'Super Weird'

Another good observation from Jason:

Thanks for reading my Diary today.

Enjoy the evening.

Be safe.

BY Doug Kass · Feb 22, 2024, 5:38 PM EST

Another good observation from Jason:

Thanks for reading my Diary today.

Enjoy the evening.

Be safe.

BY Doug Kass · Feb 22, 2024, 5:38 PM EST

BY Doug Kass · Feb 22, 2024, 4:25 PM EST

BY Doug Kass · Feb 22, 2024, 4:21 PM EST

* Based on breadth... and stocks whose earnings were weak and stayed down in price

To keep euphoria in check - see breadth and earnings stocks that opened down are staying down

No real reversals on those that gapped down on earnings - most sticking to mid to low end of their day range

BY Doug Kass · Feb 22, 2024, 3:40 PM EST

15:15 (US) Fed's Harker (non-voter): Greatest risk would be cutting rates too soon

- Financial market liquidity remains abundant

- Concerned by rise in credit related delinquencies

- The recent CPI data shows uneven progress of lowering inflation

- Still wants more confidence inflation is moving back to 2%

- Support slowing before halting balance sheet contraction

- Multiple signs the labor market is coming into better balance

- US GDP continues to be strong

- Rise in layoffs is not a sign of recession arriving

- Disinflation trend has picked up, the Fed is in the last mile of heading to 2% inflation

- Consumer spending remains strong

BY Doug Kass · Feb 22, 2024, 3:25 PM EST

Investment short FMC traded down to a fresh low today and I reduced my short position.

Short FMC (VS)

BY Doug Kass · Feb 22, 2024, 3:05 PM EST

Equities have decoupled from bonds, nonetheless:

* The yield on the 2 year Treasury note is +6 bps to 4.714%.

* The yield on the 10 year Treasury note is unchanged at 4.37%.

* The yield on the long bond is -3 bps to 4.465%

BY Doug Kass · Feb 22, 2024, 2:55 PM EST

I have reduced GS and MS longs at $390.87 and $86.01, respectively, to tagends.

I covered my AXP short for a loss.

BY Doug Kass · Feb 22, 2024, 2:45 PM EST

I have covered my ROKU short at $63.15 for a handsome gain.

BY Doug Kass · Feb 22, 2024, 2:32 PM EST

I am selling the balance of my OXY calls for a profit.

And I have reduced my OXY long from large to medium-sized.

I plan to be a buyer on any weakness.

BY Doug Kass · Feb 22, 2024, 2:20 PM EST

From Charlie:

BY Doug Kass · Feb 22, 2024, 2:12 PM EST

I am further reducing Green Brick Partners GRBK long.

BY Doug Kass · Feb 22, 2024, 2:00 PM EST

Reducing XOM and CVX to very small after the recent run up.

BY Doug Kass · Feb 22, 2024, 1:05 PM EST

Reducing more shorts - MPW, WBA and WOOF.

Reducing ELAN and FRPT longs.

BY Doug Kass · Feb 22, 2024, 12:56 PM EST

Reducing further shorts in FIGS and XPOF.

BY Doug Kass · Feb 22, 2024, 12:45 PM EST

BY Doug Kass · Feb 22, 2024, 12:00 PM EST

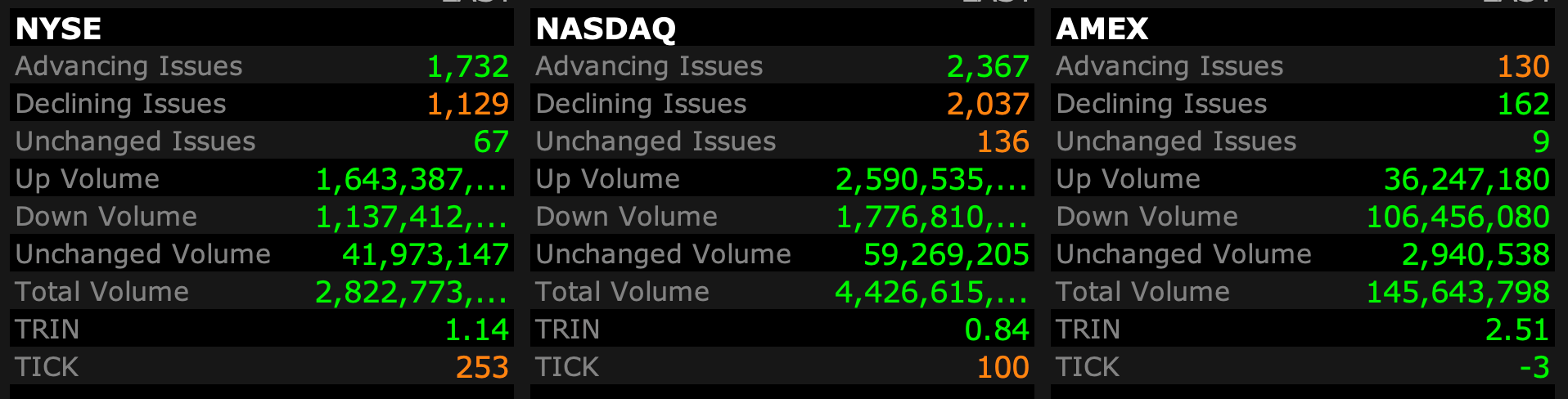

Earlier I referenced weak market breadth.

Here is another manifestation of the narrowing leadership:

BY Doug Kass · Feb 22, 2024, 11:58 AM EST

From Peter:

I’ll start with this quote from Fed Vice Chair Philip Jefferson that points to a committee that wants to cut rates this year but not anytime soon. “We always need to keep in mind the danger of easing too much in response to improvements in the inflation picture. Excessive easing can lead to a stalling or reversal in progress in restoring price stability.”

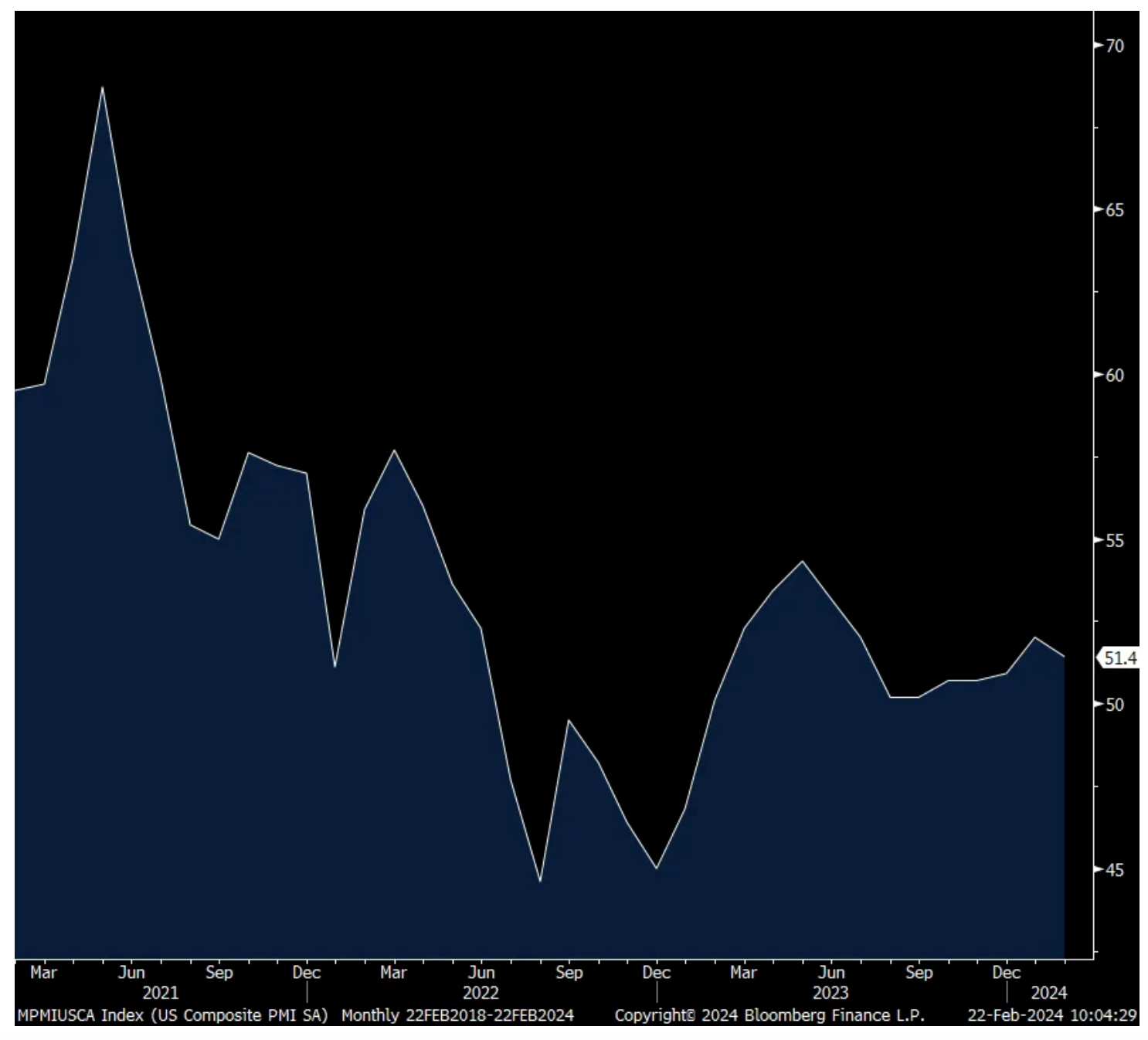

The February S&P Global manufacturing and services PMI fell to 51.4 from 52. Manufacturing actually improved a touch to 51.5 from 50.7 but was offset by a 1.2 pt m/o/m decline in services to 51.3.

With regards to the lift in manufacturing, “Although only modest, the expansion was supported by a return to output growth and quicker increases in new orders and employment. Easing pressure on supply chains led to a renewed improvement in vendor performance during February, with shortened lead times for inputs enabling firms to process incoming new work in a more timely manner.”

Thus, no real impact yet from the Red Sea travel diversions that has extended time of delivery but S&P Global is citing better February weather from the rougher January as a reason too for the improvement. Also, and what we’ve been watching closely for, “Optimism in the outlook led firms to build stocks of purchases and finished goods, as both returned to growth in February, with firms indicating the first expansion in pre-production inventories since August 2022.” Selling prices were little changed m/o/m.

In services, new orders fell to a 3 month low and backlogs were down too. The employment component eased as well and “Services firms highlighted caution with regards to hiring due to cost concerns and softer new order growth.” Selling prices were higher.

Bottom line, S&P Global equates the figures above to an annualized GDP growth rate of 2%. Treasury yields fell to 4.30% after the slight miss but has since bounced back to 4.32%, about where it was right before the release. Maybe the Jefferson comments was a factor too in the lift.

US PMI

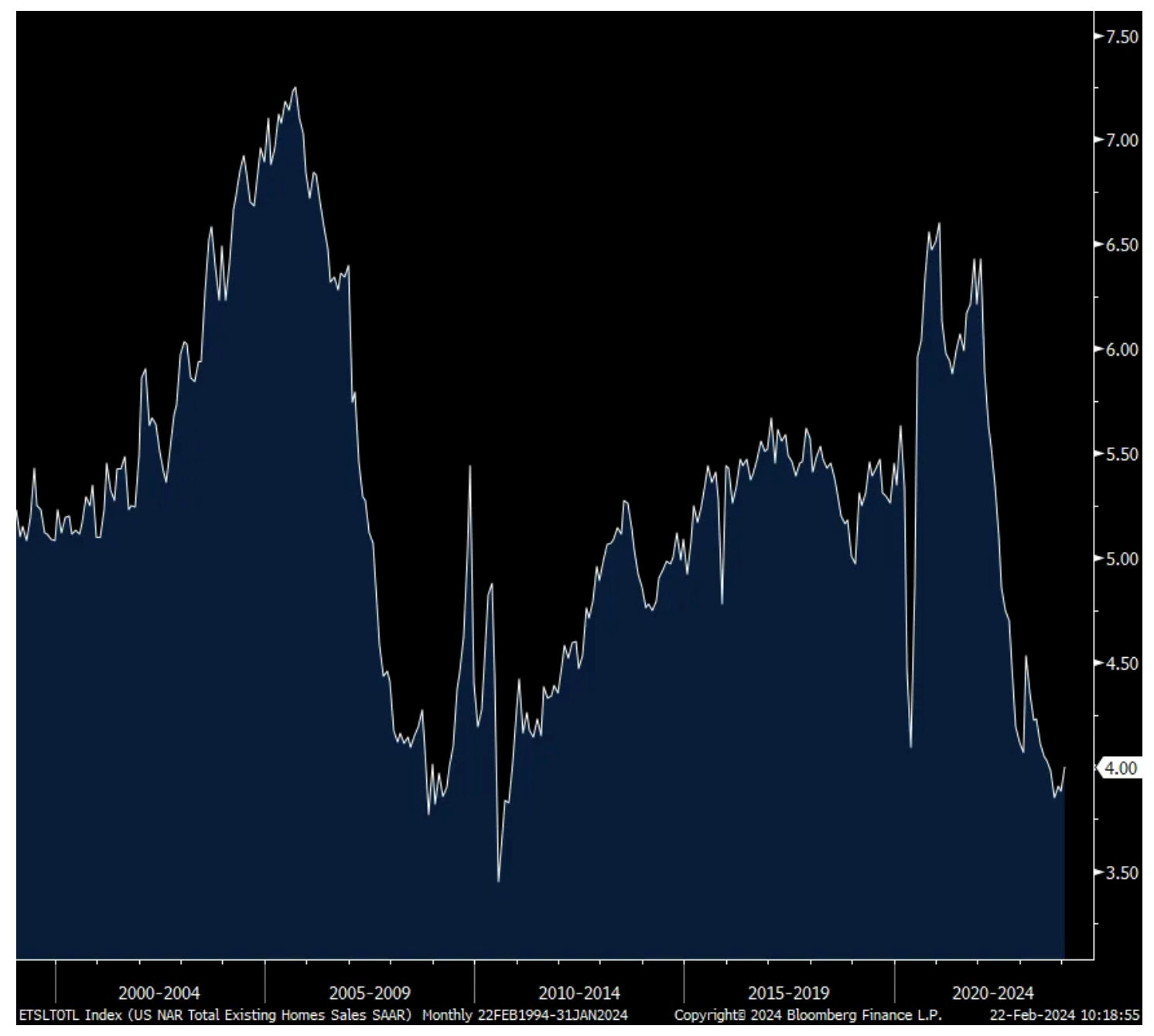

Existing home sales in January, thus likely capturing most contracts signed in the September, October, November timeframe, totaled exactly 4mm which is about in line with expectations and about the same as the final 2023 number and up from December’s print of 3.88mm (revised up by 100k).

Seasonally, the number of homes for sale is muted this time of year before picking up in the spring and months’ supply fell to 3 from 3.1 in December and compares with 2.9 in January 2023 and 3.1 in January 2020. The median home price rose 5.1% y/o/y and continues to put a squeeze on the first time home buyer who made up just 28% of purchases, getting boxed out by all cash buyers who totaled 32% of purchases from 29% last month.

Bottom line, assuming many contracts in this figure were signed in late Q3 into Q4, it was during this period that mortgage rates rose above 8%. But when closings occurred in January, that rate got back below 7% and now in the 3rd week of February it stands at 7.28% according to Bankrate. It’s tough to know however who had rate locks and who didn’t and when.

Either way, overall, we’re talking about the pace of existing home sales that are hovering the lowest levels in 2009-2010 as affordability challenges for first time homebuyers is acute.

Existing Home Sales

BY Doug Kass · Feb 22, 2024, 11:25 AM EST

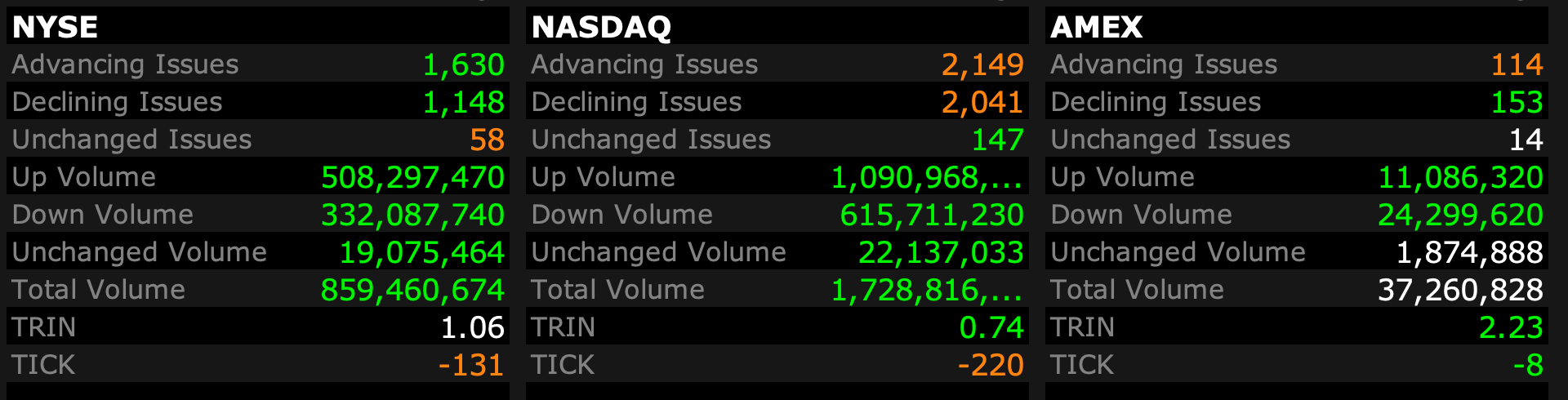

Despite the market fireworks, breadth remains narrow:

In tomorrow's opener I will explain why I don't see a broadening out of breadth and an expansion in market leadership - despite The Tattooed Lady's robust results last night.

Hint: The shares in the non MAG 7 market will not likely detach from:

* Higher (interest rates) for longer

* Weakening global economic growth

* A widening in the gap between the S&P dividend yield and short dated Treasuries

* A deterioration in the equity risk premium to multi decade lows

BY Doug Kass · Feb 22, 2024, 11:05 AM EST

From Peter:

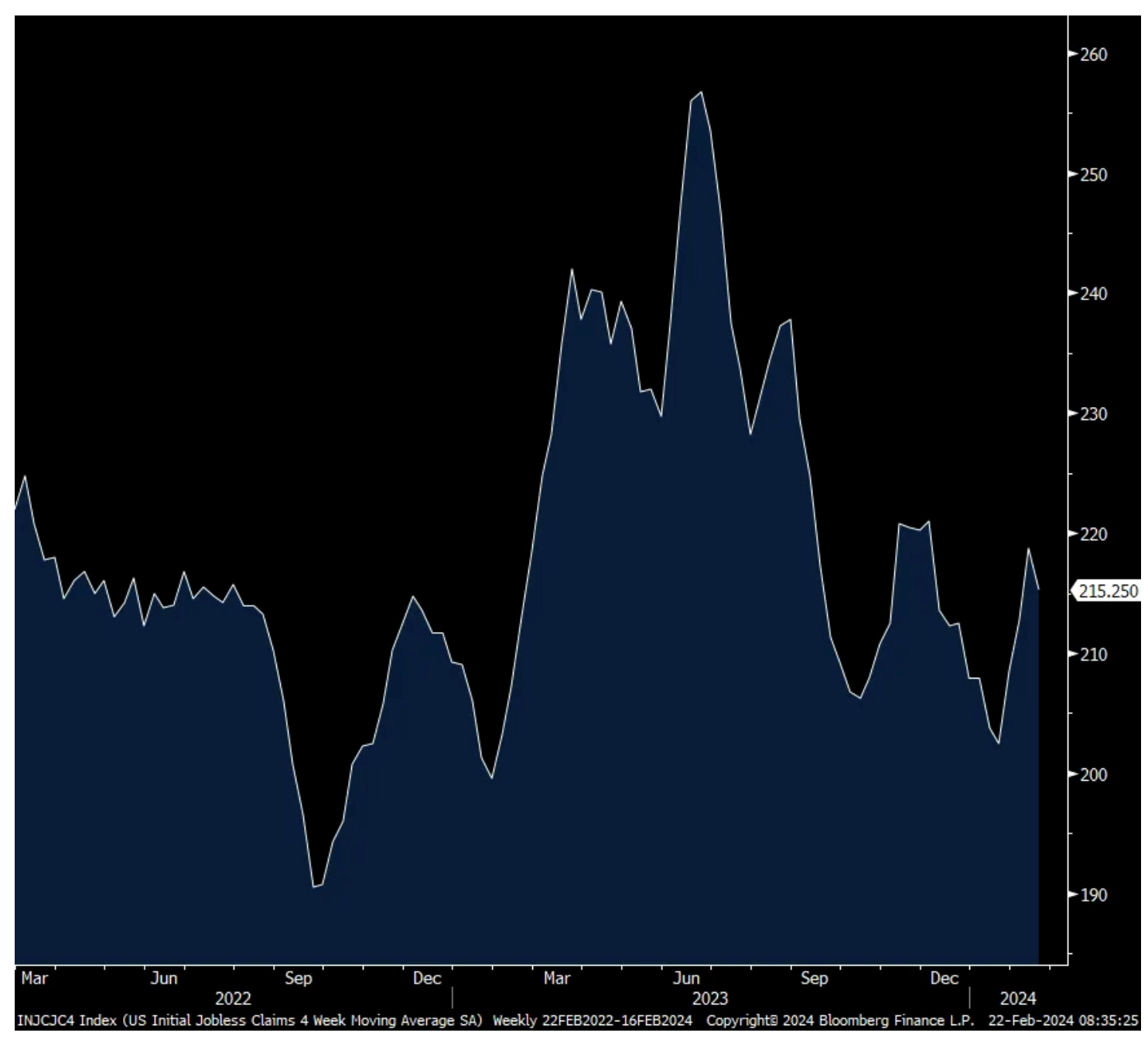

Initial jobless claims fell to 201k from 213k and that was 15k less than expected but because it was President’s Day Weekend, I’ll always wait for the week after a holiday influenced print for a better tell. Smoothing this out, the 4 week average fell to 215k from 219k. Continuing claims fell by 27k to 1.862mm after rising by a like amount in the week before.

As stated, it was a holiday influenced figure but either way, the number of people filing for claims remains muted while those remaining on benefits is still elevated.

In response to the lower than expected claims print, the 10 yr yield is at the highest level since late November at 4.34%. The 2 yr yield is at 4.70%, the highest since mid December.

Initial Claims 4 week average

Continuing Claims

BY Doug Kass · Feb 22, 2024, 10:45 AM EST

St. Joe's EPS results, reported last night, were uninspiring.

Given the recent interest rate rise I have been reluctant to buy back the shares after having sold most of my position in late January:

At $58 I have reduced St Joe back to small-sized.

Position: Long JOE (S)

That said, JOE remains an attractive long term holding.

More on my analysis of the quarter early next week...

BY Doug Kass · Feb 22, 2024, 10:30 AM EST

From Peter:

Back in the day when Apple's revenue and earnings growth rate was stellar and its stock dominated I referred to it as its own asset class. We had stocks, bonds, commodities, currencies and Apple. Nvidia has now certainly taken that mantle, especially with its 77% gross margins, rarefied air.

That said, it does seem that the earnings beat and guide up are closer to market expectations than what we've seen over the past year. Also, that gross margin will eventually get competed away but not anytime soon it seems.

The Bull/Bear spread in the Investors Intelligence survey remained extreme with a more than 40 point differential. While Bulls slipped by 1.5 pts to 57.3, Bears were down by a like amount to just 16.2. AAII today said Bulls rose 2.1 pts to 44.3 while Bears fell a touch to 26.2.

These surveys follow the near Euphoria in the Citi Panic/Euphoria index and the 11 yr high in the Market Vane Bullish Consensus. The CNN Fear/Greed index closed yesterday at 74 vs 79 one week ago but assume it jumps at least this morning.

Bottom line, the market mood is pretty excited so from a contrarian standpoint be aware.

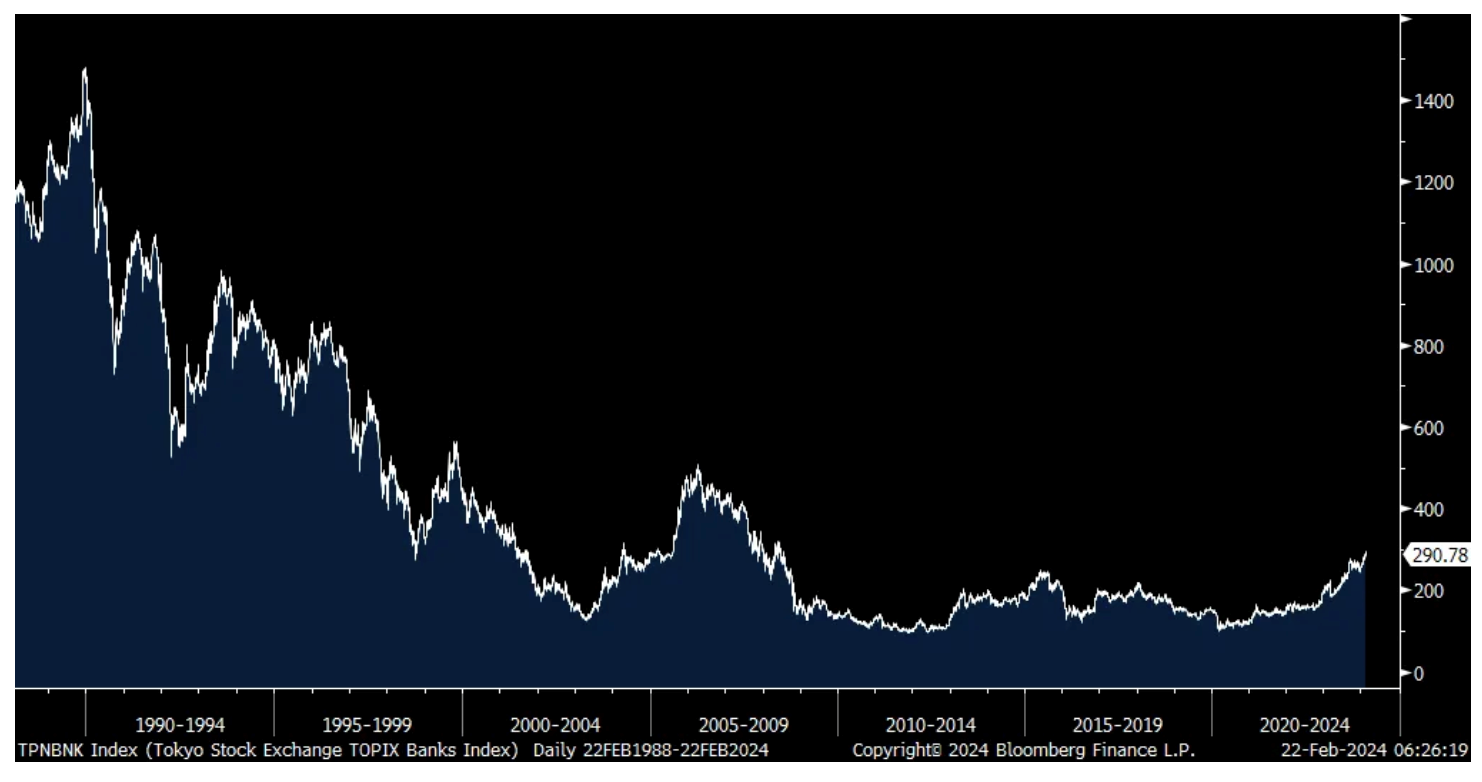

They finally did it. The Nikkei 225 index finally exceeded its last day of trade close in 1989! Finally, and we remain bullish and long. Amazingly though, the TOPIX Bank Stock index remains 80% below its 1989 peak thanks to the BoJ destroying the business model and profits of banks with what they did to the yield curve, aka, flattened it. We remain long Sumitomo Mitsui Financial.

Of note too, it seems again that BoJ Governor Kazuo Ueda is setting us up for the end of NIRP. He said in parliament today, "I expect that a virtuous economic cycle in which inflation rises gradually with an increase in wages and employment will strengthen. Signs have been observed that businesses are becoming more active when deciding wages as labor demand tightens." Notwithstanding these comments, the 10 yr JGB yield was little changed as is the yen.

Nikkei 225

TOPIX Bank Stock Index

Many global February PMI's are out today. In the face of stock market highs, Japan's composite index fell to 50.3 from 51.5 as manufacturing fell to 47.2 from 48 and thus remains below 50 while services were down slightly to 52.5 from 53.1. S&P Global said, "The Japanese private sector economy saw the slight improvement at the start of the year all but evaporate during February, as business activity broadly stagnated" and "Firms were also the least upbeat since January 2023, reflecting reduced optimism with regards to future output."

And remember, Q3 and Q4 saw GDP declines in Japan. Luckily many Japanese companies that trade on the Nikkei are global multinationals.

Australia's PMI was mixed as manufacturing fell back below 50 at 47.7 but offset by a 3.7 pt rise in services to back above 50 at 52.8. India remains a place of broad economic strength with manufacturing at 56.7 and services at 62, both up .2 pts m/o/m. We are still very bullish on India's economic outlook and its markets.

The economic situation in the Eurozone was pretty mixed in February. Manufacturing continued with its weakness at 46.1, down .5 pt with Germany in particular very weak at just 42.3. French manufacturing is still below 50 but less so at 46.8 vs 43.1 in January. The services side saw exactly a 50 print for the region from 48.4 but German and French services were below 50.

The positive in the report was this, "Business confidence about the year ahead improved, hitting a 10 month high and encouraging firms to raise staffing levels at a pace not seen since last July, adding to signs that the Eurozone's downturn is moderating." Also helping was expectations for interest rate cuts.

Stagflation remains in the region as S&P Global said "Growth of average input costs across producers of goods and providers of services accelerated for a 2nd successive month to reach the highest since last May." Also, "Selling price inflation likewise accelerated, up for a 4th month running in February to also hit the highest since last May.

Excluding the price surge seen over the last two years to last May, February's rate of inflation was the highest recorded since January 2018 and well above the survey's pre-pandemic long run average." This was mostly driven by higher service prices which saw the highest price level since September 2000 not including Covid.

Bottom line, stagflation and a tough spot for the ECB. European bond yields are down slightly while stocks are rising again.

The UK PMI rose .4 pts m/o/m to 53.3, though the internals were little changed with manufacturing at 47.1 and services remaining at 54.3. Service price inflation remains an issue as "Inflationary pressures remained elevated during the latest survey period. Moreover, the rate of input price inflation edged up to its strongest since August 2023, largely due to rising salaries in the service sector." Manufacturing saw only a modest rise in input prices "despite higher shipping costs and worsening supply chain disruptions in the wake of the Red Sea crisis."

Moving to earnings, some conferences and I'll leave Nvidia to others.

From Analog Devices, a more industrial focused semi producer:

"As we previously discussed, the inventory rationalization at our customers that began during the middle of 2023 is expected to continue through our 2nd quarter. Encouragingly, first quarter bookings improved sequentially, growing our confidence that inventory related headwinds will largely subside this quarter. That said, the macro situation remains challenging and the shape and timing of a 2nd half recovery will be governed by underlying demand."

That said, an analyst pointed out that this is the worst revenue drawdown for this company since 2001 and 2009, highlighting how harsh the inventory correction has been.

Highlighting the part of the US economy benefiting from government largess and the rest of the economy that is not, Regions Financial presented at the BoA financial conference and said this:

"Most of our clients are facing this year with a lot of caution. I see them building liquidity, using excess liquidity, if there is such a thing, to pay down debt and, waiting on the next event, where really the trigger would be around interest rate reductions. So we see that cautionary approach by our operating companies. But we also see strength in our client base coming out of those entities that are close to infrastructure improvements and that would be roads, bridges, even colleges, water sewer type construction companies and those that are in the line of supplying those kind of materials."

Toll Brothers is very bullish on its business:

After a good quarter, "since the start of the spring selling season in mid January, we have seen a meaningful uptick in demand that has continued through this past weekend."

"From a geographic standpoint, demand was broadly distributed across our footprint. We saw particular strength in our Pacific region, including all of California and Seattle and also in Las Vegas, all of Texas, Denver, and from Atlanta up through Boston. Demand was solid across all product types as well with affordable luxury accounting for 45% of our units and 34% of dollars, luxury 36% and 49%, and active adult 19% and 17%."

They are certainly catering to a higher income consumer and "The vast majority of our customers can qualify for a market rate mortgage without a buydown, and they prefer to use any incentive offered on design studio upgrades or to reduce their closing costs."

Also of note and to the higher end customer, "consistent with the past several quarters, approximately 25% of our buyers paid all cash in the first quarter, and the LTVs for buyers who took at mortgage dropped to approximately 67%, 200 bps lower than our average over the prior four quarters."

The one risk for Toll Brothers, "During the quarter, we once again benefited from our strategy of increasing our supply of spec homes, which represented approximately 50% of orders and 40% of deliveries in the first quarter."

From Mister Car Wash, a stock we own and the largest car wash operator in the country:

"We are not anticipating any changes in the macro environment. Many consumers remain challenged."

Royal Caribbean, benefiting in part from the retiring Baby Boomers, just weeks after reporting its earnings said "Since our last earnings call, robust demand for our vacation experiences has significantly exceeded our initial expectations."

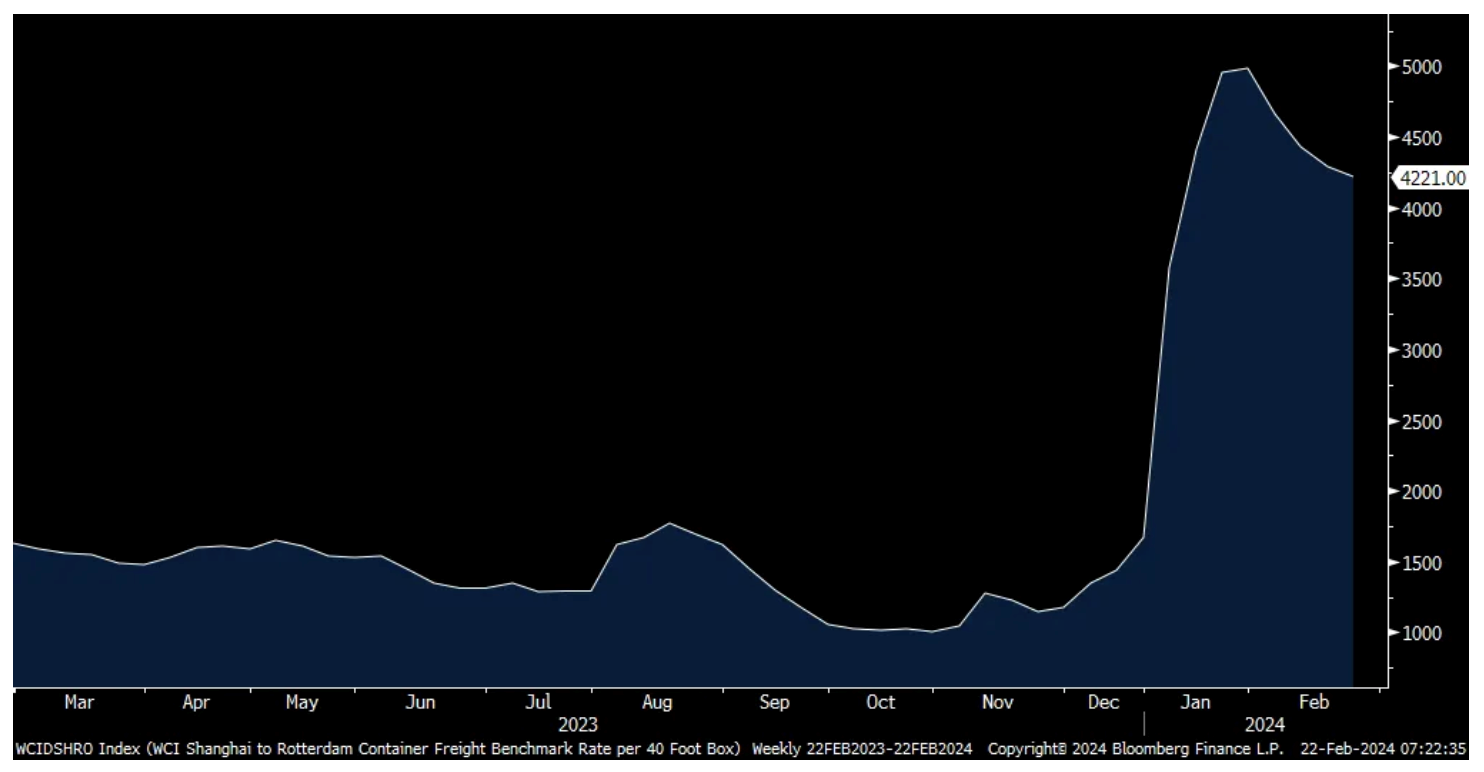

Let's end by updating container shipping pricing. The WCI Shanghai to Rotterdam route for a 40 ft container fell slightly, by $67 to $4,221 which compares with $1,667 at the start of the year. The Shanghai to LA trip fell by $71 w/o/w to $4,683 vs $2,100 in the last week of December.

Shanghai to Rotterdam

BY Doug Kass · Feb 22, 2024, 10:15 AM EST

I have taken trading short rentals in SPY and QQQ at $504.99 and $435.25, respectively.

Also shorted small Index calls for March.

BY Doug Kass · Feb 22, 2024, 10:06 AM EST

As noted last week I have no short positions in SPY and QQQ.

But I plan to...

BY Doug Kass · Feb 22, 2024, 9:54 AM EST

BY Doug Kass · Feb 22, 2024, 9:34 AM EST

Upside

-BZFD +101% (announces sale of Complex to NTWRK in $108.6M all-cash deal; to cut 16% of remaining workforce)

-RELY +24% (earnings, guidance)

-ROOT +24% (Cantor Fitzgerald Raised ROOT to Overweight from Neutral, price target: $13)

-OCUL +21% (expanded team anticipated to accelerate momentum in AXPAXLI Phase 3 Wet AMD Programs; places 32.4M shares and 10.8M warrants at $7.52/shr in $325M private placement)

-OLO +19% (earnings, guidance)

-RILY +15% (Board of Directors issues statement regarding internal review)

-NVDA +13% (earnings, guidance)

-ACVA +11% (earnings, guidance; announces the settlement of litigation regarding AutoIMS)

-SMCI +11% (files to sell offering of $1.5B of Convertible Senior Notes due 2029)

-ERF +9.7% (Chord Energy and Enerplus to combine in $11B transaction creating premier Williston-focused E&P company; reports earnings, increases dividend)

-CNNE +8.7% (Board authorized the repurchase for cash of $200 Million of the Company's common stock through a modified "Dutch Auction" tender offer; reports earnings)

-WES +8.6% (earnings)

-LNTH +7.6% (earnings, guidance)

-BIGC +7.5% (earnings, guidance)

-OUT +7.5% (earnings)

-BROS +6.3% (earnings, guidance)

-W +6.3% (earnings, guidance)

-RCL +6.1% (raises FY24 guidance)

-MRNA +5.9% (earnings, guidance)

-BLDR +5.4% (earnings, guidance; increases share buyback program)

-CLPT +5.2% (announces FDA Clearance and First-in-Human Cases Performed with the New 2.2 Software Version and the Integrated Maestro Brain)

-DASH +4.6% (Morgan Stanley Raised DASH to Overweight from Equal Weight, price target: $145)

-NGVT +4.5% (earnings, guidance)

-SNPS +4.5% (earnings, guidance)

-PWR +3.7% (earnings, guidance)

-TNHPF +3.5% (earnings, guidance)

-NVRO +3.5% (enters into Cooperation Agreement with Engaged Capital; appoints Kirt P. Karros to Board, effective immediately)

-PEBPP +3.2% (earnings, guidance; files mixed shelf of indeterminate amount)

-COTY +2.9% (TD Cowen Raised COTY to Outperform from Market Perform, price target: $16)

-VIV +2.8% (earnings, guidance)

-AMLX +2.6% (earnings)

-IONQ +2.5% (achieves first known commercial demonstration of ion-photon entanglement, a key technical milestone for networking quantum computers)

-MOS +2.1% (earnings, guidance)

Downside

-RIVN -17% (earnings, guidance)

-GSHD -16% (earnings, guidance; current COO Mark Miller named as new CEO, effective Jul 1st)

-AMIX -8.3% (secures Principal Investigators and Completes Clinical Training for First Human Study)

-RUN -7.9% (earnings, guidance)

-DRVN -7.2% (earnings, guidance)

-FIVN -7.1% (earnings, guidance)

-LCID -7.0% (earnings, guidance)

-ETSY -6.5% (earnings, guidance)

-GSM -6.3% (earnings, guidance)

-GRAB -5.0% (earnings, guidance; announces $500M share buyback program)

-FVRR -4.8% (earnings, guidance)

-KTOS -4.7% (files to sell $300M of common stock)

-ACRE -2.6% (earnings)

-JACK -2.6% (earnings, guidance)

-LKQ -2.6% (earnings, guidance)

BY Doug Kass · Feb 22, 2024, 9:06 AM EST

At 8:14 am:

BY Doug Kass · Feb 22, 2024, 8:55 AM EST

At 8:30 am:

BY Doug Kass · Feb 22, 2024, 8:45 AM EST

10:00 AM: Fed Vice Chair Jefferson (Voter) speaks on the U.S. economic outlook and monetary policy before a Peterson Institute for International Economics webcast, Washington, DC (Text available. Q&A from moderator and audience. Webcast at https://www.piie.com/events/2024/remarks-vice-chair-board-governors-federal-reserve- system-philip-n-jefferson);

3:15 PM: Fed Bank of Philadelphia President Harker (Non-Voter) speaks on the economic outlook before an event hosted by the University of Delaware Center for Economic Education, Newark, DE (Livestream expected. Text available. Audience Q&A expected. No media Q&A);

5:00P M: Board of Governors of the Fed- eral Reserve System member Lisa Cook (Voter) gives a keynote addresses at the 13th annual conference of the Julis-Rabinowitz Center for Public Policy & Finance (JRCPPF), Princeton University, Princeton, NJ; https://spia.princeton.edu/news/former-fed-chair-bernanke-current-fed-governor-cook-keynote-annual-jrcppf-conference;

5:00 PM: Fed Bank of Minneapolis President Kashkari (Non-Voter) participates in panel discussion on economic trends and outlook for 2024 and the growth of Minnesota's economy hosted by North- side Economic Opportunity Network (NEON) Community Conversations, Minneapolis, MN ( Audience Q&A expected. No media Q&A. Livestream at minneapolisfed.org/live);

7:35 PM: Fed Board Governor Waller (Voter) speaks on the economic outlook before the Notre Dame Club of Minnesota and University of St. Thomas Finding Forward Speaker Series, Minneapolis, MN (Text available. Q&A from moderator)

BY Doug Kass · Feb 22, 2024, 8:39 AM EST

* At the circus - a singalong!

* Groucho said Lydia, I said Nvidia...

Intro:

Oh this Nvidia EPS release brings back memories.

Childhood days, lemonade, romance.

Many portfolios are wrapped into Nvidia

Met her at the World's Fair in 1900...

Ah, Nvidia, she was the most glorious stock under the Sun!

Amazon, Alphabet, Apple... rolled into one!

In other words... and please sing along with Groucho and me:

Lydia the Tattooed Lady

Oh Lydia, oh, Lydia, say have you met Lydia

Oh, Nvidia, the tattooed lady

She has sales that folks adore so

And GAAP earnings even more so

Nvidia, oh, Nvidia, that encyclopedia

Oh, Nvidia, the queen of tattoo

On her back is the Battle of Waterloo

Beside it (short sellers') Wreck of the Hesperus too

And proudly above waves

The Red, White and Blue

You can learn a lot from NVDA

La la la la la la

La la la la la la

When a robe is unfurled Huang will show you the world

If you stand up and tell him where

For a dime you can see Kankakee or Paree

Or Washington crossing the Delaware

La la la la la la

La la la la la la

Oh, Lydia, oh, Lydia, say have you met Lydia

Oh, Nvidia, the tattooed lady

When her muscles start relaxin'

Up the hill comes that cool cat Jensen

Nvidia, oh, Nvidia, that encyclopedia

Oh, NVDA, the champ of them all

For two bits she will do a Mazurka in Jazz

With a view of Santa Clara that no company has

And on a clear day you can see Alcatraz

You can learn a lot from Nvidia

La la la la la la

La la la la la la

Come along and see Buffalo Bill with his lasso

Just a little classic by Mendel Picasso

Here is Captain Bezos exploring the Amazon

And Apple's Tim Cook, but with his pajamas on

La la la la la la

La la la la la la

Announced NVIDIA HGX™ H200 with the new NVIDIA H200 Tensor Core GPU, the first GPU with HBM3e memory, Over on the west coast investors have Treasure Island

Here is Sifei Liu doing the rhumba

And the company's $4.93 fully diluted earnings number.

Oh Lydia, oh, Lydia, say have you met Lydia

Oh, Nvidia, the tattooed lady

Lydia, oh, Lydia, that encyclopedia

Oh, Lydia, the queen of them all

She once swept an Admiral clear off his feet

The ships on her hips make portfolios skip a beat

And now the old boy NVDA is in command of the fleet

For he went and married Lydia

Groucho said Lydia (I said Nvidia)

Groucho said Lydia (Investors are buying Nvidia)

La la!

- Groucho Marx, Lyida The Tattooed Lady

Post Script:

BY Doug Kass · Feb 22, 2024, 7:50 AM EST

BY Doug Kass · Feb 22, 2024, 7:03 AM EST

The Street on Nvdia NVDA:

BY Doug Kass · Feb 22, 2024, 6:55 AM EST

“The impression has built up that the stock market is the cause of booms and busts. Actually, it is the thermometer -- not the fever.”

- Bernard Baruch

Bonus - Here are some great links:

BY Doug Kass · Feb 22, 2024, 6:45 AM EST

The irony of it all:

BY Doug Kass · Feb 22, 2024, 6:26 AM EST

A valuable insight:

BY Doug Kass · Feb 22, 2024, 6:15 AM EST

This is a valuable table for momentum-based short-term traders:

BY Doug Kass · Feb 22, 2024, 6:11 AM EST

From JPMorgan:

US: Futs are higher following NVDA’s earnings; the stock is +14% pre-mkt poised to propel markets to new all-time highs. All MegaCap Tech names are higher; keep an eye on AAPL as this had become a funding short inside the group and had fallen ~8% from its recent highs. Bond yields are flat to down 1bp; USD is weaker. Cmdtys are seeing strength across all 3 complexes. The econ data focus today is on Flash PMIs, Jobless claims, and existing home sales.

and...

EQUITY AND MACRO NARRATIVE: NVDA earnings hit post-market and stock moved ~7% higher after losing ~10% over the last week. Stating the obvious, the stock is poised to make new highs and taking each index with it. This may be a catalyst not only for the Street to get materially more bullish on US Equities but also to see a further decoupling of stocks and yields since the Mag7 are proving to deliver on earnings expectations irrespective of the interest rate environment.

BY Doug Kass · Feb 22, 2024, 6:01 AM EST

Wolf Street howls about QT.

BY Doug Kass · Feb 22, 2024, 5:53 AM EST