The United States reported a $1.7 trillion deficit for fiscal 2023 (the 12 months ended September 30, 2023), up $320 billion (+23.2%) from fiscal 2022 as revenues fell by $457 billion and expenses (miraculously) also fell by a lesser $137 billion. Total outlays were $6.134 trillion so the deficit represented 27.6% of total spending which was slightly lower than fiscal 2022 ($6.131 trillion vs. $6.272 trillion) due to reduced pandemic-related spending (-$170 billion), expiration of the expanded child tax credit ($177 billion), and lower spending on food and nutritional programs ($21 billion). Spending on social security (+$135 billion), Medicare (+$126 billion), Medicaid (+$24 billion) and interest on the national debt (+$177 billion) rose and will keep rising in the years ahead.

The deficit is on course to hit $40 trillion by 2027. Even the folks in Congress (some of them at least) can do the math and see that it will soon cost more than one trillion dollars annually to service this debt even under the most optimistic interest rate assumptions. The last time interest rates were at their current level in 2007, the federal deficit was equal to ~35% of GDP; today that ratio is ~98% and rising (I think it is much higher but am using the government's numbers but even these numbers should render you physically ill if you are paying attention. This alarming jump illustrates that the cost of servicing the debt is cannibalizing the budget at an accelerating rate. If it hasn't happened already, the Fed will soon lose its ability to fight inflation with higher rates because of their impact on the government's ability to service the federal deficit, a handicap that will unleash further inflationary pressures and threaten financial stability. This is why delaying action on the deficit is no longer an option. We are already at Defcon 5.

The national debt hit $33.6 trillion in mid-October 2023, up $10 trillion in less than four years (since the first quarter of 2020) as pandemic spending supercharged our appalling fiscal. The Congressional Budget Office projects the deficit will hit $54.5 trillion in 2033 as debt grows on an exponential rather than linear basis that is virtually impossible to reverse or slow. In particular, the rising burden of servicing this huge debt is going to grow as long as interest rates remain elevated (meaning until the Fed is forced to lower them to prevent an economic collapse). And even if interest rates drop, the rising quantum of debt will keep debt servicing costs elevated ad infinitum.

In fiscal 2023, $659 trillion (more than 10% of total spending) was spent on interest, up sharply from $475 trillion a year earlier. In fiscal 2024 it will be higher because much of the government's debt carries short maturities. Whoever decided to borrow short-term to fund our deficit must have worked in Silicon Valley Bank's Treasury Department. Unlike SIVB, however, there won't be anybody around to bail out the U.S. government or the U.S. dollar when these reckless spending habits hit the fan.

The Fed is now contributing to deficits by no longer returning capital to the Treasury as it did in previous years and by continuing to pay market rates on reserves. The latter policy will produce something on the order of $1.6 trillion of losses to U.S. taxpayers according to bank analyst Chris Whalen. Mr. Whalen further points out (along with others) that the U.S. economy looks deceivingly healthy due to the Fed's reluctance to aggressively reduce its balance sheet and take other steps to unwind the massive pandemic liquidity infusion that is still inflating economic activity: "The buoyant economy and job market are basically the result of the fact that the Fed has refused to drain liquidity from the economy causing, well, another liquidity crisis."

The 4.9% 3Q23 GDP print is best understood as the economy continuing to ride the tsunami of government spending unleashed during the pandemic; there is no way growth would be anywhere that number if the deficit wasn't closing in on two trillion dollars. Rather than marvel at the so-called strength of the economy, observers should be noting that it is not organic but driven by massive government stimulus still working through the system. Without that stimulus, growth would be much lower.

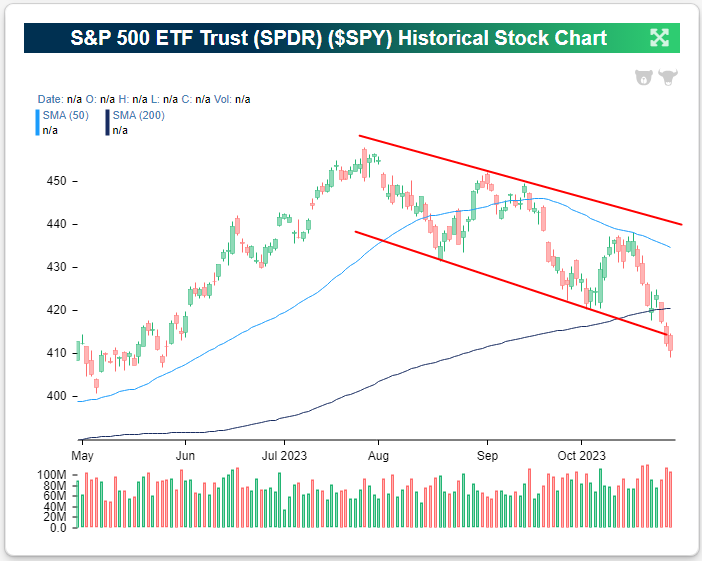

-- The S&P 500 made another "lower low" to end last week, which confirms the downtrend we've been in since the end of July.

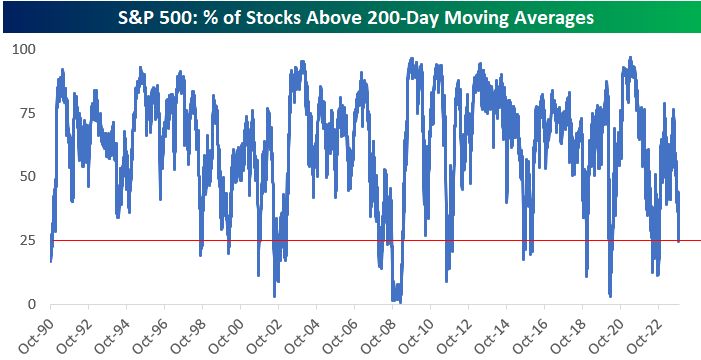

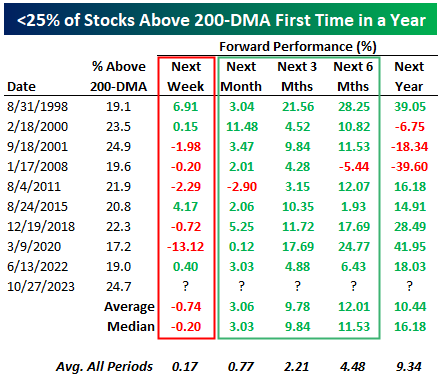

-- The percentage of S&P 500 stocks above their 200-day moving averages dipped below 25% for the first time in more than a year on Friday.

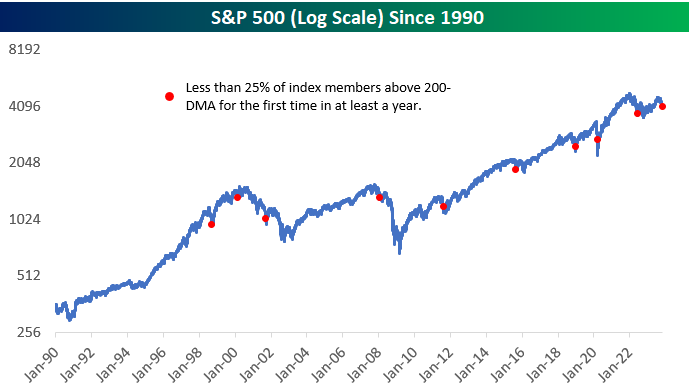

-- In the three months following breaks below 25% for this reading for the first time in at least a year, the S&P has been higher nine of nine times for an average gain of 9.78%.

Chartof the Day:

Technicals were a major "pro" for the market early on this year, but they have turned into a definitive "con" over the last couple of months. The S&P continues to make lower highs and lower lows, with the last lower high earlier this month not even reaching the top of the index's downtrend channel, and last week's lower low falling below the bottom of the same downtrend channel. Talk about ugly.

With every major US index ETF now trading in extreme oversold territory, there's certainly the possibility for upside mean reversion, but we'll need to see a significant rally from here for technicals to turn more bullish once again. The first step would be making a higher high above the highs from earlier this month, but the action has been so weak lately that the index now needs to rally more than 6% just to get there.

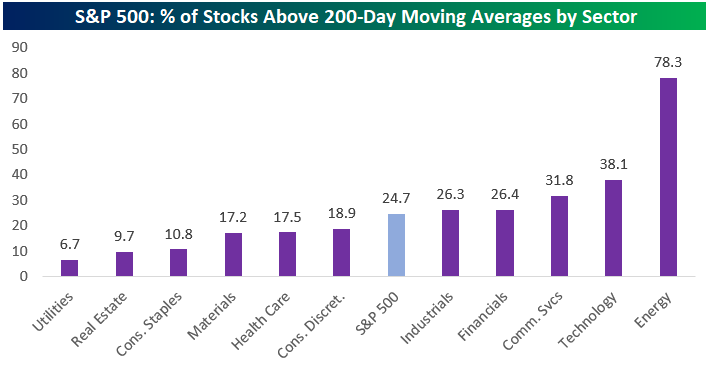

Underneath the surface, we've seen longer-term breadth measures also take a hit lately. As shown below, less than 25% of S&P 500 stocks are above their 200-day moving averages, with the weakness here in sectors like Consumer Discretionary, Health Care, Materials, Consumer Staples, Real Estate, and Utilities.

Below is a look at the percentage of S&P 500 stocks trading above their 200-day moving averages on a historical basis, with the 25% level marked by the red line on the chart.

Below is a log-scale chart of the S&P going back to 1990 with red dots denoting days where the percentage of stocks trading above their 200-day moving averages fell below 25% for the first time in at least a year.

The table below shows the dates of the red dots in the chart above along with how the S&P did in the weeks, months, and year following. What we see from the table is that the week following these breaks below 25% has been hit or miss, with average and median performance actually negative. But the next one to six months has been quite bullish.

In the month and six months after the percentage of S&P 500 stocks above their 200-DMAs dips below 25% for the first time in a year, the index was higher eight of nine times, and over the next three months, the index was higher nine out of nine times for an average gain of 9.78%. That three-month gain of 9.78% compares to an average gain of just 2.21% for all three-month periods in the S&P's history dating back to 1990.

A 9.78% gain between now and the end of January would only get us back to levels seen at the start of September, but investors would certainly take it after the brutal stretch we've had recently.

We are seeing a little bit of the dichotomy we discussed in this morning's commentary. We are clearly not seeing a flight to safety as yields inch higher and there is further discussion about the situation in Gaza.

The market is using a relatively new yardstick to measure and that being the potential limitations on Israel and its next step with public relations and demonstrations moving it and the negative pressure within Israel building around Netanyahu, which may be presenting him with handcuffs.

The net result is viewing the potential hostilities in a slightly muted sense, meaning those handcuffs may be out there.

There are rumors that Hamas is releasing some hostage videos on social media. So far, the mainstream media is not showing the photos nor actively discussing so as not to bring exposure to the hostages individually.

This appears to be the interim step over the next couple of days as the market tries to decide - are there limitations on the next step and does that limit negativity to the market, almost as a substitute for the flight to safety? May you live in interesting times indeed!

The yield on the ten-year got to 4.90% without any immediate pressure. The area between 4.90% and 5% will present interesting testing. The Halloween trick or treating may start this afternoon before the close.

The bounce off support at 4100 has helped the bulls. Let's see how they handle resistance at 4165/4175. A key factor is also what is going on in Tokyo with rumors and speculation that the Bank of Japan will be making changes to the yield curves and the like and what does that mean to things like the yield on the ten-year and the currencies.

It is a variable full buffet of things going on, but we think we are in a new phase interpreting those handcuffs and watching the yields from new areas. The resistance in the S&P and the yield on the ten-year probably becomes interesting at 4.95%.

BN: * BOJ TO TWEAK POLICY TO LET 10-YEAR YIELDS EXCEED 1%: NIKKEI

BN: * BOJ TO CONSIDER LETTING 10-YEAR YIELDS EXCEED 1%, NIKKEI SAYS

'Tweak' or 'Consider', we'll soon see. No word on negative rate policy yet.

US Treasury yields are back at high of morning at 4.90%. They came down before this announcement after Germany reported a lower than expected CPI print.

Yes, we'll hear from the Fed this week and the quarterly refunding needs from the US Treasury on Wednesday but the BoJ meeting might be the most important monetary/rate factor of them all this week when we hear from them tonight (Tuesday for them). You've heard me say all year that what happens there has a direct impact on our rates here.

Not that we expect the Fed to raise rates this week or even in December, but the moderation in rent growth just makes this decision easier because of the heavy weighting it has in the inflation stats, as we all know. Last week we heard from some publicly traded multi family REITS and they gave the blended rate growth they are experiencing.

Camden Property Trust (a stock we own) said "During the third quarter, our effective growth rates were .8% for new leases, 5.9% for renewals, and 3.4% for blended rate growth." This is trending even softer in October, in part due to seasonality, but "Effective blended lease rates for October remain positive at 1.4%."

Apartment completions will remain high thru next year but they said "On the supply side, starts have peaked, and the capital markets hurricane has begun to reduce new starts. Annualized August starts fell 42%. Witten Advisors project starts will fall to 250,000 units in 2024 and just above 200,000 units in 2025." Thus, after this moderation in rents which will carry into next year, rent price increases will head right back up again, especially if home prices and mortgage rates stay this high.

Elme Communities, another one we own, and has multi family apartments in the DC metro area and in Atlanta, said "We generated effective blended lease rate growth of 3% during the quarter for our same store portfolio comprised of renewal lease rate growth of 5.1% and new lease rate growth of .1%. Renewal rates remained strong throughout the fall and we continue to experience very strong resident retention...Thus far, we assigned renewal offers for October and November lease expirations at 5.5% on average." They have more Class B properties.

AvalonBay Communities is seeing little new lease growth but "we're seeing renewals come in at 4% to 4.5% depending on the more recent time period you're looking at." The increases they are sending to their tenants for November and December are starting at 6%.

Continuing on with the home, Mohawk Industries also reported last week, the big maker of everything from carpet to tile to rugs to countertops to wood and sheet vinyl. They saw a decline in y/o/y of sales "as our industry faced continued pressures across all regions primarily due to constrained residential investments and tightening of consumer discretionary spending."

"In the US, mortgage rates have climbed to their highest level in more than two decades which has suppressed the housing market and limited home renovation activity. In Europe, consumers are deferring large purchases such as flooring as a result of higher energy costs, inflation and uncertainty due to the war in Ukraine."

"Our industry faces a greater impact from these pressures than other sectors, given that most flooring purchases are deferrable. With the high fixed costs required to produce flooring, competition increases as the industry slows and participants attempt to increase their sales to maximize absorption. As a result, our average selling prices and mix have declined, with the impact partially offset by lower material and energy costs, restructuring benefits and process improvements."

While we absorb the robust Q3 GDP report, when it comes to the US existing home market and everything that flows from a transaction, it is clearly in a recession.

When it comes to this recession debate, my good friend David Rosenberg on Friday gave some historical perspective on strong GDP prints that were quickly followed by recessions. Here is what he said:

"We had 4.6% annualized real GDP growth in the third quarter of 2019 and we had a recession (with our without the pandemic) two quarters hence."

"We had a very nice 3.5% growth quarter in 2006 Q4, and the recession may have been deferred, but still crept on us a year later."

"We had a 7.5% growth quarter in the 2nd quarter of 2000 and the recession was just over two quarters down the road."

"We had a 4.4% pace posted in 1990 Q1 and yet, somehow, the recession began two quarters later."

"We had a 4.9% growth pop in 1981 Q3, and we were already in recession."

"We had a whopper of a 10.3% annualized GDP surge in the first quarter of 1973; one of the worst recessions ever recorded took hold two quarters after that blowout (the problem of borrowing too much growth from the future)."

"We had a 6.4% print in 1969 Q1. A leading indicator? I think not. The recession began three quarters after that blowout."

"We had a monster of a 9.3% growth rate in 1960 Q1, and the recession began the very next quarter."

"We had a huge 7.7% GDP surge in 1953 Q1...the recession? It started two quarters after that print."

Shifting back to earnings calls, and the other major interest rate sensitive sector, autos, AutoNation reported numbers. Here is what they said, remaining upbeat:

"There continues to be mixed economic signals in the economy, but despite concerns over affordability, consumer demand for vehicles remains relatively healthy. And during the quarter, partly because of improved new vehicle supply and stable used vehicle inventory, we saw double digit y/o/y growth in new vehicle sales and strong sequential growth in used vehicle volume." I guess the question from here is now that inventory levels have been normalized and customer demand possibly satiated as a result, what happens from here with financing costs so high? It's hard not to expect a slowdown because of high prices.

I want to comment on the overall corporate funding environment in this higher rate world and with the notable jump in long term interest rates since late July. In case you didn't see the Thursday FT article titled "Treasury Rout Deters US Companies from Borrowings as Finance Costs Soar, " it said "US groups have raised just under $70b from sales of bonds and leveraged loans in the month to date, the quietest month this year and the weakest pace of borrowings in any October since 2011, according to data from LSEG. The total of 50 deals is the lowest number at this point in the month, according to records going back 20 years."

Looking at the data overseas, the Eurozone October Economic Confidence index was little changed at 93.3 vs 93.4 in September but that is the softest since November 2020. The estimate was 93. Manufacturing weakness was offset by a lift in services. There were further declines in retail but little change in consumer and construction confidence.

This number doesn't move markets but helping to rally European bonds was the lower than expected Spanish CPI print for October that was up 3.5% y/o/y, 3 tenths below the estimate, though still up from 3.3% in September. The Spanish 10 yr inflation breakeven is down 3 bps in response. We'll get the German October print at 9am est. The euro is up a touch while the Spanish IBEX is jumping by 1.2%, outperforming Europe on the upside today.

Germany by the way said its economy contracted by .1% q/o/q in Q3, though one tenth better than feared and follows a .1% gain in Q2. Their economy has basically stagnated since Q1 2022.

As Friday's trading progressed, traders found that they could empathize more and more with the listeners to Welles program. The news was influential and not necessarily beneficial to either the market or to the overview of where things stood. There were military underpinnings and, as the day progressed, traders were not actually thinking about the end of the world, but they were thinking about a good deal of damage they were watching and that continued throughout the day. It had started out somewhat modestly lower at least by the final results and the news from Gaza was a key influence and filtered into the market throughout the day as the feeling of concern expanded as Israel expanded and then continued expanding its ground offensive.

That left a lot of questions of how wide would that go. What would be the extent of the influences? Would it bring in Lebanon in a second front? The U.S. sounded like it might be looking for a ceasefire, which it actually called for, but the Israeli's seemed to have little choice but to continue and both in the United States and certain capitals around the world, there were more and more protests in favor of what was viewed as a bad deal for the Palestinians. That gave a rather negative tone, as usually, Israel does not often get on the wrong side of the public relations picture.

All of these things continued to leave question marks and question marks always bother traders. The early selling seemed to fit very handily into the presumption of a consolidation day, but then as the reports grew of further increasing hostilities in the Middle East, things began to weaken a good deal further than the original thought of a consolidation day might be. By midday, the trading was heavily based on the news from the Middle East and prices had eroded further. So, that hanging onto the consolidation day was a bit of a gamble. We touched on some of that in this midafternoon recap:

10.27.23 Mid Afternoon Recap - The stock market gets the consolidation day we had assumed, but not as cleanly as it might have been. The techs continued to rebound thanks to the Amazon boost, while the Dow is the weakest of the lot,, pulled down by the surprisingly weak energy sector. We said surprisingly, since I would have thought the air strikes against the Iranian agents in Syria might have warmed things up in the whole region. That having been said, we will see how they work their way through the afternoon. The yield on the 10-year inches back up. If they manage to touch 4.90% or higher, it could send a chill to the equity markets.

For now, the jury is out, and we continue to favor the consolidation aspect, but as I say if the yields get higher the equity bears might take control. Most traders want to tiptoe into the weekend and get the World Series started. So far, the market appears not to cooperate. Stay close to the newsticker and watch the yields, particularly if they touch that 4.90% and, above all, try to stay safe, as we move into a chilly-looking weekend. Stay safe.

The last hour was a very interesting event. As the trading began to grow heavier, it looked like the S&P, which had violated a variety of presumed support areas like moving averages and such, went into the early afternoon, after the recap went out, and began to violate others - trendlines and the like and, it looked like the gods of Finance, might want to teach a sixty-year veteran a lesson in humility or at least modesty as they stood on the verge of blowing away the consolidation day.

It was saved in that interesting final hour as I said, because just as they looked like they were about to crack open like an egg, the sense of a flight to safety began. Gold began to move up sharply and the yields came off their highs. It was obvious that at the last minute, going into the weekend, people wanted to reduce their risk by going into that flight to safety and, in the perverse logic that lives in Wall Street, that then allowed for a very mild case of short covering and the stock prices came off the lows and the S&P avoided breaking the key psychological area of 4100, which might have prompted cascade selling. Strangely, although it was a rough day, some traders felt concerned that they might have been better if it were rougher.

You might recall, a week or so ago, I talked about a possible air pocket selloff, and we had every opportunity as we went into the final hour on Friday to hit one of those air pockets, perhaps on the breaking of 4100 and that could have led us to a possible capitulation bottom and might have made some of the equity trading bulls feel a bit more secure. At any rate, by the close, the market was clearly oversold, almost screaming for a rebound rally, but they never ring a bell in that manner and, remember that an oversold condition is a condition and not a signal.

Before we finish up with the technicals and get to the international global markets overnight, we have to note what looks to be a bit of nuance in the flight to safety and a bit of the perception of what is going on with the war in Gaza and nearby. There were some signs in last night's trading and, in fact, the day before in those markets that were showing their influence that we may be seeing a change in perception.

At the risk of sounding like Meet the Press, to some of us traders this appears to be what is going on. Usually, Israel pretty much has the upper hand in the public relations surrounding the attacks and the warfare in the area. Now, it appears some of that is changing. There is a virtually unprecedent amount of counter-Israeli, almost pro-Hamas demonstration going on in certain capitals and even here in the U.S. The other factor is that Netanyahu was already under some political pressure and seems to be under more, particularly over the weekend. He apparently engaged in some verbal finger pointing about whose fault it was that the intelligence groups appeared to completely have missed the planning for an implication of the attack on October 7th.

That has inspired a lot of chatter in Israel, including many calls for Netanyahu's resignation. So, traders looked at that and think that may represent a set of handcuffs that will make it difficult for him to pursue the war, particularly in any cases where casualties increase sharply and/or there is large loss of hostages, etc. All in all, traders and others are trying to reassess the status of how Israel stands in the hostilities. Will the pressure from outside and the apparent less than one hundred percent support from the current U.S. government force them to change the way Netanyahu and the Israelis as a whole pursue and manage the war?

That is causing a kind of minor crosscurrent between the flight to safety ranges and military assessments. Will that inhibit hostilities from flaring up? We will not get into what probably should be a book length dissertation, only to tell you we are probably at a stage now things may not be as they appear to be or appear to have gone in the past. Stay tuned for new twists and turns. On renewed weakness breaking 4100, might cause the techncials to bring in further problems and we will deal with the techncials later in the week. Now, it is time to get back to our foreign cousins and what has been happening in their equity market.

We had a little difficulty getting the perspective on the foreign markets. There may be some international communications problems. A couple of friends have noted that on that on a heliocentric basis (that is with the sun in the center of the solar system as it should be), there may be a lot of gravitational pull on the atmosphere and the ionosphere, and it could cause communication problems over the next two weeks. Okay, so much for the Captain Zodiac approach. At any rate, the foreign markets are showing modest changes. Japan equities closed down about 300 points in the Dow. Hong Kong closed basically flat, and Mainland China was up about 100 Dow points. India, on the other hand, was up stronger - maybe 180 points in the Dow.

Over in Europe, things are relatively quiet. As we go to press, London is trading up about 250 points in the Dow. Paris is up about 180 points in the Dow and Frankfurt is about the same as Paris.

The U.S. economic calendar is empty. So, traders will be wondering whether they will get tricks or treats as the week unfolds. Things look very, very quiet, but they will present more as we head into midweek and the FOMC decision making.

As we say, psychology on Gaza may be changing. We will have to read some of the military reports through a filter. As the old saying goes - whenever you find the key to the market, they change the locks. They sure know how to live up to that. We will watch to see if the emotions begin to change. Will the historical flight to safety begin to change also? For now, we will continue to look at the yields on the ten-year. I think if they tick back up at 4.90% and above, that could put a little stress on the equity markets.

Tomorrow is Halloween. Beware of things that go bump in the night as we move along.

In my judgment an increased amount of individual stocks and sectors are now at or approaching levels to where upside reward is improving relative to downside risk.

In certain situations a margin of safety is even in place.

Buying into this weakness in anticipation of a better market backdrop requires dispassion and a rigorous view of value, which is the fundamental calculus behind our security analysis.

It will soon be time to start tap dancing to work and buying and holding equities.

* There is no other large cap company with retail, advertising and cloud offerings...

The more work I do on Amazon's AMZN quarter the more I think it should be purchased and held.

Amazon is a retail share gainer with an AI/cloud kicker.

Though I have no idea how much the AI component is worth, it is the cherry on the top of the sundae.

New management at the job is apparently getting serious about the bottom line - so estimates might prove conservative over the next 2-3 years.

The valuation has come down and is reasonable:

20-22x 2025 GAAP EPS ($5.00-$6.25/share) compared to COST (trailing 38x) and WMT (26x).

While the existential threat of antitrust dampens so of my enthusiasm, if EPS growth is higher than expectations, Amazon can play a lot of catch up against Costco and Walmart.

This seems like a reasonable two to three year price target - based on a conservative EPS central point:

* Like bees to honey I am back guying cannabis stocks after their dramatic fall from grace since late August

In the words of a broken heart It's just emotion that's taken me over Tied up in sorrow, lost in my soul But if you don't come back Come home to me, darling You know that there'll be nobody left in this world to hold me tight Nobody left in this world to kiss goodnight Goodnight Goodnight

-MIRO +225% (to be acquired by United Therapeutics for $3.25/shr in cash plus additional $1.75/shr in cash upon the achievement of a clinical development milestone) -VYNE +50% (expected to advance into Phase 2b clinical trial in 1H24; announces $88M private placement) -ICU +30% (FDA issues Approvable Letter for Selective Cytopheretic Device for Pediatric Patients) -AUVI +24% (granted significant new patents by USPTO and enters into strategic partnership with Canon Virginia, Inc.) -CHRS +23% (momentum following FDA approval of LOQTORZI (toripalimab-tpzi) in all lines of treatment for Recurrent or Metastatic Nasopharyngeal Carcinoma) -RVPH +21% (global Pivotal Phase 3 RECOVER Trial of Brilaroxazine in Schizophrenia met primary endpoint) -DCPH +18% (MOTION Pivotal Phase 3 Study of Vimseltinib in Patients with Tenosynovial Giant Cell Tumor (TGCT) met primary and secondary endpoints; reports Q3 earnings) -MGTX +16% (Sanofi to purchase $30M of ordinary shares at $7.50/shr; MeiraGTx approached by multiple parties with strategic interest in different assets and actively pursuing these options) -SRC +13% (to be acquired by Realty Income in $9.3B all-stock deal; Spirit shareholders to receive 0.762 newly-issued Realty Income shares for each Spirit share) -MOGO +11% (comments on recent share price volatility; affirms FY23 guidance) -NXGL +10% (secures supply agreement with AbbVie) -KPTI +8.1% (announces clinical trial collaboration with BMY to evaluate novel CELMoD Agent CC- 92480 Mezigdomide in combination with Selinexor in patients with Relapsed/Refractory Multiple Myeloma) -WDC +8.0% (earnings, guidance; Board of Directors unanimously approves a plan to separate its HDD and Flash businesses) -JKS +7.0% (earnings, guidance) -XPO +6.9% (earnings, guidance) -PHAT +6.1% (announces FDA Approval of Reformulated Vonoprazan Tablets for VOQUEZNA TRIPLE PAK (vonoprazan, amoxicillin, clarithromycin) and VOQUEZNA DUAL PAK (vonoprazan, amoxicillin) for the treatment of H. pylori Infection in adults) -SOFI +5.4% (earnings, guidance) -NYAX +3.5% (acquires retail point of sale software firm Retail Pro International for EV of $36.5M on a cash-free debt-free basis) -LITE +3.4% (to acquire optical interconnect co Cloud Light to accelerate data center Speed and Scalability for $750M in cash; reports prelim Q1) -MCD +2.8% (earnings, guidance) -HOLI +2.3% (provides update on sale process)

Downside

-COMM -24% (reports prelim earnings, guidance) -EAR -11% (to be taken private by Patient Square Capital for $2.55/shr) -RVTY -9.2% (earnings, guidance) -TECH -5.9% (President and CEO Chuck Kummeth to retire; Names Kim Kelderman as next CEO) -FDMT -5.0% (gains alignment with FDA on plan to lift Clinical Hold on Phase 1/2 INGLAXA clinical trial for 4D-310 for Fabry Disease Cardiomyopathy) -ON -4.1% (earnings, guidance) -CHKP -2.9% (earnings) -CTVA -2.5% (earnings, guidance)

"The stock market will do whatever it has to do to embarrass the greatest people to the greatest extent possible." -- Wally Deemer

"Workin' on our night moves Trying to lose the awkward teenage blues Workin' on our night moves In the summertime And oh the wonder Felt the lightning And we waited on the thunder Waited on the thunder."

This daily Futures feature is like inside baseball. I try to show you and write about what I believe thoughtful hedge fund managers are looking at when they awake -- let's call it our normal routine -- setting the stage for their strategy for the day. The market is a complicated mosaic and the more info you have, the better trader and investor you will be!

The market (and money) never sleeps -- and neither do I, it appears! I have previously described the importance that overnight futures trading hold for me here. It is a guidepost to my strategy in the regular trading session. Moreover, the overnight/early morning futures hold opportunities as they are (1) inefficient, though liquid and (2) it seems fear and greed are often exaggerated outside the regular trading session. I frequently try to capture those efficiencies by trading actively both in the pre- and after-market sessions.

Here are brief observations I wanted to highlight and provide a summary of overnight price movements in various asset classes:

* Stock futures were stronger all evening. S&P futures peaked at +29 and bottomed at +5. Nasdaq futures peaked at+134 and bottomed at +41. At 6:39 am ET, S&P futures were +24 and Nasdaq futures were +102.

* The S&P Short-Range Oscillator is increasingly oversold, at -5.89% vs. -5.18%.

* The VIX is now at 20.83 a loss of -0.44. I am actively trading straddles, selling on VIX spikes and covering on VIX drops. But my more constructive view caused me to take off the short SPY calls leg of my straddle.

* Treasury yields are subdued this morning. The 2-Year Treasury yield is +3 bps at 5.042% and the 10-Year is +2 bps at 4.87%. Over there, the yield on the 10-Year U.K. Gilt bond is up by one basis point.

Here is a synopsis of some of my columns I believe were important, or in the event you were out for the day and/or did not read my Diary. The principal intent is to review the logic of my market moves and other factors:

From JPMorgan, asking whether a bottom is forming:

US: Futs are higher, potentially setting up a relief rally into month-end or does the selling pressure continue with SPX under its 200dma (4,240)? MegaCap Tech names all positive pre-mkt. Bond yields in the belly are +2-3bps while USD is off a touch. Cmdtys are mixed with Energy weaker and Ags/Metals rallying. Base metals appear to be boosted by China's fiscal stimulus as precious metals are being sold. This is a heavy data week with ISM, Housing prices, ADP/NFP, Consumer Confidence, and Durable/Cap Goods plus the Fed and the Treasury's refunding announcement. Earnings are headlined by AAPL and Consumer-sector names.

and...

EQUITY AND MACRO NARRATIVE: Real GDP growth has averaged 3% this year, the unemployment rate is 3.6% while the economy has averaged adding 270k jobs each month this year. YoY CPI has fallen from 6.4% in January to 3.7% with Core CPI YoY has fallen from 5.6% to 4.1%. The jumps in productivity (4.7% annualized) give some comfort that we can continue this growth, without a material increase in inflation, and without triggering recession.

This economic growth is showing up in corporate profits. With ~40% of the SPX having reported, we are seeing +12% YoY EPS Growth; 78% of companies have beaten estimates by an average of 8%. Revenue growth is +4% YoY, only 48% of companies are beating revenue estimates, surprising by +1%. EPS growth is seen in 8 of the 11 major sectors with Energy flat and Materials/Real Estate delivering negative EPS growth. Revenue growth is seen in 9 of 11 sectors with Energy/Materials seeing negative YoY growth. Across all US businesses, the Econ team see a 20% increase in corporate profits (Kasman; here).

This environment should be positive for stocks, but we have seen SPX and NDX all enter correction territory this week, down 10.3% and 10.5% from their July peaks. RTY is less than 2% away from being in a bear market, down 18.3% from its July peak. These moves have occurred as the 10Y yield increased from 3.96% to 4.83% and the MOVE increased 112 to 129; VIX has increased from 13.63 to 21.27. The yield curve is seeming repricing this above trend growth, higher-for-long, and a deteriorating supply/demand for bond issuance. Jay Barry has increased his YE23 forecast for the 10Y from 3.5% on July 28 (here) to 4.75% currently (here), reflecting how quickly the economic outlook has improved driven by the consumer.

Where from here? A few thoughts:

HISTORY OF CORRECTIONS- Since 1980, a 10%+ pullback happens about once every 1.2 years; the average decline is 14.3% over 4 months. 5% pullbacks are more frequent, averaging 4.5 times per year (Covenant).

EARNINGS- the absolute prints have been strong but forward guidance remains poor given the lack of consensus among economists (Fed, sell-side, corporate) on FY24 and incessant media headlines flagging an imminent recession driven by consumer/corporate deterioration. Regarding media, the data do not support that conclusion with US household balance sheets, ex-subprime, still in better shape than at any time pre-COVID and the same is true of the IG and HY universes. Price action around earnings has been poor, illustrated by MegaCap Tech.

FACTORS / POSITIONING- Our Delta One team's PURE Beta factor (JPBPURE Index in BBG) is experiencing an extreme drawdown, surpassed only by COVID and the inflation shock of summer of 2022. This suggests that elevated probability of a squeeze that drives Equities higher especially if we see risk reduction in any combination of earnings, geopolitical, or macro. Keep an eye on the team's Squeeze basket (JP9PSQZ Index in BBG). For more color on how to trade this, access to the Bloomberg components, and/or for the full note, please contact the team here. Separately, Positioning Intelligence told us, "What is the risk of a short squeeze now? Still present, but potentially delayed...A squeeze might not accelerate unless we get 1) evidence consumer spending isn't slowing too much, 2) relatively good earnings season, 3) Fed communicating they're on hold. Given the conditions that might have to be met, a sustained move higher in shorts seems like a greater possibility in Nov than right now."

* To me he was a cross between Warren Buffett and Satchel Paige

* As a mentor, I have always sought Byron's approval and I wrote today's column as if he was looking over my shoulder...

"Disasters have a way of not happening."

- Byron Wien

I first met Byron Wien in 1980 through an introduction by Scarsdale Fats (Bob Brimberg) The Contrarian: Taking a Cue from 'Scarsdale Fats' - TheStreet and, a bit later, when I became a member of the First Tuesday of the Month Club. The First Tuesday of the Month Club included The Bearded Prophet of the Apocalypse (Tony Cillufo) Link Susan Byrne (Westwood Management), Salomon Brothers' Lou Margolis, Rocker Partners Dave Rocker, (then) Goldman Sachs' Lee Cooperman, JPMorgan's Fran Bovich and a few other investment luminaries.

We quickly became friends and he became an important mentor to me.

If memory serves me right, Byron was orphaned at 14 years of age. His dad, a doctor, had previously passed away when Byron was nine years old. Both his parents suffered from rheumatic fever and had weak hearts. His aunt became his guardian.

He attended Harvard College and got his MBA at Harvard Business School.

Byron's business career (at Morgan Stanley, Blackstone, etc.) is legendary but I have always found his back story more interesting.

Twenty one years ago I began to write an annual List of Surprises, purposely emulating Byron's list which he began in 1986 (sixteen years earlier).

What did I learn from Byron? A lot of things.

But few as important as the quote I started this column with.

Byron did not suffer fools lightly but he accumulated a vast network of friends and investors.

We dueled in our Annual Surprises Lists since 2002. I so anxiously awaited is constructive criticism and responses to my List on TheStreet.com.

Here is a sampling of a portion of his most recent emails Byron sent to me this year, including some nice responses to my Surprise Lists:

My last physical encounter with Byron was at Ira Harris' house in Palm Beach two years ago which was done in Byron's and Anita's honor. As always, he held court (in this case with Jeff Greene, Lee Cooperman, Jerry Jordan, Lowes' Joe Rosenberg and their wives), much like his annual Hamptons Benchmark Lunches enclave every Summer with the greatest minds in Wall Street and Industry. Byron Wien: Complacency Gives Way to Uncertainty - Blackstone Private Wealth Solutions

As to the quote I started this column with (previously referenced), it singularly helped my investment career and was partially responsible for my reliance at calculus of upside reward vs. downside risk.

As someone with a short selling bias, and with multiple economic tragedies and market swoons over the last several decades it was easy to get bearish at the bottom when things (especially to a "first level thinker") were obvious. But Byron taught me that it was always darkest at the dawn and disasters rarely happen. His dictum emboldened me to buy in March, 2009, in May, 2020 and in October, 2022 (among other times).

Byron's greatest talent, at least the way I viewed it, was his ability to identify secular changes.

Though generally upbeat, he has accurately predicted (starting back around 2020) that global economic growth rates would slow relative to history and that there would be a widening schism between the haves and the have nots - the standard of living for many people would be on the descent.

He also accurately predicted a rise in social unrest in the U.S. stating that "the future for those born now is not so bright."

Byron had an endearing twinkle in his eye when he smiled.

An avaricious reader. Byron used to tell me owed a lot to Harvard - he was handpicked by his public high school to apply. I think that is where he got his confidence and he long said he owed a lot to Harvard.

Here is my second favorite quote by Byron:

"I still ski, play tennis, sail and make love, although my skills at all of these have deteriorated. "

Come to think of it, Byron's work ethic was as solid as it gets and his investment wisdom was a cross between Warren Buffett and the legendary baseball pitcher Satchel Paige.

* His quote at the beginning of the column ("disasters have a way of not happening") is reminiscent of Buffett's:

"In the 20th century, the United States endured two world wars and other traumatic and expensive military conflicts; the Depression; a dozen or so recessions and financial panics; oil shocks; a flu epidemic; and the resignation of a disgraced president. Yet the Dow rose from 66 to 11,497."

* Many of his lessons also remind me much of Satchel Paige's philosophies on life:

"Age is a case of mind over matter. If you don't mind, it don't matter."

"How old would you be if you didn't know how old you are?"

" Work like you don't need the money. Love like you've never been hurt. Dance like nobody's watching."

"I've said it once and I'll say it a hundred times, I'm forty four years old."

Ten years ago, in the Jewish Journal, Byron reflected upon the lessons he learned over his first eight decades of his life (I have found it beneficial to read these every few years and you might also!):

Here are some of the lessons I have learned in my first 80 years. I hope to continue to practice them in the next 80:

Concentrate on finding a big idea that will make an impact on the people you want to influence. The Ten Surprises, which I started doing in 1986, has been a defining product. People all over the world are aware of it and identify me with it. What they seem to like about it is that I put myself at risk by going on record with these events which I believe are probable and hold myself accountable at year-end. If you want to be successful and live a long, stimulating life, keep yourself at risk intellectually all the time.

Network intensely. Luck plays a big role in life, and there is no better way to increase your luck than by knowing as many people as possible. Nurture your network by sending articles, books and emails to people to show you're thinking about them. Write op-eds and thought pieces for major publications. Organize discussion groups to bring your thoughtful friends together.

When you meet someone new, treat that person as a friend. Assume he or she is a winner and will become a positive force in your life. Most people wait for others to prove their value. Give them the benefit of the doubt from the start. Occasionally you will be disappointed, but your network will broaden rapidly if you follow this path.

Read all the time. Don't just do it because you're curious about something, read actively. Have a point of view before you start a book or article and see if what you think is confirmed or refuted by the author. If you do that, you will read faster and comprehend more.

Get enough sleep. Seven hours will do until you're sixty, eight from sixty to seventy, nine thereafter, which might include eight hours at night and a one-hour afternoon nap.

Try to think of your life in phases so you can avoid a burn-out. Do the numbers crunching in the early phase of your career. Try developing concepts later on. Stay at risk throughout the process.

Travel extensively. Try to get everywhere before you wear out. Attempt to meet local interesting people where you travel and keep in contact with them throughout your life. See them when you return to a place.

When meeting someone new, try to find out what formative experience occurred in their lives before they were seventeen. It is my belief that some important event in everyone's youth has an influence on everything that occurs afterwards.

On philanthropy my approach is to try to relieve pain rather than spread joy. Music, theatre and art museums have many affluent supporters, give the best parties and can add to your social luster in a community. They don't need you. Social service, hospitals and educational institutions can make the world a better place and help the disadvantaged make their way toward the American dream.

Younger people are naturally insecure and tend to overplay their accomplishments. Most people don't become comfortable with who they are until they're in their 40's. By that time they can underplay their achievements and become a nicer, more likeable person. Try to get to that point as soon as you can.

Take the time to give those who work for you a pat on the back when they do good work. Most people are so focused on the next challenge that they fail to thank the people who support them. It is important to do this. It motivates and inspires people and encourages them to perform at a higher level.

When someone extends a kindness to you write them a handwritten note, not an e- mail. Handwritten notes make an impact and are not quickly forgotten.

At the beginning of every year think of ways you can do your job better than you have ever done it before. Write them down and look at what you have set out for yourself when the year is over.

The hard way is always the right way. Never take shortcuts, except when driving home from the Hamptons. Short-cuts can be construed as sloppiness, a career killer.

Don't try to be better than your competitors, try to be different. There is always going to be someone smarter than you, but there may not be someone who is more imaginative.

When seeking a career as you come out of school or making a job change, always take the job that looks like it will be the most enjoyable. If it pays the most, you're lucky. If it doesn't, take it anyway, I took a severe pay cut to take each of the two best jobs I've ever had, and they both turned out to be exceptionally rewarding financially.

There is a perfect job out there for everyone. Most people never find it. Keep looking. The goal of life is to be a happy person and the right job is essential to that.

When your children are grown or if you have no children, always find someone younger to mentor. It is very satisfying to help someone steer through life's obstacles, and you'll be surprised at how much you will learn in the process.

Every year try doing something you have never done before that is totally out of your comfort zone. It could be running a marathon, attending a conference that interests you on an off-beat subject that will be populated by people very different from your usual circle of associates and friends or traveling to an obscure destination alone. This will add to the essential process of self-discovery.

Never retire. If you work forever, you can live forever. I know there is an abundance of biological evidence against this theory, but I'm going with it anyway.

It should be clear by this list as well as the broad market knowledge he delivered over the years that we can all still learn from Byron.

I have been buying as opportunities may abound - a byproduct of an emotional and a volatile market that has reached a potentially important support level ($409, SPY ).

Volatility provides both trading and investing opportunities.

Capitalizing on market structure's changing impact on generating higher volatility - and doing so unemotionally, as I did in covering a number of shorts and going longer on Friday, is the essence of my approach at my hedge fund, Seabreeze Partners.