO51 Phase 2 clinical trial for treatment of Duchenne Muscular Dystrophy)

-MGNX -25% (provides Vobramitamab Duocarmazine update; agrees with IDMC recommendation to discontinue study for remaining mCRPC study participants who potentially could have received additional doses)

-BGFV -17% (earnings, guidance)

-PEN -17% (earnings, guidance)

-NARI -15% (earnings, guidance)

-OI -14% (earnings, guidance)

-SLS -13% (announces $21M registered direct offering priced at a premium to market)

I added to the VKTX weakness late in the day yesterday.

I viewed the Merck MRK comments during EPS call as constructive (below) - though the market disagreed:

Yeah. No, Chris, thanks for the question. Obviously, we discussed what we did in the quarter with EyeBio and Elanco Aqua business. We're going to continue to follow the same strategy we've been looking at, which is really focusing on the science and looking at how can we best continue to drive where we see a scientific opportunity that matches our portfolio and our skill set to bring that in more in the earlier-stage settings and with some mid-late, but clearly not commercialized products more to build the pipeline.

So the continuation of the strategy we've been following, we continue to have the financial flexibility to consider deals of all sizes. But as we've pointed out in the past, we tend to look in that $1 billion to $15 billion is a good indication of where we would most likely play. And to the obesity question specifically, our view continues to be that if we can find opportunities to look at next-generation plays in that space, those will be things we will continue to evaluate and consider.

We don't believe going after today's first generation is the place to play. So it will continue to be looking at second and third-generation waves of innovation, whether it be around oral delivery, looking for where there's high tolerability, combined ability and/or preservation of muscle mass. Those are the areas of focus for us. And if we see something, we continue to have the capacity and the interest to act.

From The Street of Dreams: Rotation, Microsoft, and the AI Trade

From JPMorgan:

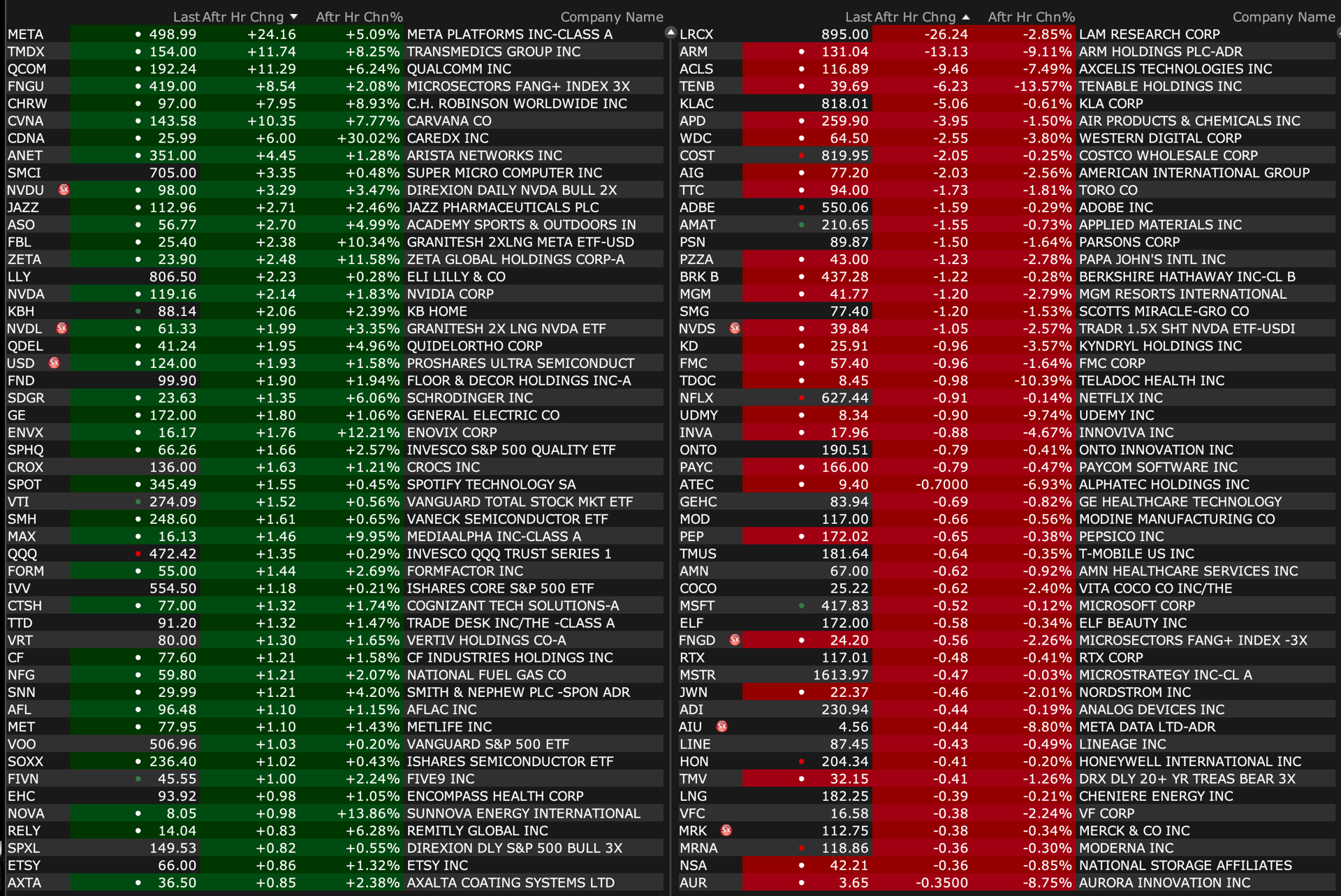

US: Futs are higher with Tech leading with Semis outperforming. NVDA +5% pre-mkt following AMD’s earnings (+9.3%) and positive read-thru from MSFT earnings. MSFT -2.9% having cutting losses from as much as 7% and is the only member of Mag7 in the red. The AI trade appears to remain intact. Bond yields flat and USD is weaker. Cmdtys are higher led by Energy following yesterday’s supply drawdown and relief rally as WTI has seen ~8% drawdown this month. Today, we receive ADP (which has not been predictive of NFP) and the Fed decision. Mag7 EPS continues with META.

and...

EQUITY AND MACRO NARRATIVE: The rotation resumed yesterday with Tech and Semis dragging SPX/NDX lower as investors sold NVDA ahead of MSFT earnings. There was a bit of a midday rally punctuated by $3.5bn MOC to buy. Post-market earnings were net positive, and we are seeing a bit of a risk-on rally in APAC/EMEA markets following BOJ’s decision. The most important update is on AI, eloquently written by our Industrials Sector Specialist Paige Hanson.

· Anyone who is long AI/data center exposure in industrials (pick your poison: VRT, ETN, GEV, etc) had their stomach sink at 4:01p upon seeing red headline after red headline hit on the MSFT print and how much the stock was dropping after hours. I didn’t want to add to noise/fears so stayed in my lane to cover the industrial prints post-close, but revisited MSFT transcript and skimmed headlines of other tech prints to take a stab at reads for the VRT type names but also just to get a sense for how much pain the market would be in because let’s face it… we’re all covering AI right now no matter what sector you cover since it has driven the market for 18 months. My 2c is that there is actually enough evidence in tech prints tonight that suggest to me that growing AI fears lately on fears of capex stalling/slowing or lack of monetization proof (essentially any way for ppl to try to call peak on AI spend) is not necessarily occurring in the fundamentals nor in the company’s messages as much as one would think reading news or looking at how any of these stocks have traded in the last 6 weeks. Incidentally, that’s what I took away from GOOG print last week as well and was perplexed to see many blame AI pressure late last week on the GOOG print which had better capex and commentary that risk of under-investing is “dramatically” higher than risk of over-investing.

· MSFT’s Q&A was very much focused on the capex breakdown in terms of cadence of spend within the breakdown of total capex spend, and how to think about that holistically on capex: on the breakdown, the co said about half of total capex is infrastructure buildout (building of data centers, leases etc) while half is servers, with the latter being demand-driven (i.e. look to items like Azure growth rates as an indication since the “pace at which they fill” those builds with CPUS/GPUS can fluctuate to match demand and is therefore more real-time). On the contrary, the infrastructure spend portion of total capex spend has a much different life cycle as well as cadence of spend during the life cycle of those assets, and is taken to be more upfront in nature which is part of the reason why AI bears have expected that co’s will not be able to continue to accelerate capex spend and it could stall out or slow from elevated levels. To be diplomatic, I do think the co gave some pieces to both bulls & bears on this front as they did confirm an analyst’s question that it would be possible to see consistent revenue growth without more of this elevated capex number continuing to accelerate, but then also said in the 10k explicitly that they “expect capital expenditures to increase in coming years to support growth in our cloud offerings and our investments in AI infrastructure and training.” Specifically, as it goes to the items that fill the data centers (ie what we care about in our industrials world!), that is tied to the demand-side of the capex spend, and CFO said they expect Azure growth to accelerate in 2H of FY25: “expect Azure growth to accelerate as our capital investments create an increase in available AI capacity to serve more of the growing demand.” I am no MSFT/tech expert, and would love to hear other reads, but I don’t see how folks can think that this is peak orders for a name like VRT if that is the message from co’s like MSFT about the demand driving a need to accelerate the capex spend that is more real-time and not the longer-cycle, more upfront half of the capex spend. Other headlines tonight from tech co’s included AMD’s “AI investment cycle will continue to be strong”, and ANET: “AI strength drives double-digit growth; affirms AI lift and positions for 2025”…

· So maybe we are past the “buy it all as fast as you can” phase of the AI trade, but there seems to be a lot of bottoms-up evidence from tech companies that demand continues to be strong so maybe that translates into a more discerning approach to the AI trade about what part of the data center buildout life cycle each co serves, but either way I truly don’t think the mosaic of messages on AI from tech co’s suggest that undiscerning AI selling can/should continue.

The Beginning of the End (or The End of the Beginning) for Mag7?

"Most people get interested in stocks when everyone else is. The time to get interested is when no one else is. You can't buy what is popular and do well."

- Warren Buffett

"I don't care to belong to a cIub that accepts people like me as members."

- Groucho Marx

I am inclined, as you can gather from my frequent and continuing series ("Tales From Nvidia") as well as my Dairy's daily comments that the recent fall from grace for the Magnificent 7 stocks is the beginning of the end (and the first blow) rather than the end of the beginning.

Mag7 valuations, as I have chronicled, have rarely been more stretched - both absolutely and relatively. The sector is still very overowned and, as important, (uber) confidence in the future has only taken a small dent. Moreover, even the anointed Mag7 is not immune to an economic slowdown (particularly by the consumer).

Leadership changes rarely occur in a flat or higher market backdrop.

To this observer we appear to be in a late (economic and market) cycle in which an overweight position in equities may not be justified - especially against interest rates and the numerous economic, policy, social, political, geopolitical and valuation headwinds.

The recent rotation away from technology is now getting overdone as well (providing some shorting fodder) - and a mean reversion (and fall in the indexes) is likely in the weeks and months ahead.

Note: My view is an educated guess based on my own analysis of the fundamental data and valuations (and not by observing the colorful outfit worn by Dan Ives this morning in the business media). Others feel differently. In fact, today, in the business media you will hear - with certainty - that the drop in tech stocks is just a bump in the road from the crown that is often wrong but never in doubt. As to me, I am often wrong and always in doubt. I weigh probabilities against scenarios (from very pessimistic to very optimistic) in order to ascertain "fair market value." So, I may be wrong (especially if my input is wrong), but my conclusions are based on analysis (which you read daily in my Diary) and not narrative.

Geopolitical risks, a continuing concern of mine, are now back on the front burner. (The Microsoft MSFT EPS disappointment has deflected the focus, but I suspect the focus by investors will be renewed in equities and maybe in the oil market).

From my pal Whitney Tilson:

Holy cow – I just woke up to this bombshell news: after what was widely believed to be a “proportionate” response to a Hezbollah rocket attack that killed 12 Israeli children last week (likely by accident – there was a military base nearby), killing Fuad Shukr, a senior member of Hezbollah, in Beirut, Israel just ramped things up in a MAJOR way by killing (not sure how) Ismail Haniyeh, a senior Hamas commander and the Former Prime Minister of Palestine in Gaza while he was IN IRAN for the inauguration of Iran’s new president.

It would be as if Putin assassinated one of his enemies in DC who was attending our presidential inauguration on Jan. 20.

This is a MUCH bigger escalation than Israel’s strike on Iranian commanders in Syria in April led Iran to fire hundreds of missiles at Israel.

Iran, by itself and through its proxies, has no choice but to retaliate in a MAJOR way, which dramatically increases the odds of all-out war across the Middle East.

My quick thoughts:

Israel, the U.S. and their allies need to be ready to shoot down even more hundreds of missiles and drones – and anything else.

The U.S. might have to get directly involved – for example, flying fighter jets missions over Lebanon if things get hot with Hezbollah.

The idiots who think Biden/Harris/Schumer/Democrats don’t support Israel will have to shut the fu*k up when they see how strong their/our support is when push comes to shove.

While I of course celebrate the death of any terrorist with so much blood on his hands, any possibility of a ceasefire and return of the hostages has now been pushed off far into the future, and now Israel faces the danger of a much larger multi-front war.

I think there are reasonable arguments on both sides of the debate whether Israel was smart to assassinate Haniyeh – but I wish I had more certainty that, in ordering the strike, Netanyahu truly had only Israel’s long-term interests in mind, rather than maintaining his own power/office and further delaying the trial for the crimes he was indicted for in 2019 (breach of trust, accepting bribes and fraud).

Hamas accused Israel of killing Ismail Haniyeh, who was in Tehran for the inauguration of Iran’s new president. He was a key player in negotiations to stop the fighting in Gaza.

...

Ismail Haniyeh was in Tehran to attend the inauguration of Iran’s new president.

...

Now, the focus is on how Hamas and Hezbollah will respond to the attacks on their leaders; how Iran will react to a strike on its territory; and whether either reaction leads to the outbreak of a wider regional war. An Israeli strike on Iranian commanders in Syria in April led Iran to fire hundreds of missiles at Israel. Iran’s supreme leader, Ayatollah Ali Khamenei, said Haniyeh’s assassination would prompt a “harsh punishment.”

“Most people get interested in stocks when everyone else is. The time to get interested is when no one else is. You can’t buy what is popular and do well.”