Closing Market Internals

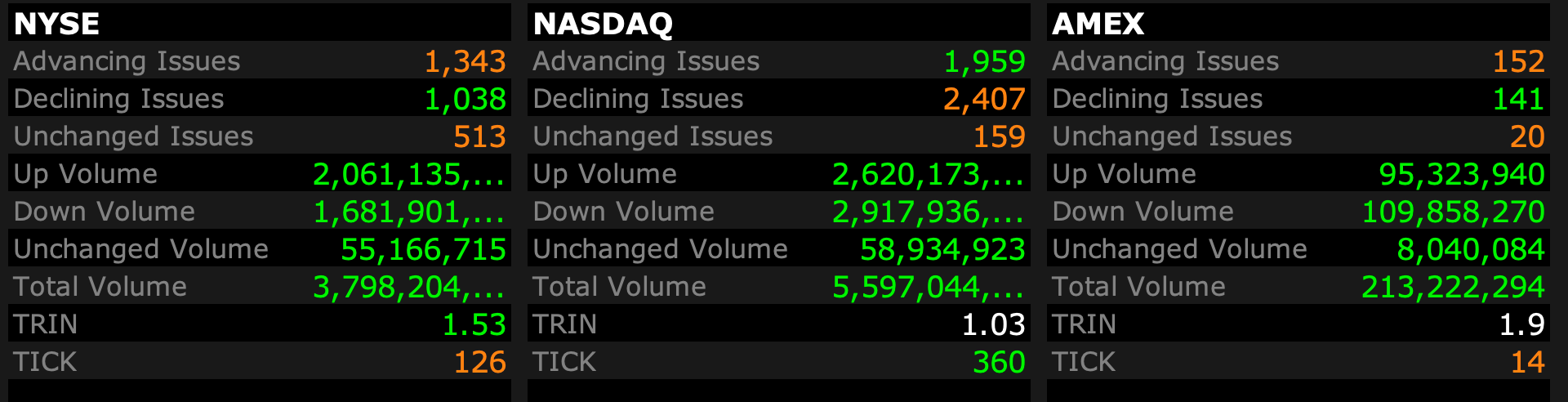

Closing Breadth

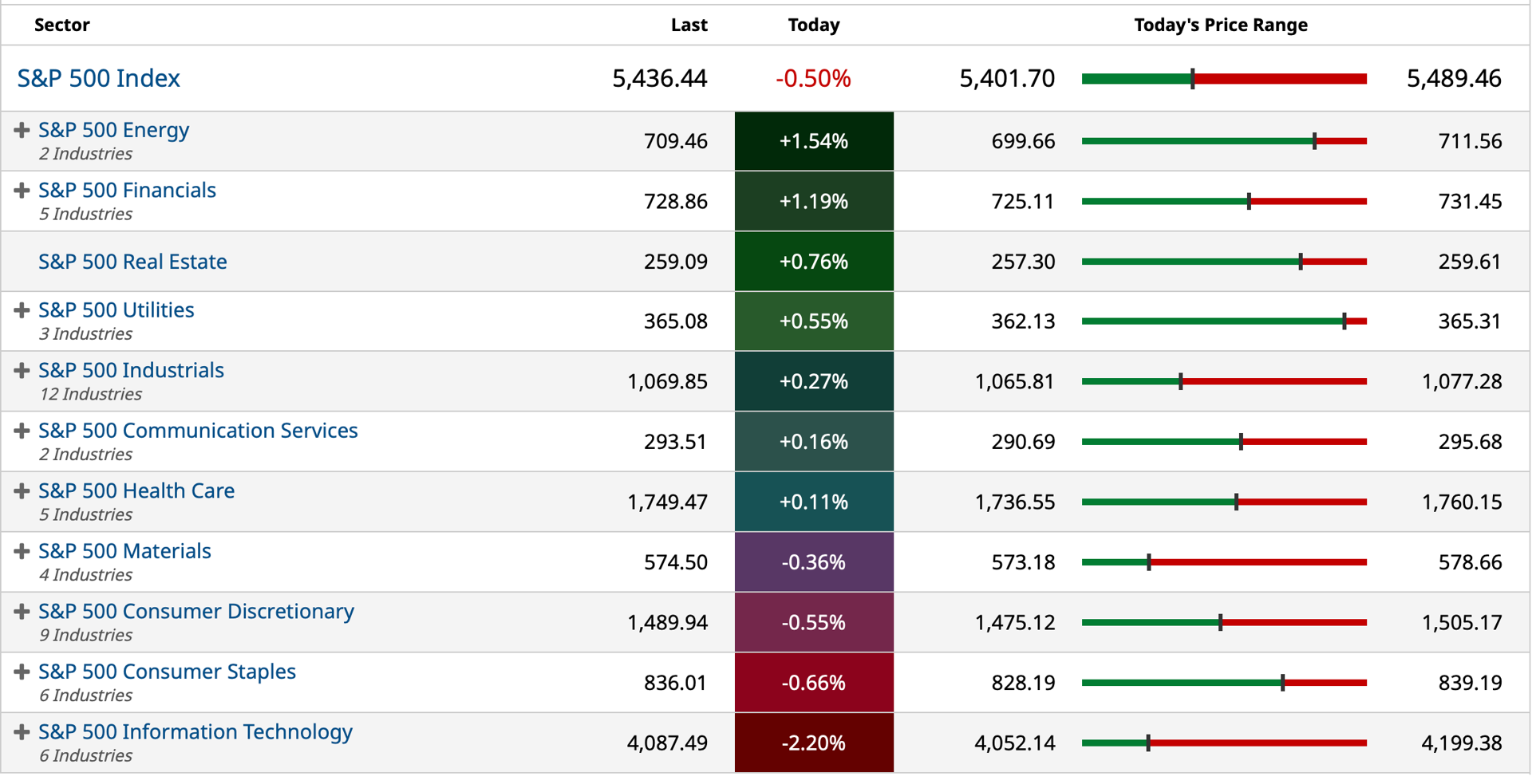

S&P 500 Sectors

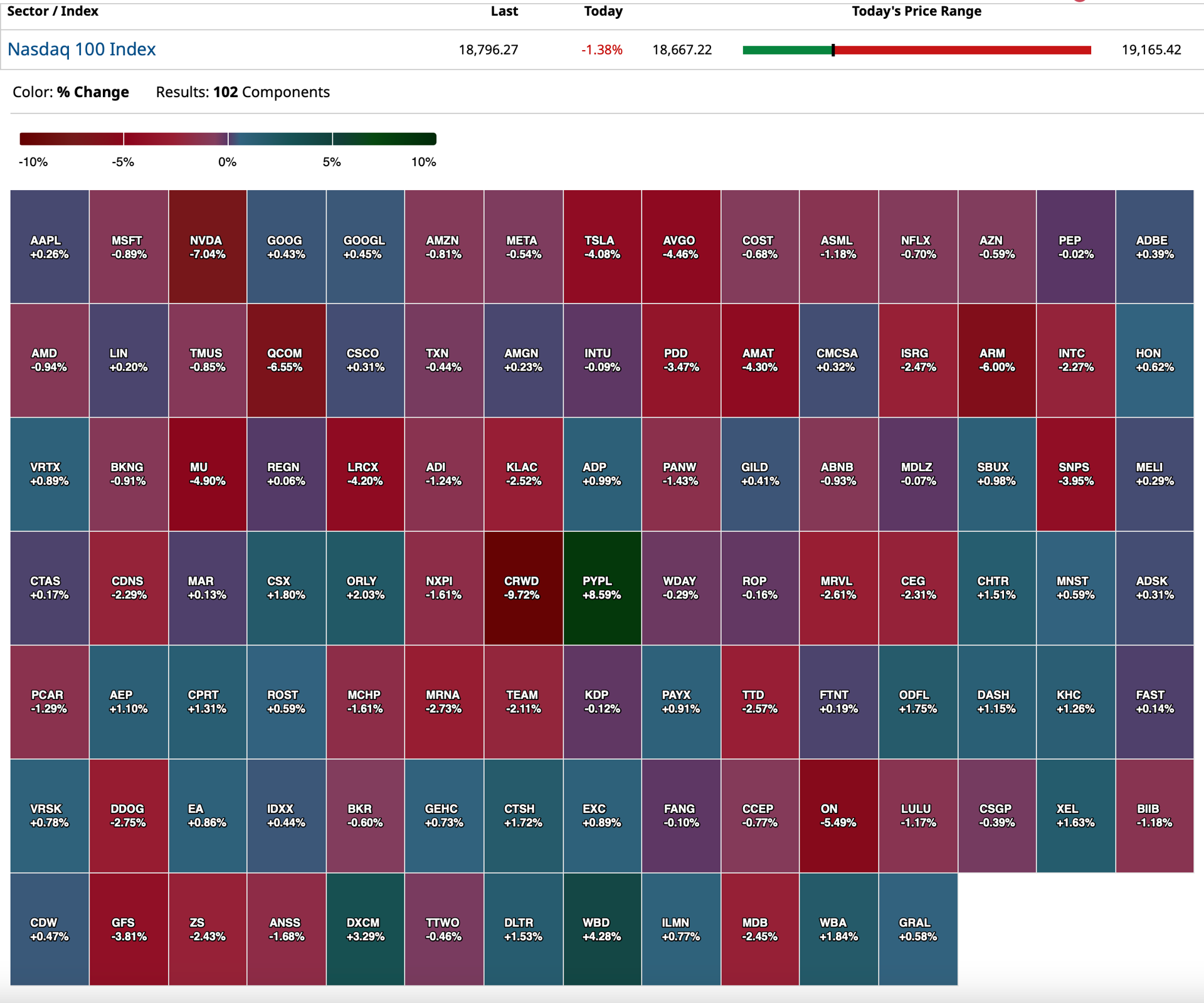

Nasdaq 100 Heat Map

BY Doug Kass · Jul 30, 2024, 5:00 PM EDT

BY Doug Kass · Jul 30, 2024, 5:00 PM EDT

BY Doug Kass · Jul 30, 2024, 4:25 PM EDT

"Just one more thing."

- Lt. Columbo

Tonite on the shows we will be told that everyone sold out at the high on Monday...

BY Doug Kass · Jul 30, 2024, 4:20 PM EDT

Thanks for reading my Diary today.

I am still a bit roughed up from my illness so I will be calling it a day.

Enjoy the evening.

Be safe.

BY Doug Kass · Jul 30, 2024, 3:50 PM EDT

BY Doug Kass · Jul 30, 2024, 3:28 PM EDT

I am back shorting Goldman Sachs GS at $507.35.

BY Doug Kass · Jul 30, 2024, 2:36 PM EDT

The early end-of-month (July) markup in the winners (e.g. GS, homebuilders, etc.) is as conspicuous as it is breathtaking.

BY Doug Kass · Jul 30, 2024, 2:01 PM EDT

Wolf Street howls about "Peak Housing."

BY Doug Kass · Jul 30, 2024, 1:32 PM EDT

Another good one from Bret:

Bret Jensen

Echoing what Dougie said earlier about consumer facing corporations

Wells Fargo on Tuesday expressed some concerns related to the consumer stemming from the second quarter earnings season so far.

“2Q24 SPX earnings are coming in ahead of consensus, but the rate of sales beats is disappointing and consumer commentary has been mostly negative,” Wells Fargo's Christopher Harvey said in an investor note.

When looking at large-caps, Wells Fargo noted that 44% of the S&P 500 names have beat sales consensus estimates, which is well below the typical 60% rate. At the same time, small-caps, similar to large-caps are also beating less frequently on the top line.

Taking it a step further, when looking at companies such as McDonald's (MCD), Nike (NKE), Delta Air Lines (DAL), Lamb Weston (LW), and Pool Corporation (POOL), see what Wells Fargo spotlighted in some of the consumer notes from the 2024 earnings transcripts:

BY Doug Kass · Jul 30, 2024, 1:17 PM EDT

* Of a uranium-kind

In mid-June I sold out URNM above $58.

Last sale $44.43!

From six weeks ago:

Damn good out in Sprott Uranium Miners ETF (URNM) above $58 recently, now -$1.70 on the day and -$8 from the recent sale price.

Position: None

BY DOUG KASS JUN 11, 2024 10:40 AM EDT

BY Doug Kass · Jul 30, 2024, 12:52 PM EDT

From Peter Boockvar:

Consumer confidence mixed/Private sector job openings near 3 1/2 yr low

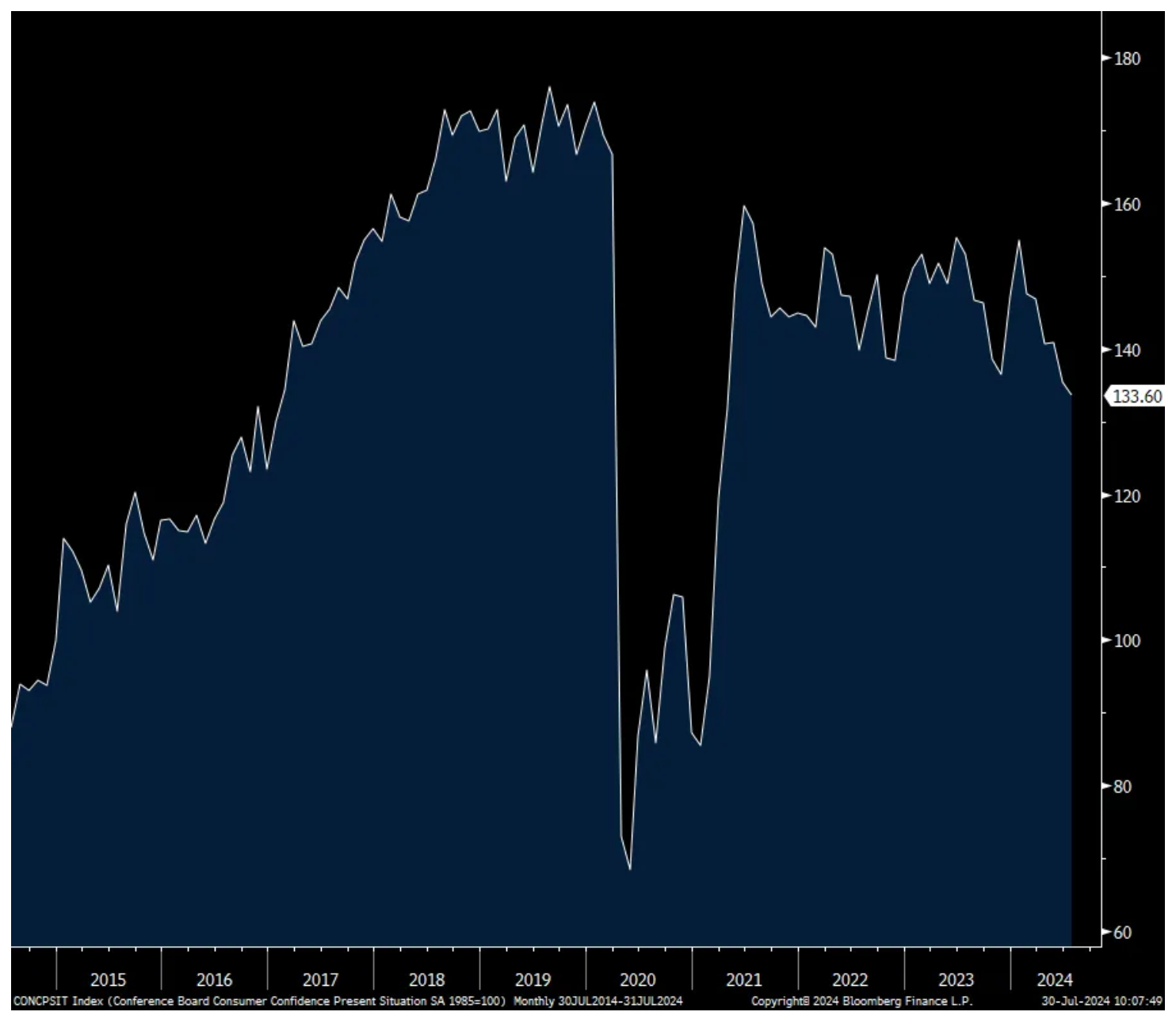

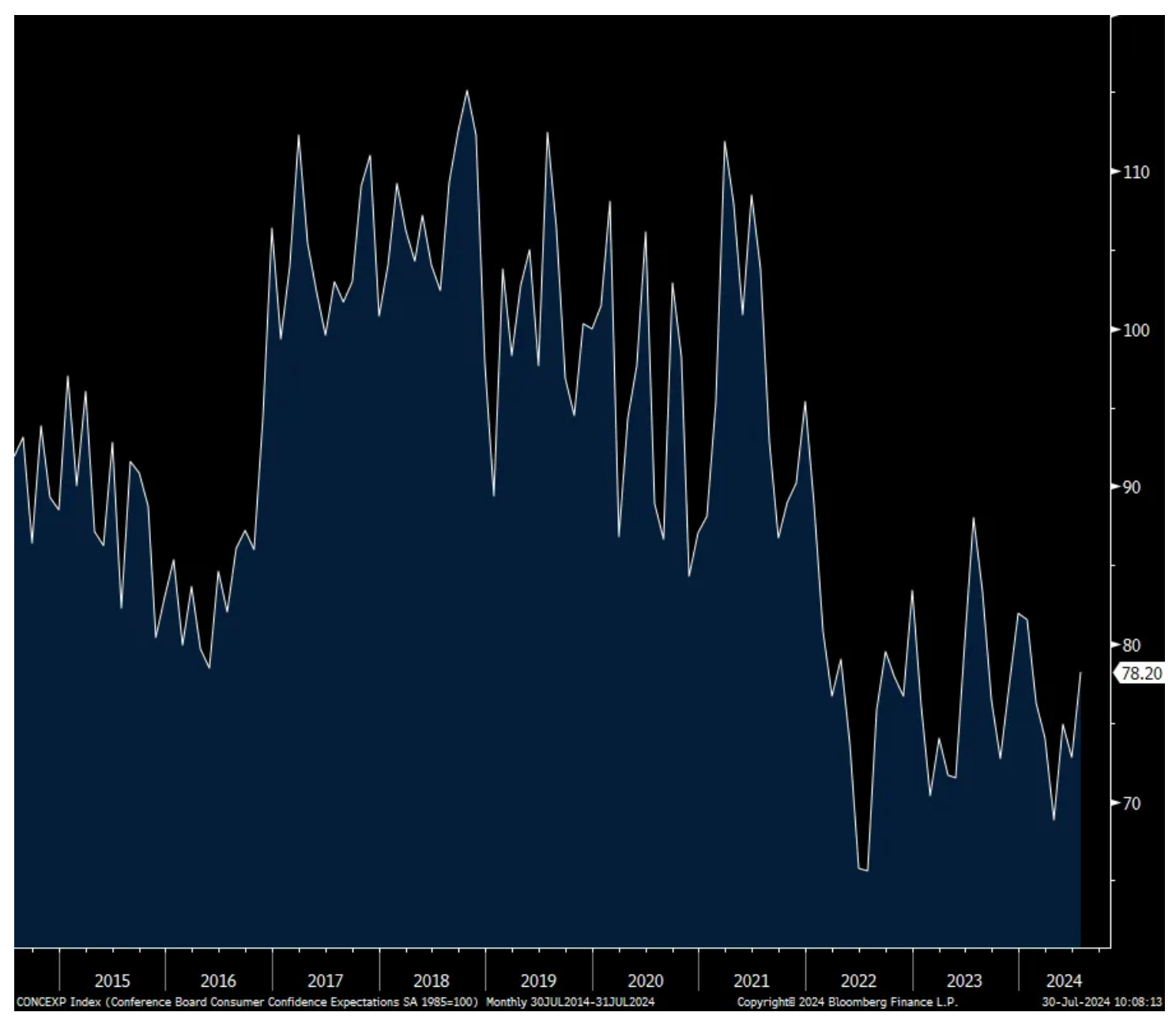

The July Consumer Confidence index from the Conference Board was 100.3, about in line with the estimate of 99.7 and compares with 97.8 in June (revised up from 100.4 initially) and 101.3 in May. There has been an interesting divergence with the two main components this year. The Present Situation has fallen to the lowest level since April 2021 and go back to January 2017, not including Covid, the last time it was lower. On the flip side, while still pretty depressed, the Expectations component rose to the highest since January.

The differential can be explained by the labor market answers. People are more worried now but hopeful in the coming 6 months things will improve, albeit slightly.

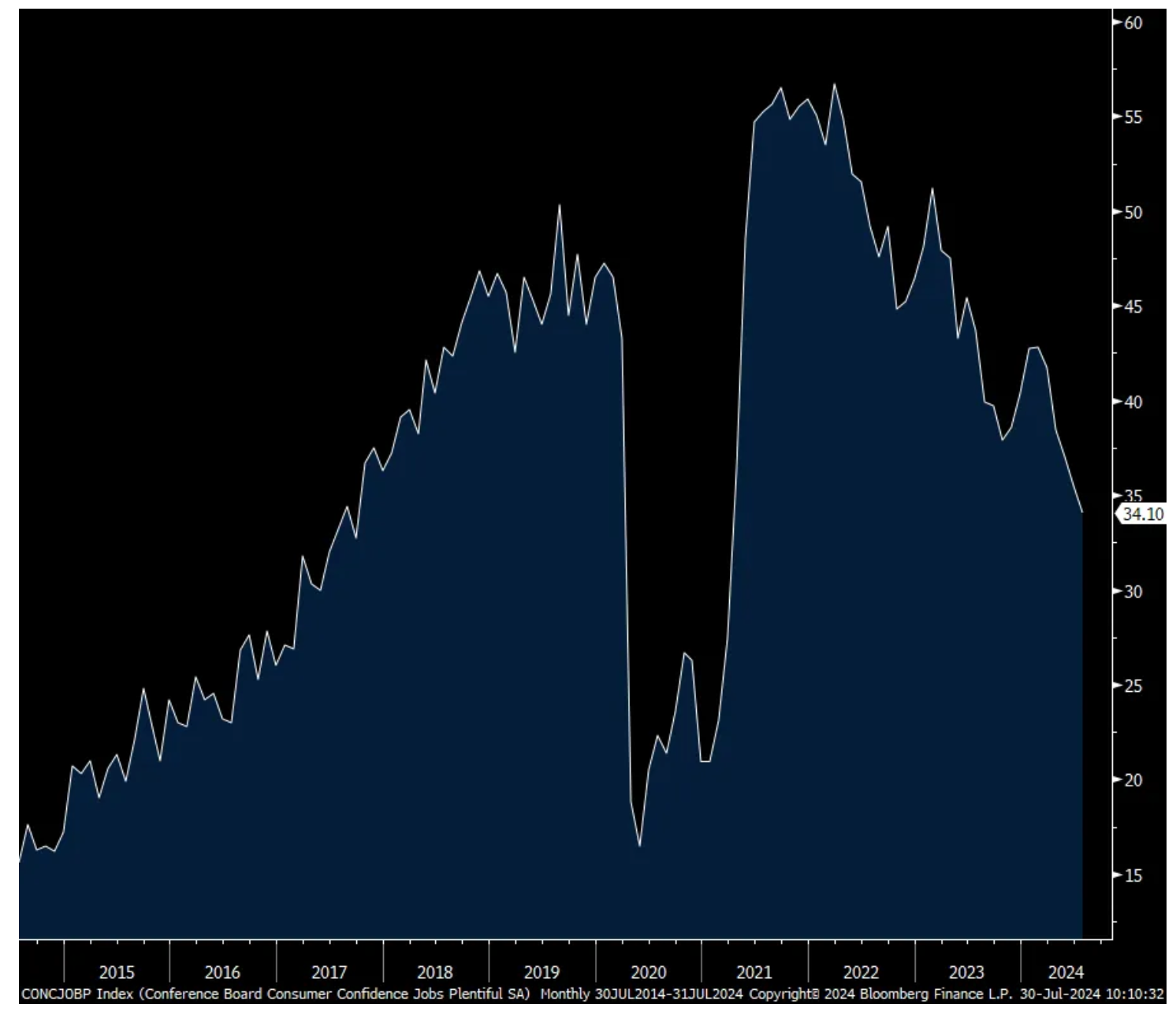

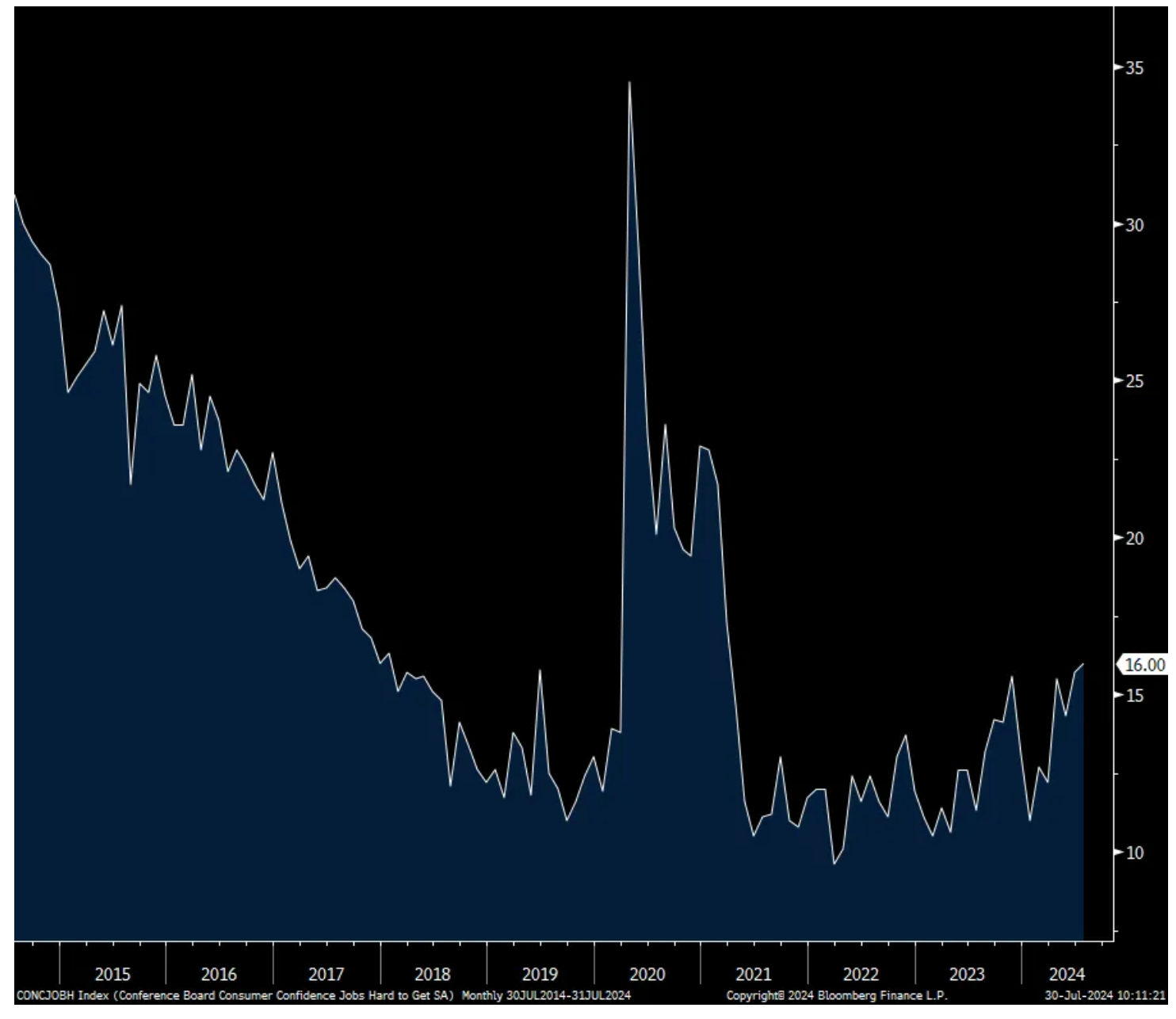

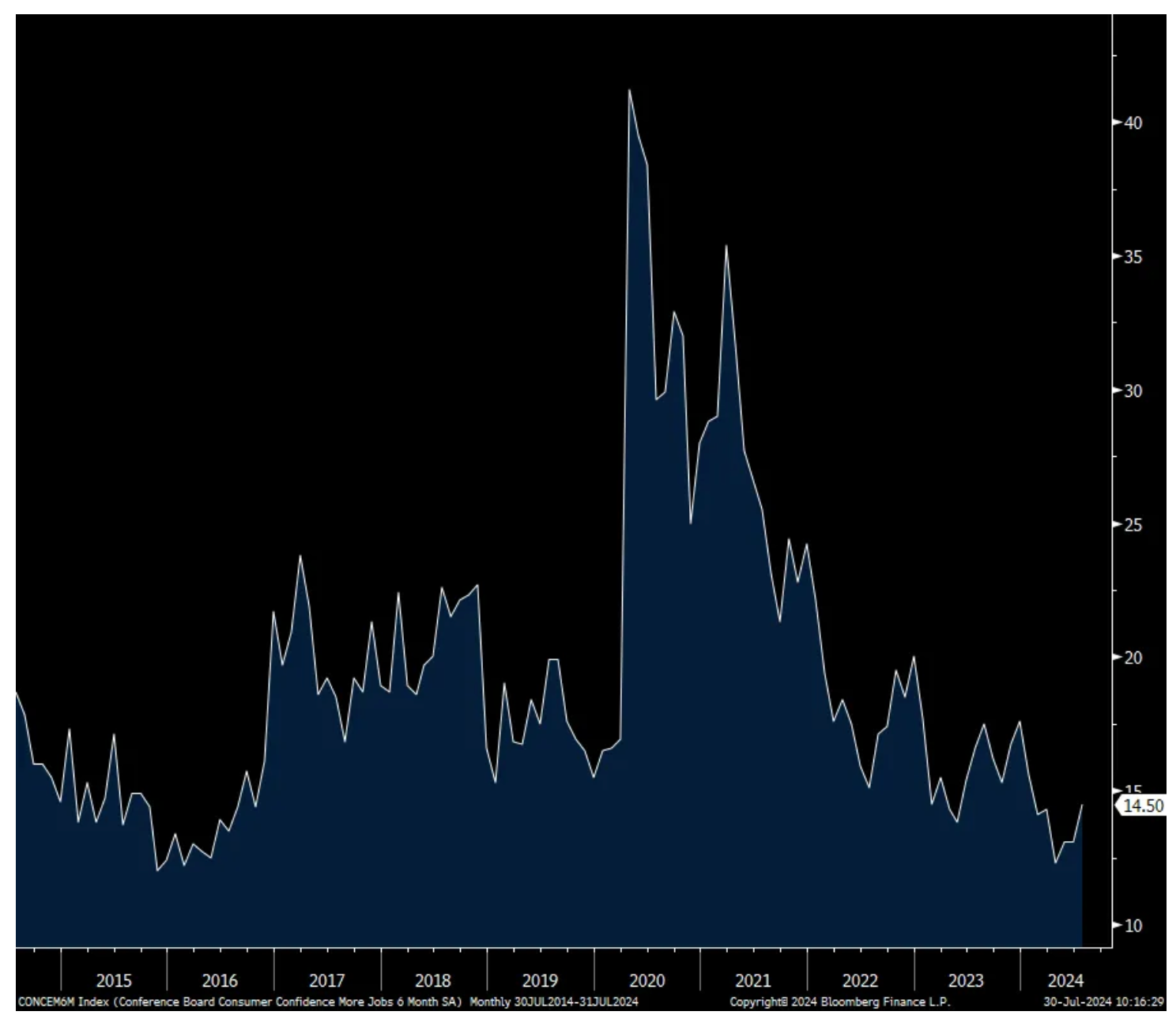

Those that said jobs were currently Plentiful fell to the lowest level since March 2021. Jobs Hard to Get rose to the most since March 2021. On the other hand, those expecting ‘more jobs’ in 6 months rose to the highest since January, though still remaining very low. Adding further to the unevenness, the 6 month outlook for ‘higher income’ fell to match the lowest since February 2023.

One yr inflation expectations held at 5.4% for a 3rd straight month and remaining in a tight range of 5.2%-5.4% this year.

Spending intentions continued to weaken. Expectations to buy a home fell almost 1 pt m/o/m to just 4.2, the least since 2013. Intentions to buy a car fell to the lowest since last October. Plans to buy a major appliance declined to a 3 month low.

In terms of demos, confidence rose to the highest of the year for those under the age of 35 but for those 35-54 yrs old fell to the lowest since November 2020. It rose to a 3 month high for those 55 and over.

Bottom line, combine the data here and what we’ve heard from so many consumer touching businesses and we know all about the divergent state of the US consumer.

Present Situation

Expectations

Jobs Plentiful

Jobs Hard to Get

Expecting ‘More Jobs’ in coming 6 months

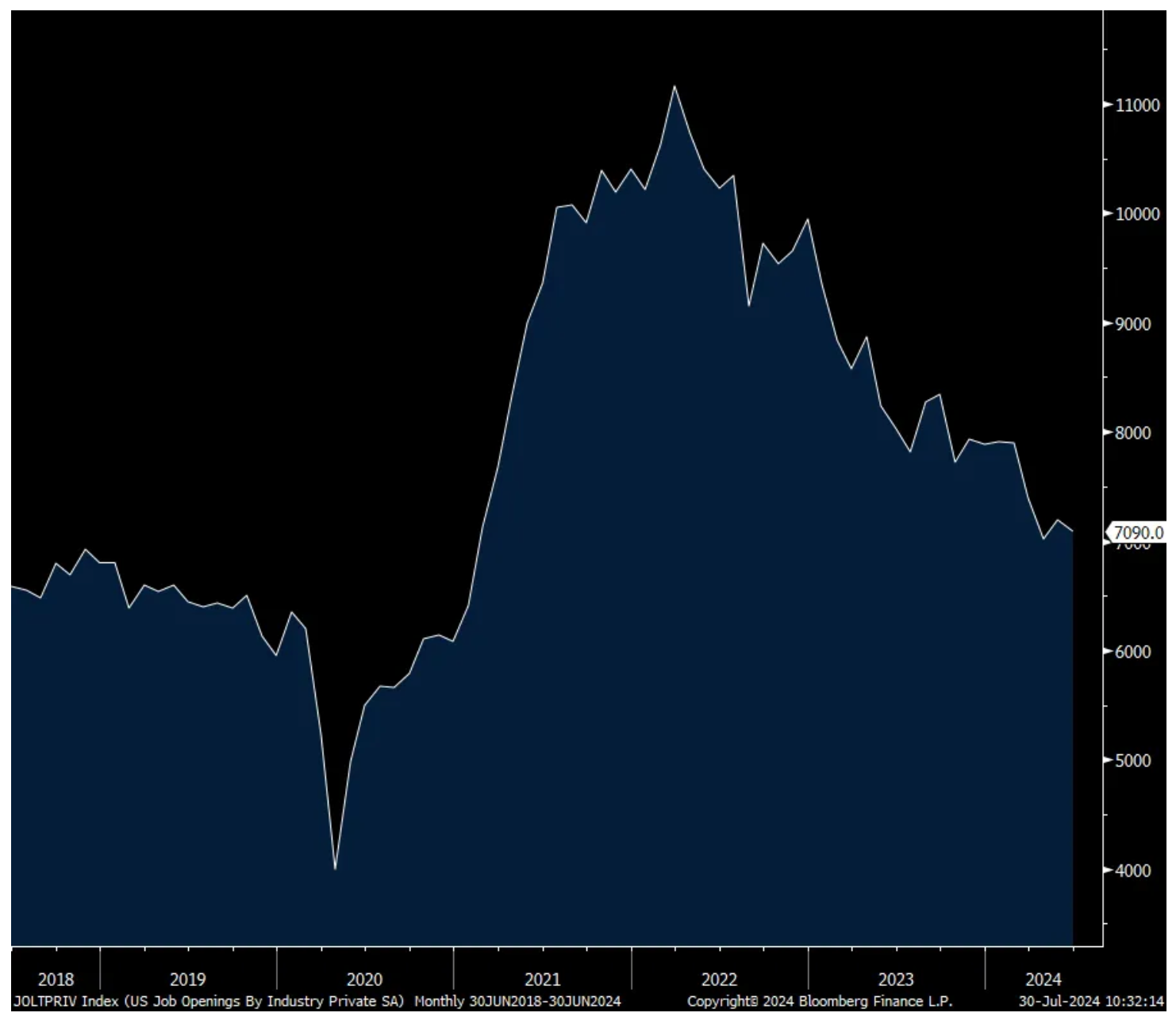

Somewhat dated, and with questions on some possible double and triple counting, job openings in June totaled 8.18mm, down slightly from the 8.23mm seen in May. That though is above the forecast of 8mm.

A factor keeping the figure above 8mm is the growing demand for workers from state and local governments. As for the private sector, job openings fell to 7.09mm and that is the 2nd lowest since early 2021 and nearing its pre Covid pace when we didn’t have work from home as a thing.

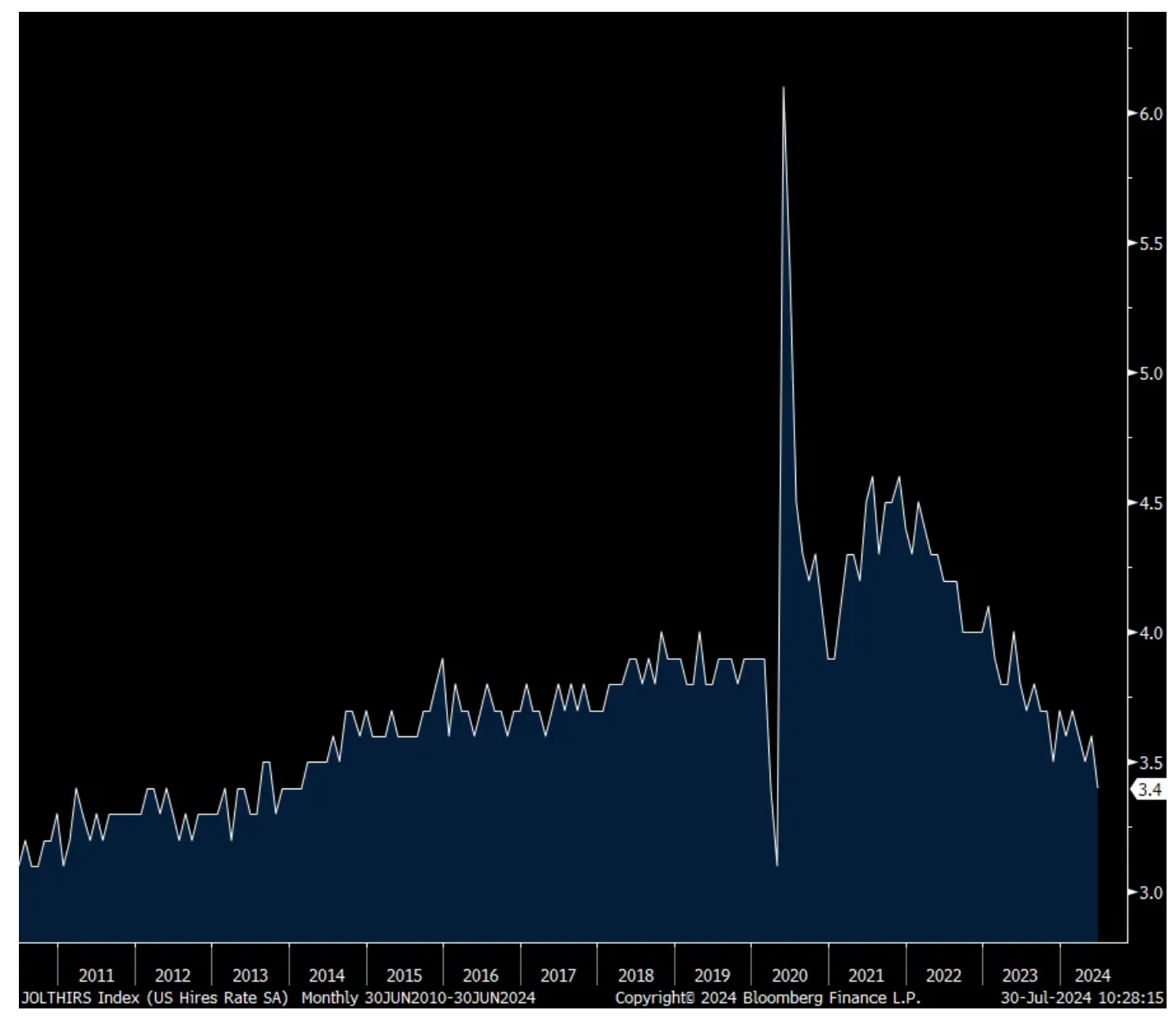

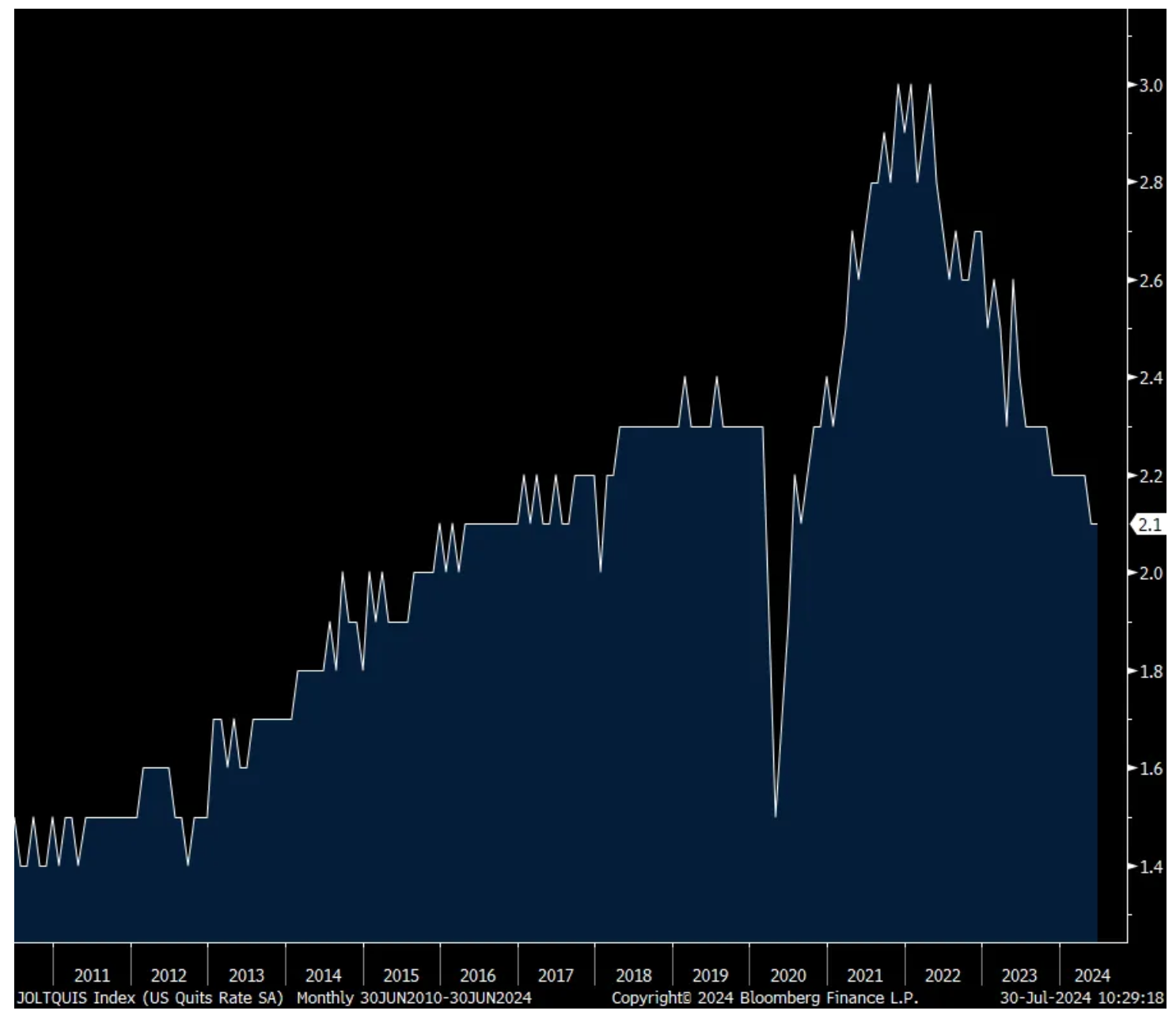

A growing issue too in the month was the hiring rate which fell to just 3.4% which is the slowest since 2013 not including Covid and not far from the Covid low of 3.1%. The quit rate at 2.1% is the lowest since 2018, also taking out Covid data.

Bottom line, the labor market is seeing a more muted demand for new workers at the same time we’re seeing a pick up in firing’s, albeit somewhat, as seen in the initial claims data.

Private Sector Job Openings

Hiring Rate

Quit Rate

BY Doug Kass · Jul 30, 2024, 11:51 AM EDT

In the last few months I have written over 30 "Tales From Nvidia."

NVDA shares are now at $105 or -$36 below its yearly highs.

BY Doug Kass · Jul 30, 2024, 11:35 AM EDT

Gartner predicts “at least” 30% of AI projects will be abandoned. That is a lot of excess capacity...

BY Doug Kass · Jul 30, 2024, 11:16 AM EDT

Check out SPY, QQQ and the Magnificent 7 on this chart:

BY Doug Kass · Jul 30, 2024, 10:50 AM EDT

"Last summer, for instance, Chevron created an Enterprise AI team, tasked with finding new AI applications that could bring value to the company. The team is still looking for such an app, Braun (Chevron CIO) said, and he isn't yet convinced that large language models will significantly transform Chevron's business or save the company money by making employees more productive."

https://www.theinformation.com/articles/a-reality-check-on-ai-with-chevrons-cio

Side point, I do find this disturbing. Teach children not to think or write? Big tech does it again. They don’t care.

https://www.cnn.com/2024/07/29/tech/googles-ai-olympics-ad-backlash?cid=ios_app

BY Doug Kass · Jul 30, 2024, 10:10 AM EDT

Adding to shorts on early market ramp - homebuilders, AXP $250.75 (new name) and others.

BY Doug Kass · Jul 30, 2024, 9:51 AM EDT

From Boockvar:

I agree with the case for the Fed to cut rates tomorrow, a tweak as I've referred to it but understanding they will most likely go in September instead. I was ok with Alan Blinder's argument in yesterday's WSJ for most of his piece but then he lost me when he said if the Fed cut Wednesday, "I believe the markets would stand up and cheer." He revealed the Fed's unspoken 3rd mandate of trying to please the markets. The last time they did that we ended up with 9% inflation (and would have been in the double digits if home prices instead of rents were used).

Interestingly, in the same WSJ, ex Fed Governor Kevin Warsh wrote a piece mostly focused on the Fed's balance sheet and said "Much of Wall Street applauds the Fed's big balance sheet and monetary dominance in Washington. Households and businesses on Main Street have far less reason for enthusiasm" and that is because of the inflation the former has stoked. I would welcome Warsh as the next Fed chair if he was given the opportunity.

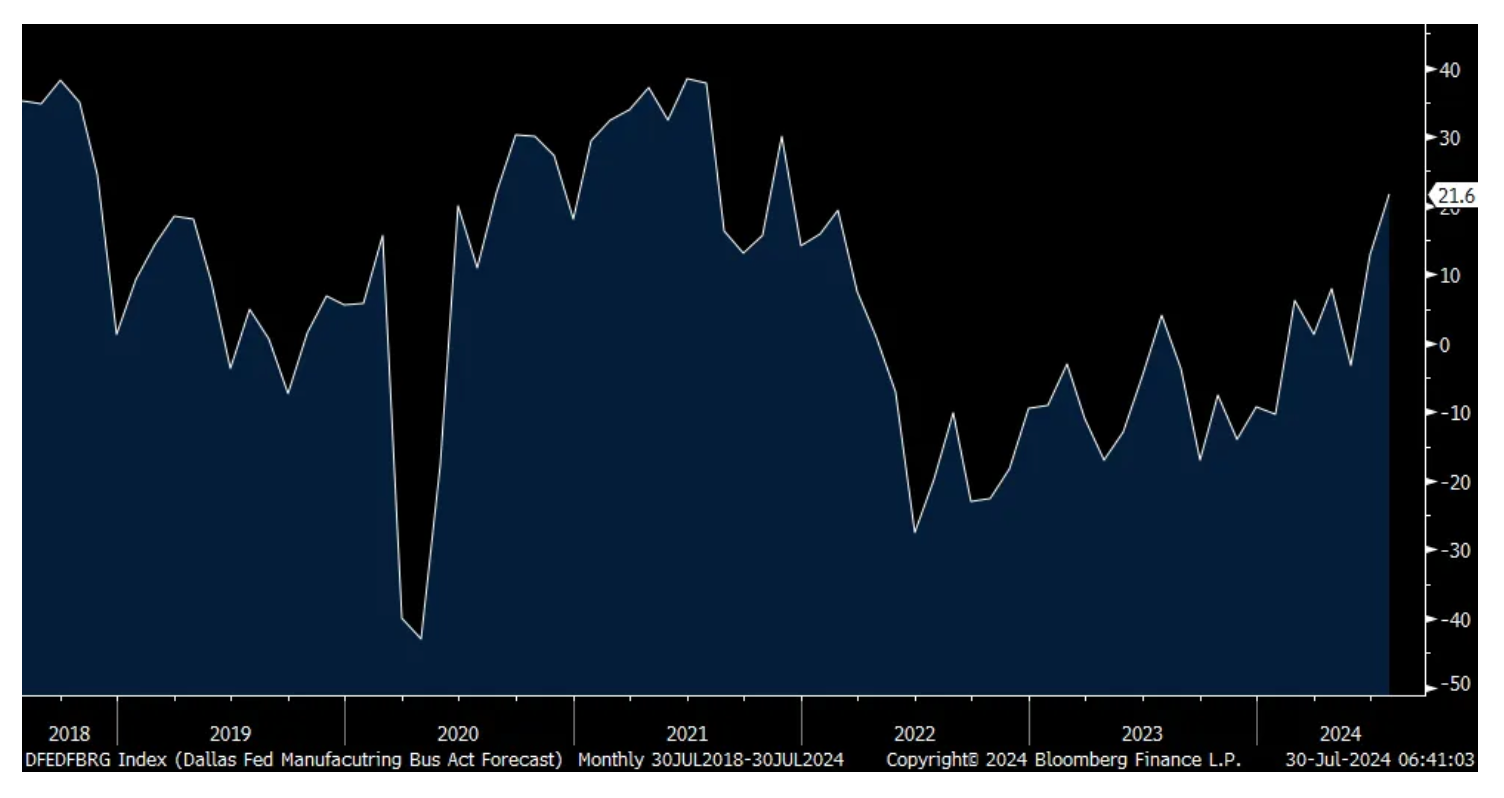

The July Philly manufacturing index remains the outlier as yesterday the Dallas regional survey joined NY, Richmond and KC in reporting a contraction. Its index came in at -17.5 vs -15.1 and it was last above zero in April 2022. The bright spot though was hopes for improvement from here as the 6 month business activity outlook rose to 21.6 from 12.9 and that was the highest since November 2021. Thursday's ISM manufacturing index is forecasted at 48.8, thus remaining in recession.

Dallas Mfr'g 6 month Business Outlook

Here were some comments, and I won't include ones that talk about the hurricane or politics:

"Activity has slowed down, but we anticipate an uptick soon." - Paper Manufacturing

"Customer demand is the overriding concern. Decreased credit availability and affordability for the markets we sell into have all but stopped demand. I estimate we are operating at 30-40% capacity." - Fabricated Metal Product Mfr'g

"Business activity is horrible, and we are seeing no signs of improvement." - Machinery Mfr'g

"Inquiries and orders activity has seemingly halted. The brakes are on. This is pretty common in presidential election years, but this comes at a time when things were already volatile due to price pressures and massive inflationary pressures." - Machinery Mfr'g

"Many customers are holding off on expenditures as well as allowing for cost-of-living adjustments to prices. The market continues to be soft, and with uncertainty in the election year, even our federal business is a bit stagnant." - Computer & Electronic Product Mfr'g

"We need lower interest rates, so end customers resume buying capital equipment again." - Computer & Electronic Product Mfr'g

"We are expecting to see stronger signs of a cyclical recovery in industrial and automotive markets, which have not materialized yet. This is leading to higher uncertainty that the recovery may be delayed or muted." - Computer & Electronic Product Mfr'g

"While we still have a large order backlog, new orders are significantly below where we forecasted them to be this year. This will shorten lead times and should allow us to pick up additional orders next year." - Transportation Equipment Mfr'g

On to some notable earnings comments.

From McDonald's:

"Beginning last year, we warned of a more discriminating consumer, particularly among lower-income households and as this year progressed, those pressures have deepened and broadened. The QSR sector has meaningfully slowed in the majority of our markets and industry traffic has declined in major markets like the US, Australia, Canada and Germany. In several markets, we also continue to be negatively impacted by the war in the Middle East. These external pressures certainly weighed on our performance for the quarter, with declines in comparable sales globally and across each of our segments."

"but we're also seeing an impact with larger groups, particularly around families in Europe that we're seeing this as people are just looking to economize. You're also right that we're looking at a continued gap between food at home and food away from home inflation. The gap is about 3% right now or 300 basis point gap between the two. So you are seeing consumers being much more discretionary as they treat restaurants. You're seeing that the consumer is eating at home more often. You're seeing more deal seeking from the consumer. And you're seeing, I think, a trade down even within either units per transaction or within mix. All of those things for us are indicators that the consumer across a number of these markets is being very discriminating and I would point out consumer sentiment in most of our major markets remains low."

From ON Semiconductor whose revenue fell 7% sequentially and 17% y/o/y, but its stock rallied yesterday, and whose sales "decline was driven by an ongoing inventory correction in the automotive and industrial end markets, which together contributed 79% of our revenue":

"As we indicated in our Q1 call, we are seeing some stabilization in demand in our core markets. Inventory digestion persists with some pockets improving as customers maintain a cautious stance in 2024. We don't see a change to the L-shaped curve I talked about in Q1, but we expect parts of industrial such as energy infrastructure to recover in the 2nd half. Among the regions, Asia-Pacific, namely China is recovering, driven by both automotive and industrial."

They talked about their opportunities in the data center and AI market.

From Lattice Semiconductor, whose stock is down sharply pre-market:

"The inventory normalization and near term cyclical corrections continued as revenue declined 12% sequentially and 35% y/o/y."

"In Q2, we continue to undership to end customer demand as inventory normalization continues. On an end market basis, demand remained soft across industrial and automotive in Q2, with revenue down 23% sequentially as customers continue to reduce their inventory levels...Within communications and computing, Q2 revenue was flat sequentially. Strengths in data center networking and servers helped offset incremental weakness in wireless communications."

"As we discussed previously, we expect the inventory normalization cycle to continue through the 2nd half of this year."

Eagle Materials, a company that makes concrete, cement and wallboard, is mostly benefiting from government tax incentives and spending:

"Construction spending on infrastructure and heavy industrial projects continues to drive cement demand. In addition, despite some interest rate sensitivity, residential construction activity remains resilient, given chronic housing supply shortages and continued underlying demand strength."

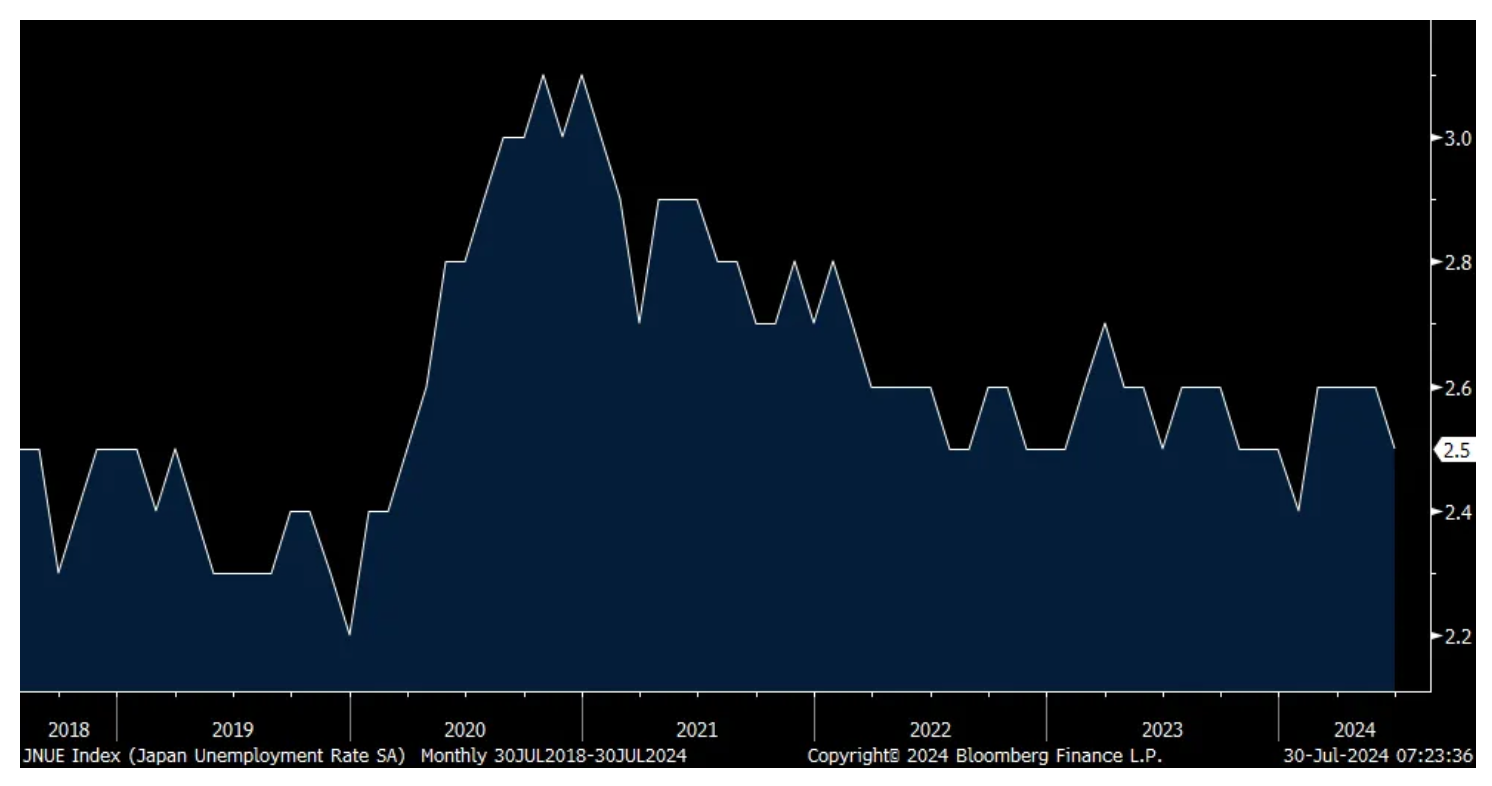

Ahead of the BoJ meeting tonight, the 10 yr JGB yield fell 2.3 bps to exactly 1.00% and the yen is weaker after Japan reported mixed jobs data. Their unemployment rate ticked down by one tenth to 2.5% and employment rose by 250k. On the other hand, the jobs to applicant ratio fell by one tenth to 1.23, the lowest since March 2022. It seems that with the BoJ, a cut in QE is a definite, likely to 5 trillion yen from 6 trillion and a jump ball on the rate hike but I expect a 10 bps increase, at least.

Japan's Unemployment Rate

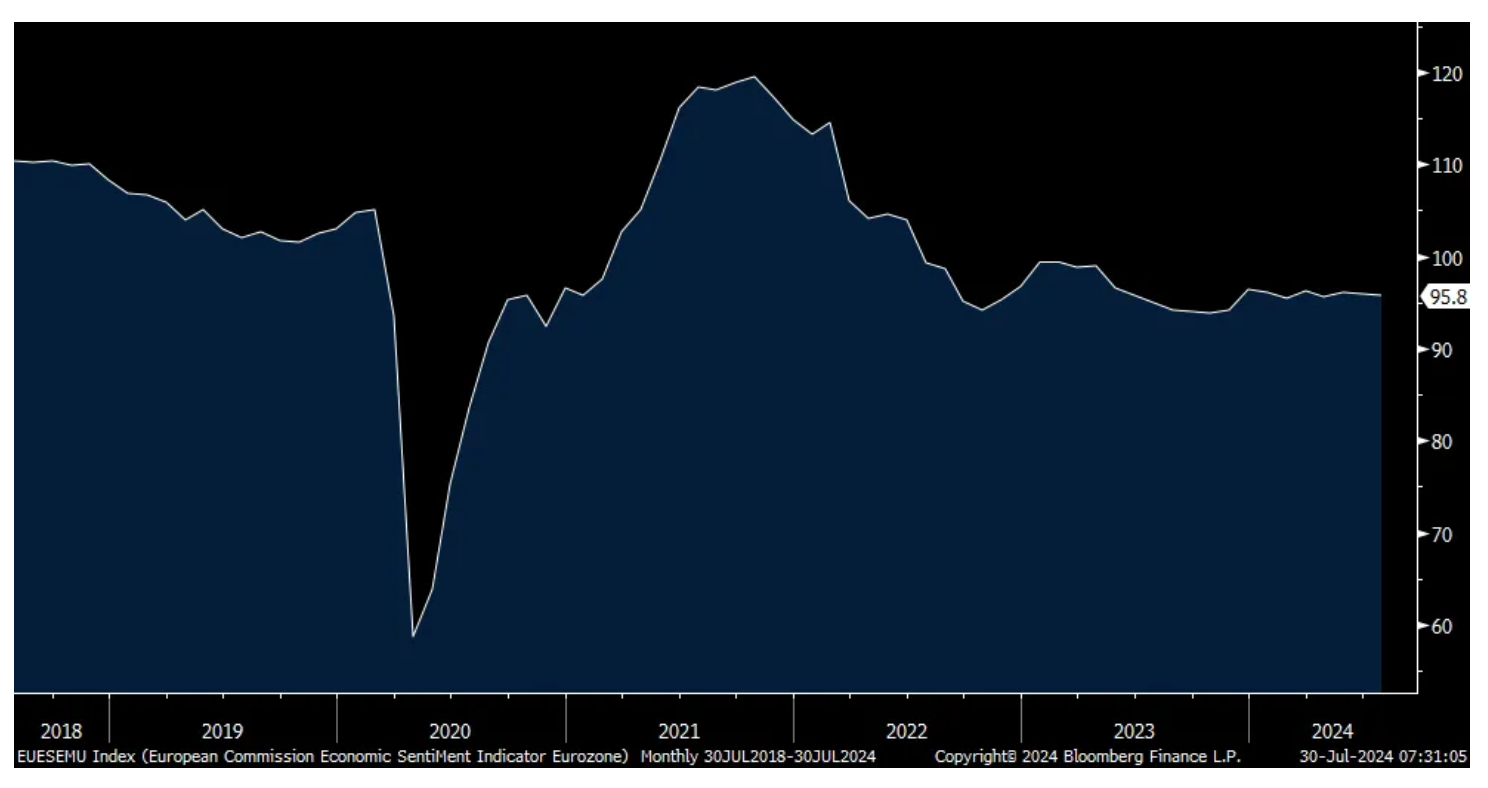

The Eurozone reported a better than expected Q2 economic performance with GDP up .3% q/o/q and .6% y/o/y, both one tenth above the forecast. Germany though continued with its weakness as its economy contracted by one tenth q/o/q vs the estimate of up one tenth. Spain has been the bright spot, helped by tourism, as its economy grew by .8% q/o/q, well above expectations of up .5%. The French economy grew by .3% q/o/q vs the estimate of .2%.

There was not much of a market response as the euro is little changed as are sovereign bond yields. Stocks though are higher. Helping to offset the upside in GDP, in terms of what this means for the ECB, Spain also reported a slower than expected gain in July CPI.

As for July Economic Confidence in the region, it continues to flat line.

Economic Confidence Index

BY Doug Kass · Jul 30, 2024, 9:49 AM EDT

I moved from very small PG to small - buying at $159.83 in premarket trading.

An investment and not a trade.

BY Doug Kass · Jul 30, 2024, 9:36 AM EDT

U.S. select premarket movers as of 8:46 a.m. ET:

-IMNN +246% (announces 11.1 Month Increase in Overall Survival in Patients with Newly Diagnosed, Advanced Ovarian Cancer Treated with IMNN-001)

-HLIT +20% (earnings, guidance)

-SFM +19% (earnings, guidance)

-FFIV +12% (earnings, guidance)

-TTOO +11% (earnings, guidance)

-VRNS +11% (earnings, guidance)

-PYPL +9.3% (earnings, guidance)

-AISP +7.8% (withdraws filing for stock offering)

-FBMS +7.7% (to be acquired by Renasant for $1.2B at implied transaction value of approximately $37.09/shr)

-TLRY +7.7% (earnings)

-BYON +7.4% (earnings)

-SWK +7.2% (earnings, guidance)

-LDOS +6.1% (earnings, guidance)

-VSTM +4.7% (receives US FDA Orphan Drug Designation for treatment of pancreatic cancer)

-ZBRA +4.6% (earnings, guidance)

-INCY +4.4% (earnings, guidance)

-VSTO +3.7% (Board Announces Review of Strategic Alternatives)

-HSAI +3.5% (announces Design Wins with Three Top Global Automakers JV Brands)

-ITW +3.5% (earnings, guidance)

-AMT +2.8% (earnings, guidance)

-QXO -81% (files mixed shelf of an indeterminate size)

-SMRT -23% (reports prelim Q2 revenue and suspends FY24 outlook; announces CEO transition)

-SYM -23% (earnings, guidance)

-EKSO -19% (earnings; files offering of an indeterminate size)

-LSCC -16% (earnings, guidance)

-WWD -13% (earnings, guidance)

-SKYX -9.8% (announces Collaboration with Home Depot for its Advanced and Smart Plug & Play Products for both Retail and Professional Segments)

-CLDX -9.5% (Barzolvolimab Phase 2 Study in Chronic Inducible Urticaria results)

-GLW -7.5% (earnings, guidance)

-AGCO -6.9% (earnings, guidance)

-RMBS -6.0% (earnings, guidance)

-AMKR -5.8% (earnings, guidance)

-PG -5.4% (earnings, guidance)

-SANM -4.7% (earnings, guidance)

-HOLX -4.6% (earnings, guidance)

-CRWD -4.0% (Delta said to seek compensation from Microsoft and Crowdstrike due to outage on July 19th)

-SBAC -3.7% (earnings, guidance)

-SAVA -3.1% (Ongoing open-label extension trials of simufilam in Alzheimer’s disease to be extended by up to an additional 36 months or until NDA has been reviewed by FDA)

-MRK -2.6% (earnings, guidance)

BY Doug Kass · Jul 30, 2024, 9:25 AM EDT

As of 8:24 a.m. ET:

BY Doug Kass · Jul 30, 2024, 9:15 AM EDT

As of 8:40 a.m.:

BY Doug Kass · Jul 30, 2024, 9:05 AM EDT

More on the weakening consumer from "Meet" Bret Jensen:

Bret Jensen/STAFF

1 minute ago

Dougie, I agree with your call on PG and consumer facing stocks having no pricing power as well as on housing. Seeing significant price cuts in my Zillow/Redfin feeds in recent months. In addition, the restaurants in Delray are having an increasingly rough time with a half dozen closing down since the first of the year. Friend of mine of one of my go to places here stated their restaurant had the slowest June on record based on sales tax receipts and they have been in same location for 22 years. Down by more than a third from last year. Caminos which is located in the 'pit' or epicenter on Atlantic is even suffering. The big joke for years if you pass Caminos and there is an actual seat at the bar, you are obligated to sit down and have at least one corona because usually it is two deep. I passed the place Sunday at 1pm. Not a single customer at the 24-seat bar. I did a double take and lingered for a few minutes to make sure they were not doing a photo shoot or something. Nope, just two confused bartenders as this is Twilight Zone like material. JMTC

BY Doug Kass · Jul 30, 2024, 9:00 AM EDT

BY Doug Kass · Jul 30, 2024, 8:45 AM EDT

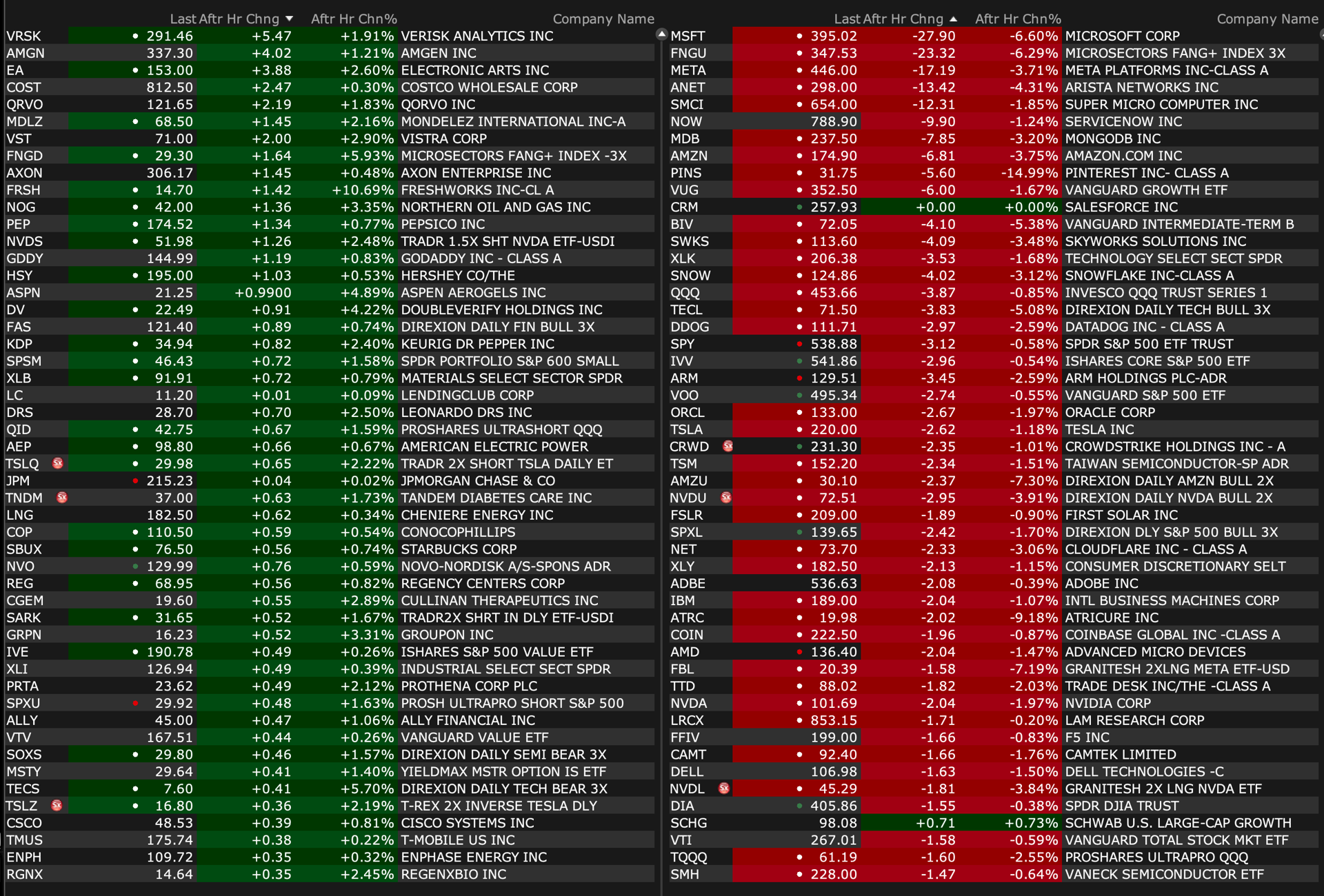

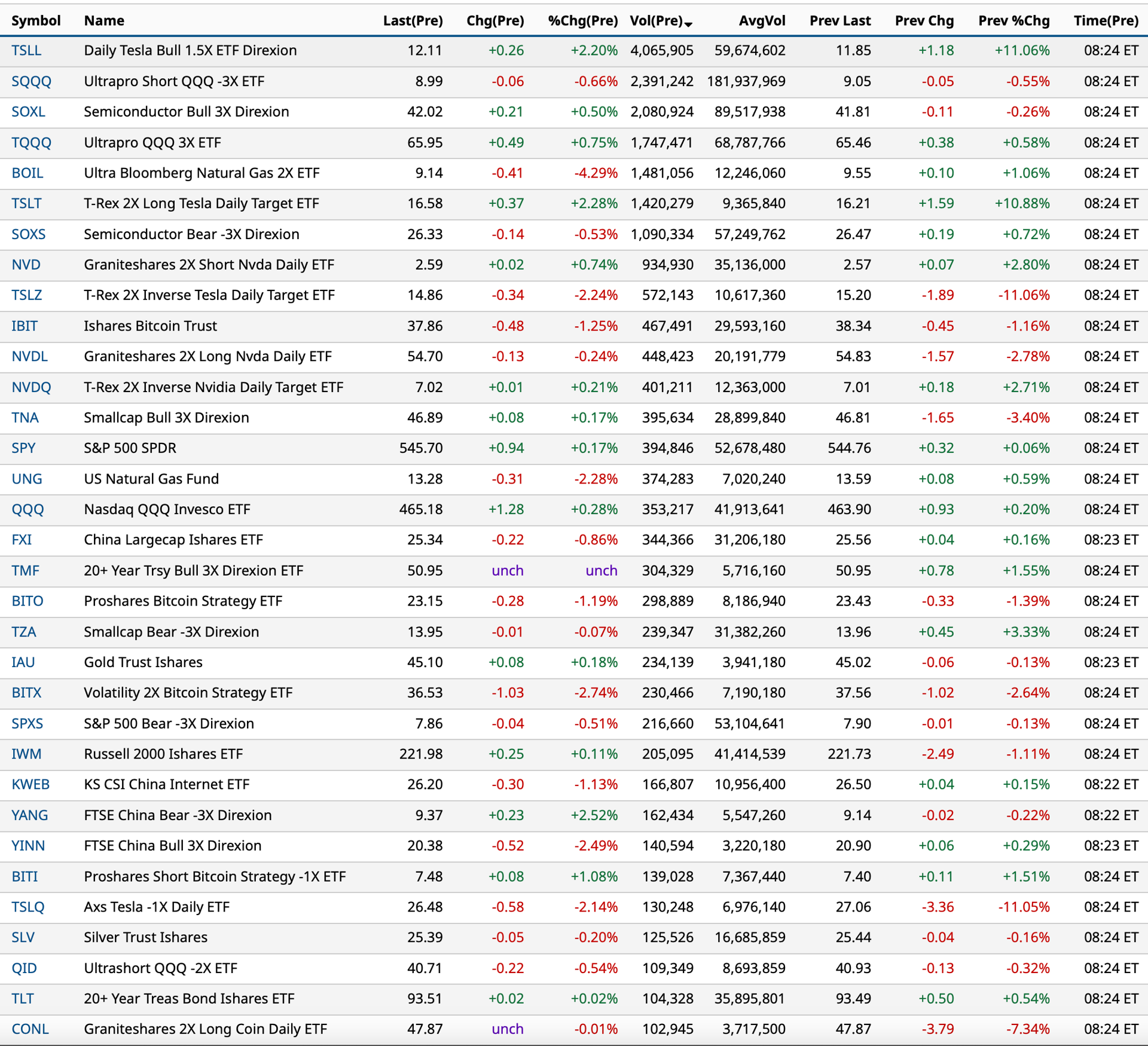

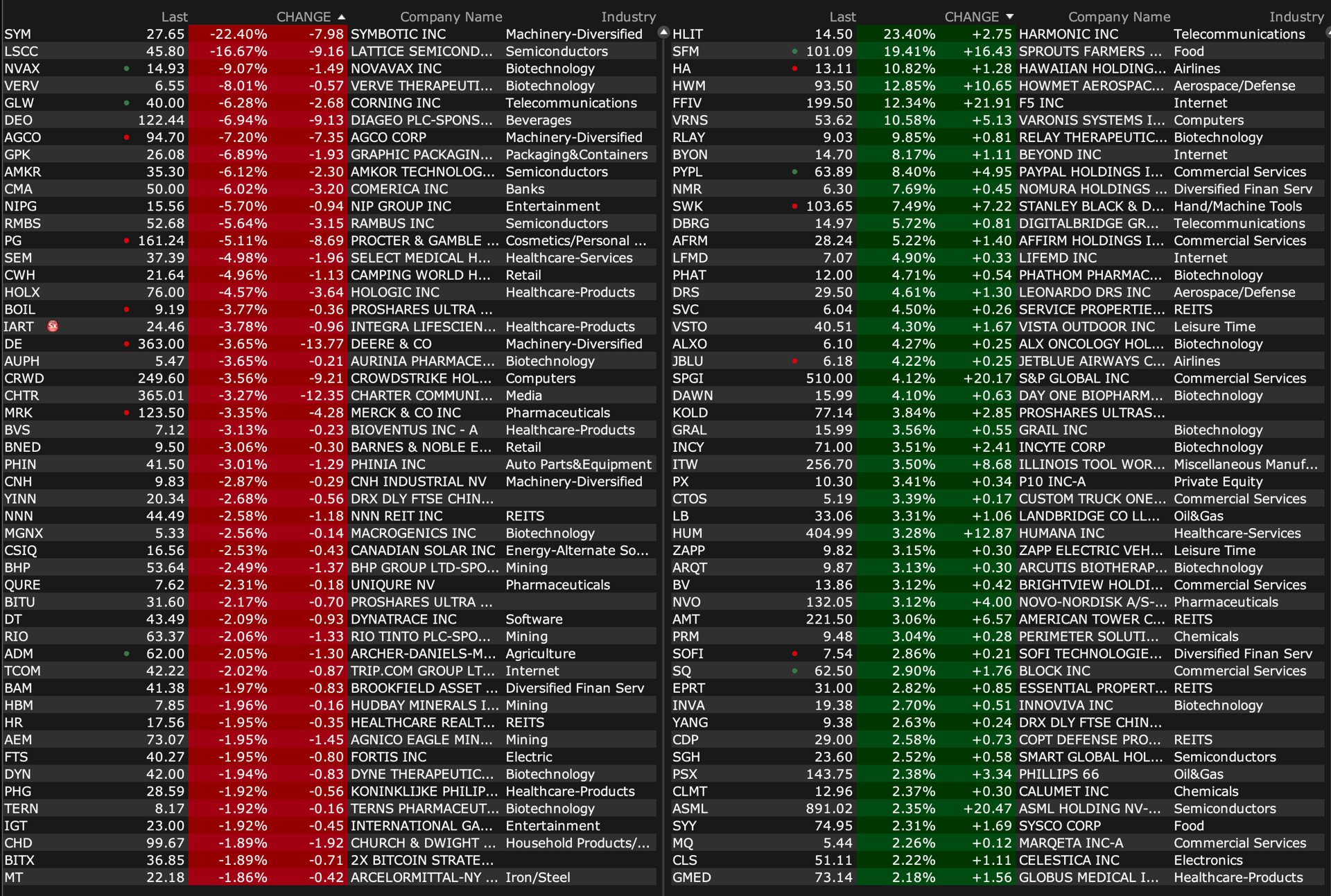

This table is a valuable resource for momentum-based short term traders:

BY Doug Kass · Jul 30, 2024, 8:31 AM EDT

From JPMorgan:

· US: Futs are higher but lacking the strength seen in EU mkts. Pre-mkt, Mag7 is mixed, and Semis are higher despite NVDA -63bps. MSFT is flat with earnings post-mkt. The yield curve is twisting steeper and 10Y yield is 1bps. USD is flat and cmdtys are lower across all 3 complexes. The macro data focus is on JOLTS and Consumer Confidence in what shapes up to be a quiet session ahead of BOJ and Fed releases tmrw; both could impact the yield curve though no large moves are expected. The bond market is pricing no moves tmrw for the Fed but is not pricing a small probability of a 50bps cut in Sept.

and...

EQUITY AND MACRO NARRATIVE: A rotation halted? Perhaps but it feels more like investors are being patient into a week that sees updates from most of the Mag7, a Fed meeting, and material updates on macro data including NFP/JOLTS and ISM-Mfg.

Reviewing the tactical scenarios from the July 22 Morning Briefing, where we looked at the combination of macro/earnings being stronger/weaker and the impact on the SPX; let’s take a look at where we are with both macro and earnings environments.

· MACRO – The macro environment remains one of above-trend growth with 24Q2 GDP numbers flagging that 24Q1 was a soft patch. Recent macro data, including Retail Sales, Industrial Production, and Flash PMIs seem to support this view. While GDP growth is slowing, it is unlikely to fall off a cliff which seems to be the view of the Bearish cohort of investors. Further, NFP is expected to hold up with consensus NFP forecasts of 159k for 24Q3, 132k for 24Q4, and 130k for FY25. I use NFP as a proxy instead of unemployment as that feels like a stronger measure of the labor market as the unemployment rate may be distorted given COVID and immigration patterns.

· EARNINGS – Entering earnings season, expectations were for revenues to grow ~4.5% and earnings to grow ~8.5%. With 41% of the SPX reporting, revenue growth is closer to 5% and earnings growth is closer to 10%, according to FactSet. Net profit margin is 12.1% vs. 11.8% 24Q1 and the five-year average is 11.5%. The notable sectors are Financials (15.0% EPS growth vs. 4.3% survey) and Energy (-80bps EPS growth vs. +13.3% survey). Overall, this is shaping up to be the best quarter since 21Q4, in terms of absolute growth.

o On a relative basis, earnings/revenue beats are below historical averages which may stem from the fact that we failed to see expectations fall significantly over the 30 days into earnings season, which we typically observe.

o 78% of companies are beating EPS vs. the ten-year average of 74%; EPS prints are surprising by 4.4% vs. 6.8% ten-year average. This is leading to smaller rewards for beats with stock prices seeing +0.3% reward for beats versus +1.0%, the five-year average (timing is from T-2 to T+2). Earnings misses are seeing 3.8% declines vs. 2.3% decline for the five-year average.

o 60% of companies are beating on revenues vs. 64% ten-year average; revenue beats are averaging 1.1% vs. 1.4% ten-year average.

BY Doug Kass · Jul 30, 2024, 8:15 AM EDT

* A constant refrain of ours...

Procter & Gamble PG (joining McDonald's MCD, Disney DIS, Pepsi PEP, Delta Airlines DAL, Starbucks SBUX and others) becomes the latest consumer-based company to suffer from demand elasticity concerns as top line slows relative to expectations.

Here is the press release:

P&G Announces Fourth Quarter and Fiscal Year 2024 Results | Procter & Gamble News (pg.com)

We purchased PG lower (around $160) on a similar miss awhile ago and I am considering adding after the shares initially fell by nearly -$4/share:

I added to weakness in JNJ , PG and MSOS. I lost some shares on expiration exercise - short calls.

Position: Long JNJ (M), PG (M), MSOS (L), Short MSOS calls (S)

BY DOUG KASSAPR 22, 2024 10:35 AM EDT

I continue to see consensus corporate profits expectations for 2024 and 2025 to be far too optimistic - elevated valuations seem unjustified.

BY Doug Kass · Jul 30, 2024, 7:55 AM EDT

Homebuilder equities have hit 52-week highs... while inventory is rising and home prices are weakening.

I have been steadily adding to my housing shorts.

From last week:

Trade of the Week: Short Homebuilders

This week I sold out of a multi-year long holding in Green Brick Partners GRBK and I began to short the shares of Toll Brothers TOL and D.R. Horton DHI .

Once again, this is a contrarian call.

Homebuilder stocks have been league leaders.

The bears on homebuilders over the last two years made the mistake of not realizing that the supply of existing homes would decline appreciably as interest (and mortgage) rates climbed — as basically fifteen years of zero interest rates allowed an opening to refinance at unprecedented low mortgage rates. Why upgrade your home, after all, with a 3% mortgage rate to replace it with a somewhat nicer home with a 7% mortgage rate.

The Movie May Now Be in Reverse

With rates slipping now, the lack of home affordability at record high levels, and employment rising — a squeezed consumer (suffering from high stacked or cumulative inflation since 2020) may result in a reversal in home pricing power and a rapid increase in inventory/supply may lie ahead. (See below)

Moreover a consequential drop in equities could also reverse the positive wealth effect that was a tailwind for home purchases (particularly the most expensive homes) over the last four years:

The change in mix was very pronounced in expensive markets that depend more on stock prices than on mortgage rates, where many high-end buyers — including those now riding the AI bubble — pay cash, often with funds either obtained from the sale of stocks, or borrowed against their stocks.

For example, the luxury market in the San Francisco Bay Area. Luxury is over $5 million. According to Compass’ luxury report for the San Francisco Bay Area:

“It is in the most affluent counties where high-tech industry is concentrated – and the centers of what is being described as the “AI boom” – that luxury home sales truly soared in Q2.”

San Francisco County and Santa Clara County (incl. San Jose) “saw year-over-year increases in $5-million+ home sales in Q2 2024 of 54% and 63% respectively.”

“The circle of seven extremely expensive communities circling Stanford University – on either side of the San Mateo/Santa Clara County line – saw a year-over-year Q2 increase of 92% in $10-million+ sales.”

“The most affluent households are typically much more affected by changes in stock markets – and in the Bay Area, by the soaring Nasdaq in particular – than by interest rates: Many of these buyers pay all-cash…. And, of course, many employees of companies such as Nvidia have suddenly become very wealthy indeed.”

To the homebuilder bulls the stocks remain cheap – after all P/E ratios are nearly half that of the S&P Index. But this is always the case for the sector (and for cyclicals in general) – the valuations always appear to look inexpensive (e.g., DHI trades with a price/earnings ratio of only 12x) at the top! (We look to CNBC for the consensus, here a panelist advances the conventional notion that homebuilders are cheap Trade Tracker: Stephanie Link buys more D.R. Horton and Seagate and sells CDW (cnbc.com) because of the conventional view that interest rates will drop!)

As noted in Wolf Street's analysis: Here Comes the Inventory of Vacant Homes: With Buyers on Strike despite Lower Mortgage Rates, Supply Spikes to Highest in 4 Years. Sales Drop Further except at High End | Wolf Street

Mortgage rates have dropped to about 6.8%, down by a full percentage point from October last year, and yet sales of existing homes have plunged, and vacant homes for sale are coming out of the woodwork, the same vacant homes that the industry said didn’t exist, the second and third homes that people had moved out of but didn’t sell when they bought a new home over the past few years in order to ride the price spike all the way to the top. So now it’s time to sell those vacant homes. And supply in June spiked to the highest level in four years.

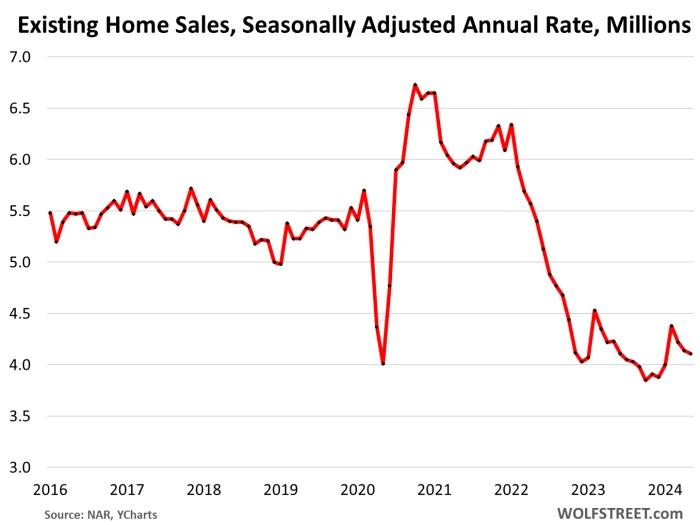

Sales of existing homes of all types – single-family houses, townhomes, condos, and co-ops – fell 5.4% in June from May on a seasonally adjusted basis, and also by 5.4% year-over-year to an annual rate of 3.89 million homes, the third-lowest sales volume since the depth of the Housing Bust in 2010, behind only October and December 2023, according to the National Association of Realtors (NAR) today.

“We’re seeing a slow shift from a seller’s market to a buyer’s market. Homes are sitting on the market a bit longer, and sellers are receiving fewer offers. More buyers are insisting on home inspections and appraisals, and inventory is definitively rising on a national basis,” the NAR said in its report (historic data via YCharts):

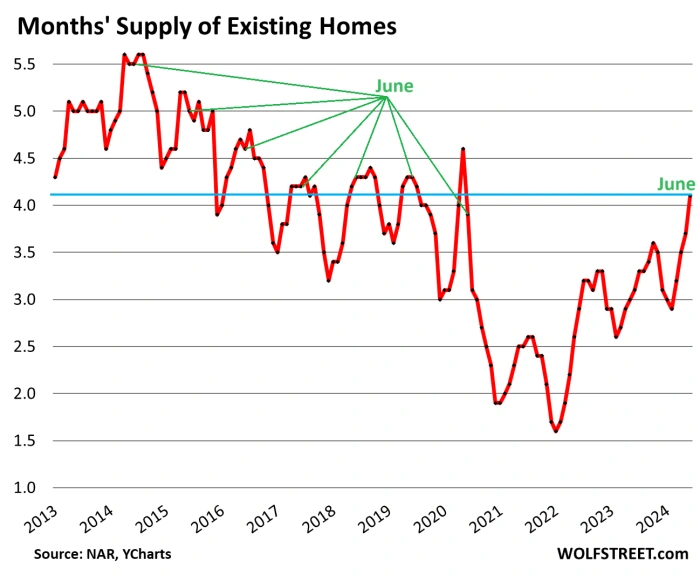

Supply spiked to 4.1 months in June at the current rate of sales, the highest since May 2020, and just a hair below the Junes in 2019 (4.3 months), 2018 (4.2 months), and 2017 (4.2 months).

Inventory for sale jumped by 23.4% year-over-year, to 1.32 million homes, according to NAR data. At the same time, sales dropped 5.4% year-over-year. This surge in inventory combined with the drop in sales caused supply to spike by one-third year-over-year, to 4.1 months in June, from 3.1 months in June last year.

And normally, supply remains roughly stable or declines from May to June, but not this June. This June it spiked. There is a game-changer underway (historic data via YCharts):

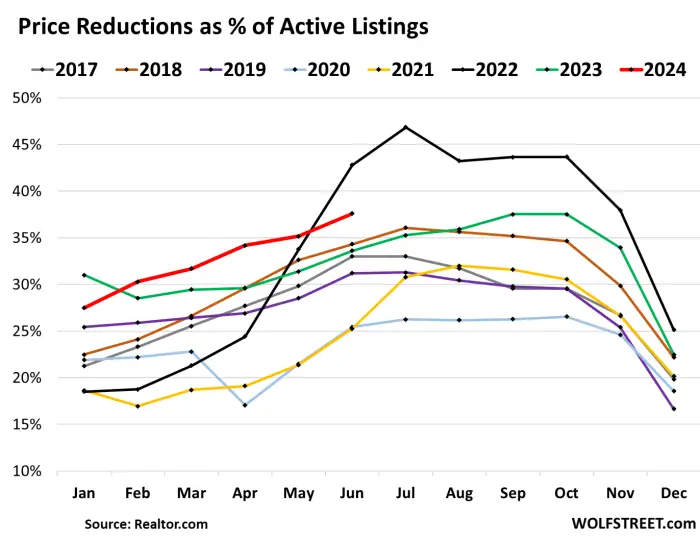

Price reductions continued to surge. Of the active listings, 37.6% had reduced prices in June, the highest share of reduced prices for any June, except June 2022, in the data from Realtor.com going back to 2016:

BY Doug Kass · Jul 30, 2024, 7:33 AM EDT

BY Doug Kass · Jul 30, 2024, 7:15 AM EDT

“The one thing I’ve learned about markets over time is that they tend to train you to ignore something and then humiliate you once you figure it doesn’t matter.”

- Stanley Druckenmiller

Bonus — Here are some great links:

BY Doug Kass · Jul 30, 2024, 7:05 AM EDT

Wolf Street howls about an ill-fated share buyback.

BY Doug Kass · Jul 30, 2024, 6:50 AM EDT

BY Doug Kass · Jul 30, 2024, 6:31 AM EDT

The S&P Short Range Oscillator has dropped from 2.23% to 1.39%.

BY Doug Kass · Jul 30, 2024, 6:21 AM EDT

BY Doug Kass · Jul 30, 2024, 5:45 AM EDT