Closing Numbers

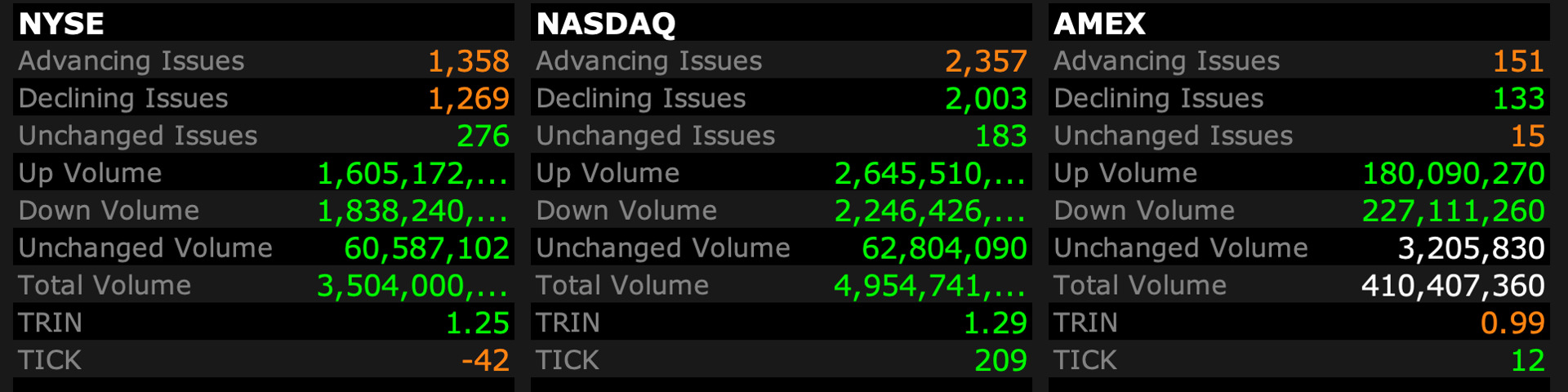

Closing Breadth

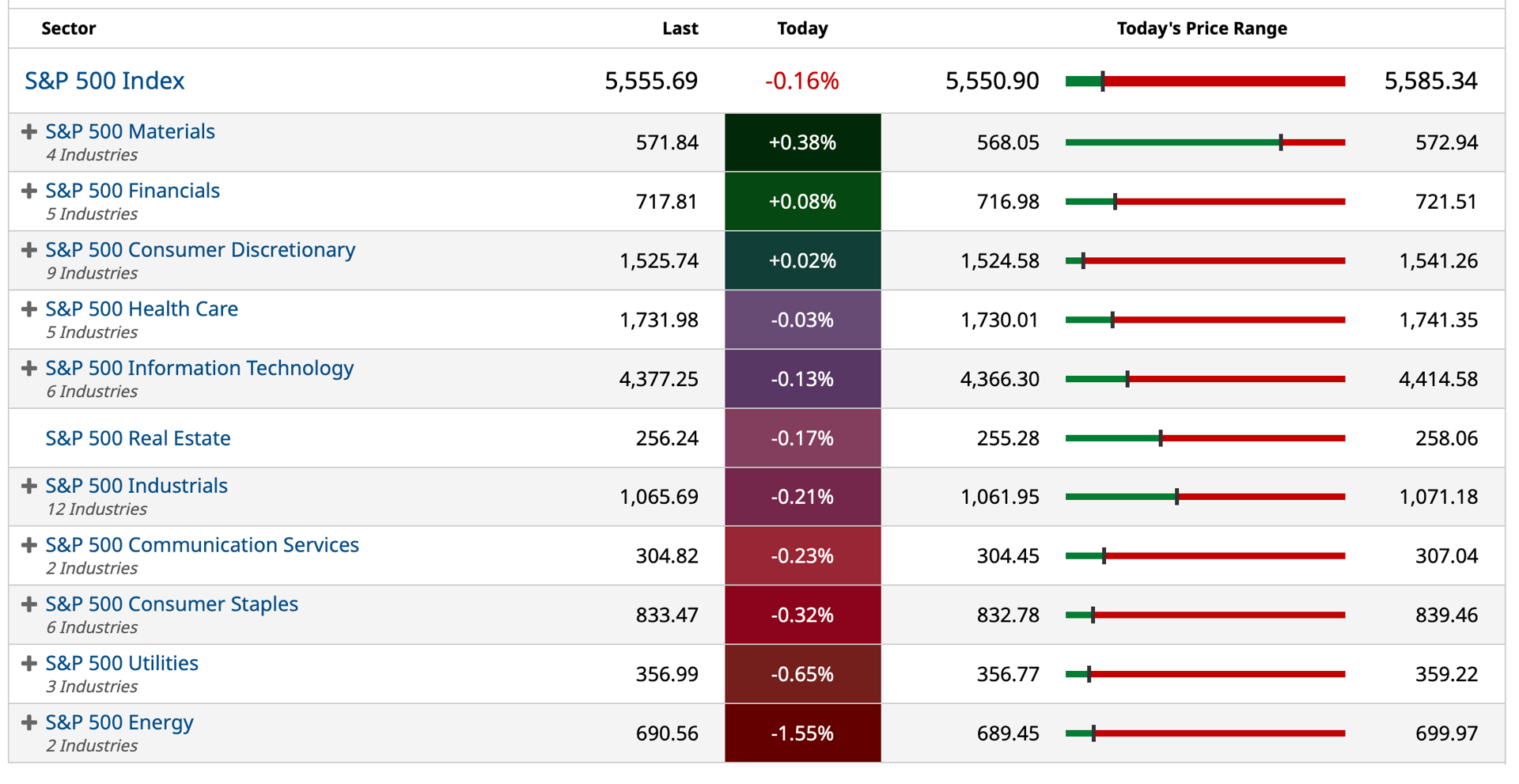

S&P 500 Sectors

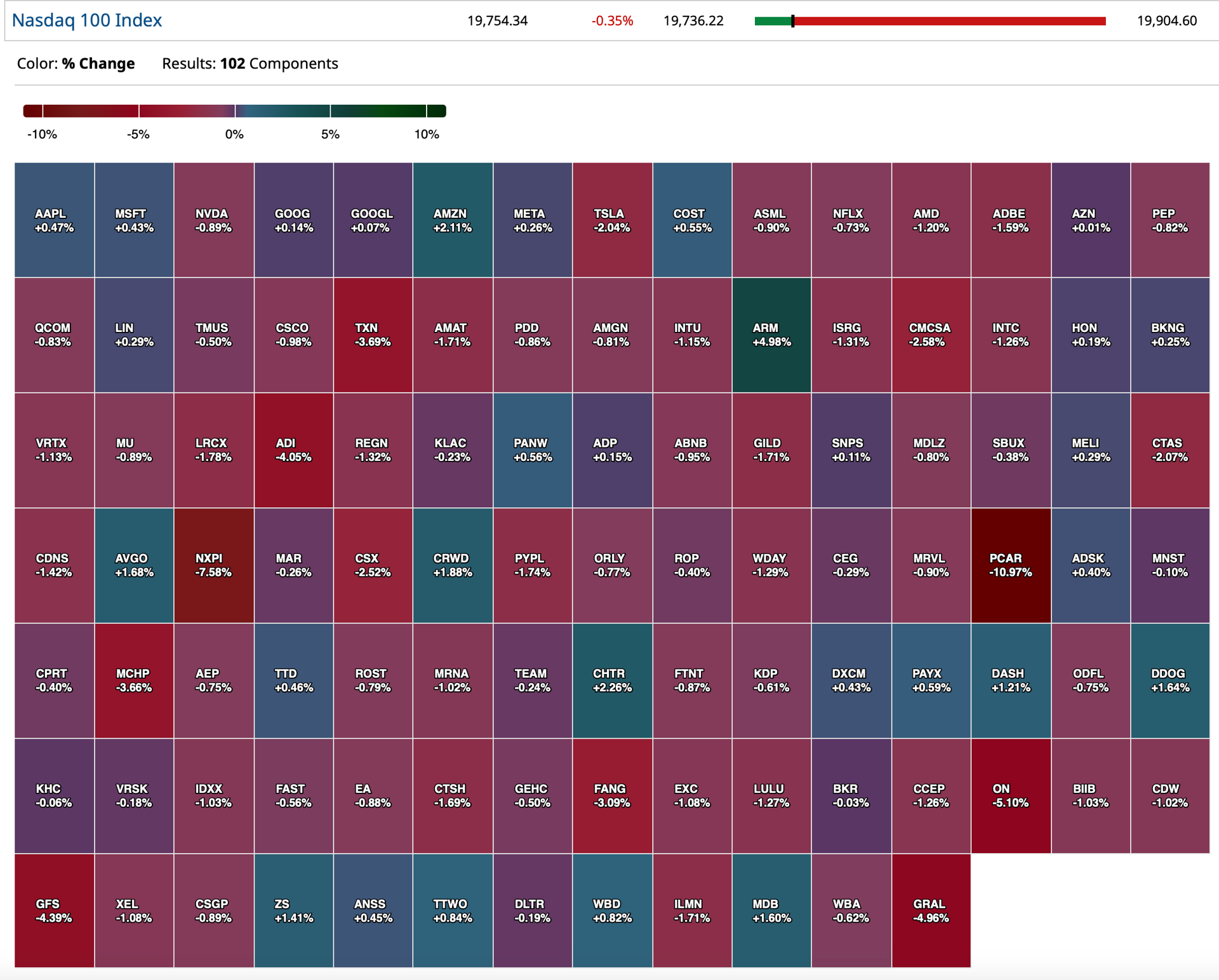

Nasdaq 100 Heat Map

BY Doug Kass · Jul 23, 2024, 4:56 PM EDT

BY Doug Kass · Jul 23, 2024, 4:56 PM EDT

As of 4:25 p.m.:

BY Doug Kass · Jul 23, 2024, 4:45 PM EDT

"Just one more thing."

- Lt. Columbo

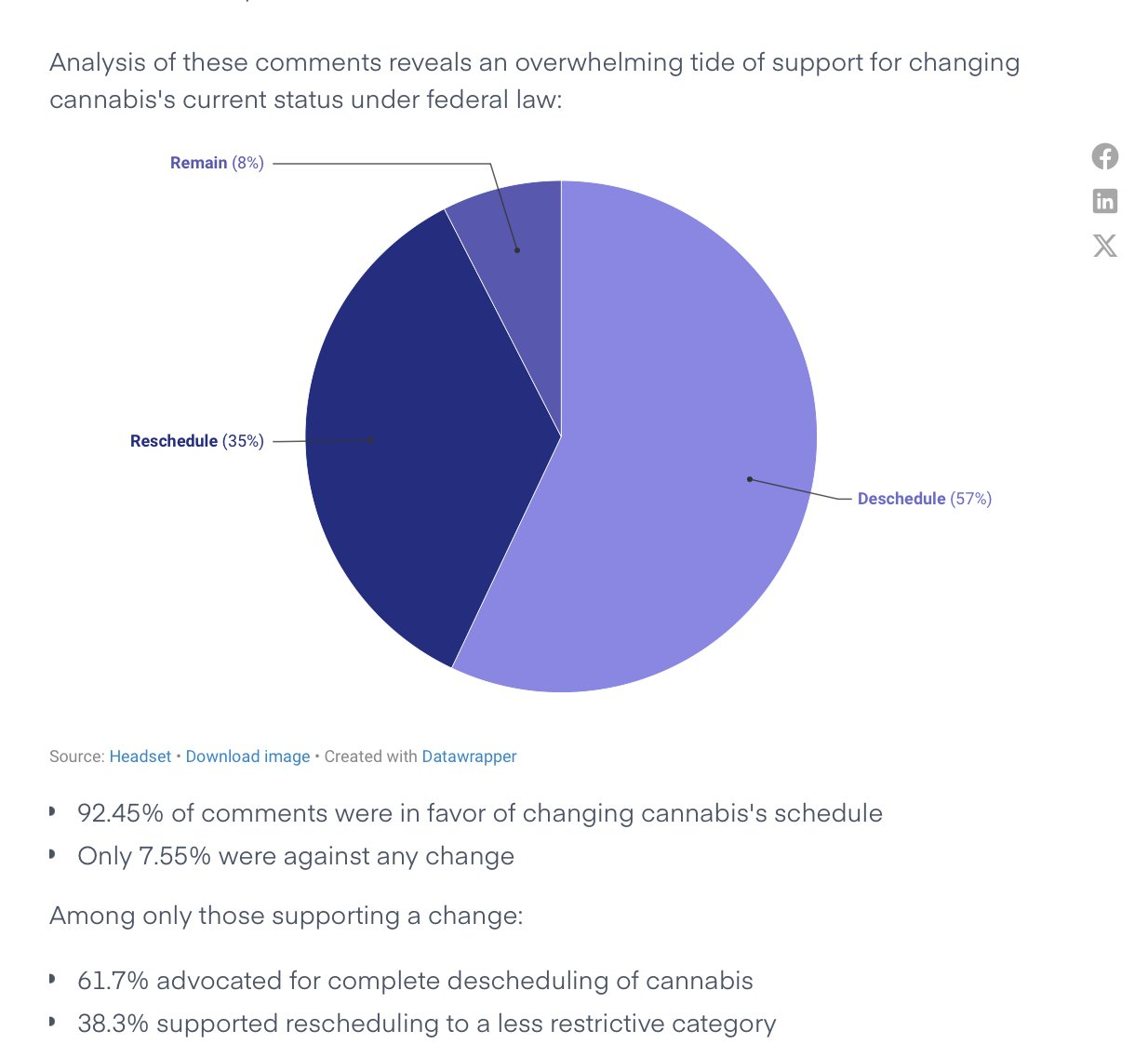

For cannabis holders — regarding comments period on rescheduling:

Full report:

BY Doug Kass · Jul 23, 2024, 4:02 PM EDT

I am calling it a day early as I have a bad sinus infection that is bothering me.

I hope the Methylprednisolone cycle and the arithromycin clicks in soon!

Thanks for reading.

Be safe.

BY Doug Kass · Jul 23, 2024, 3:35 PM EDT

Bret Jensen has the ticket in his comment I posted on my Diary this afternoon:

* The S&P Index trades at about 22x forward EPS forecasts.

* The earnings yield on the S&P Index is 4.55%.

* The S&P earnings yield of 4.55% compares to the following risk-free rates of return: the yield of 5.32% on the 3-month Treasury bill, the yield of 5.18% on the 6-month Treasury bill and the 4.49% yield on the 2-year Treasury note

* The risk-free rate of return (of about 5%) is nearly 4x the S&P dividend yield of 1.32% — the widest spread in decades (just as the equity risk premium is the lowest in 22 years!).

Everyone is bullish. (Just read the confidence expressed regarding the upward slope of equities by the chartmasters in Charting The Technicals posted daily in my Diary).

What could possibly go wrong?

BY Doug Kass · Jul 23, 2024, 2:14 PM EDT

From Peter Boockvar:

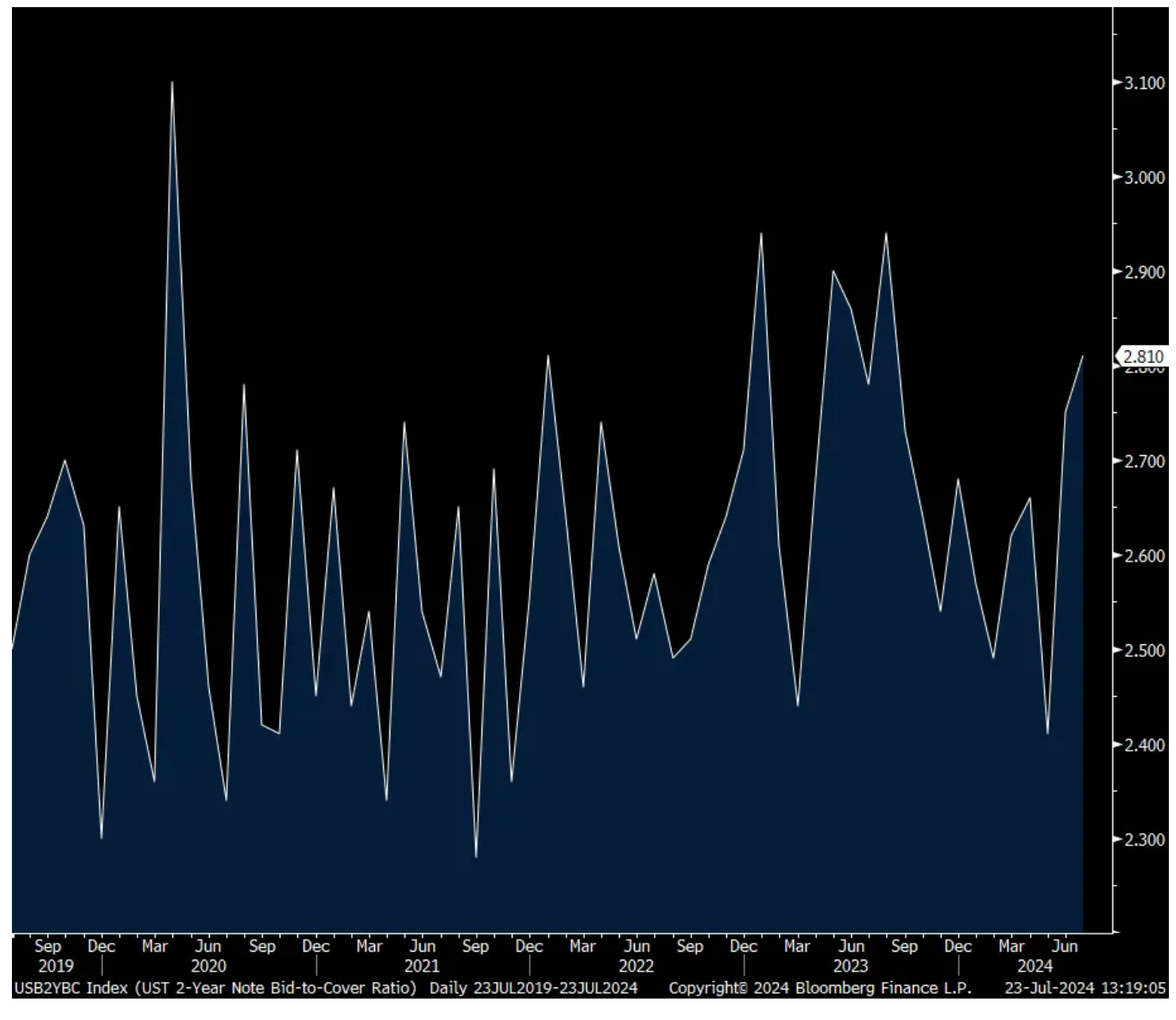

2 yr auction excellent, all in on rate cuts

I rarely write on the 2 yr auction as it remains tied to expectations for Fed policy rather than general market expectations of inflation, growth, etc…Well, today is worthy of a comment as the auction was excellent. The yield of 4.434% was about 2 bps below the when issued, tailing well. The bid to cover of 2.81 was above the previous 12 month average of 2.65 and the best since last August. Also, direct and indirect bidders took down 91% of the auction, the most since I have data going back to 2003.

Bottom line, the messaging here seems easy. Market buyers today expect rate cuts from the Fed and stretching out a year from now by looking at the July 2025 fed funds futures yield (barely trades keep in mind), has the fed funds rate at around 4.00% vs the current effective rate of 5.33%. As many are trained by the Fed for decades to cut rates in aggressive fashion in response to a recession, today’s ‘vote’ assumes they will keep on going on past that time frame. While I think the 2 yr Treasury is attractive here (certainly more attractive when it was closer to 5%) and we’re buying it, I don’t think the Fed will have the same ability to react to an economic downturn like they have in the past.

2 yr Bid to Cover

BY Doug Kass · Jul 23, 2024, 1:40 PM EDT

From "Meet" Bret Jensen:

Bret Jensen

Does it matter? It is pretty obvious he hasn't been in charge of much since 01/20/2021 at this point. Given the massive explosion of debt and fast slowing economic growth, it is only a matter of time before the economy settles into Stagflation for some time or worse in the coming quarters, regardless of who is in the WH. Fortunately, the S&P 500 is 'only' valued at approximately 22 times forward earnings when the risk-free 10-Year Treasury yields 4.25%. Just because the overall market is selling at a much richer valuation (based on P/S, P/B, Market Cap to GDP ratio, etc) than at the end of the Internet Boom, I am sure everything is truly 'different' this time around and the Federal Reserve will magically achieve only their second 'soft landing' in my near 58 years on this planet. AKA, nothing to worry about here. Move along. JMTC

BY Doug Kass · Jul 23, 2024, 12:50 PM EDT

I have a corporate board meeting between noon and 2 p.m.

Radio silence.

BY Doug Kass · Jul 23, 2024, 12:11 PM EDT

With S&P cash +17 handles I am shorting my next batch of index calls.

BY Doug Kass · Jul 23, 2024, 11:35 AM EDT

What follows is a compilation of recent commentary in my Diary and comments delivered to my investors at my hedge fund, Seabreeze Partners:

To me, the stock market's advance this year has represented a challenge to value investors and to rational thought and analysis.

Investors, in our view, have not been compensated properly for the economic, profit, valuation, political, geopolitical and market structure risks I have expressed in my Diary throughout this year. Moreover, the interaction of monetary and fiscal policy has now lead to a toxic brew – contributing to a nation of (nearly unfinanceable) entitlements with a bloated balance sheet and an unsustainable budget.

It has been most surprising that investors have continued to ignore that equities are materially overvalued relative to interest rates - with the equity risk premium at a twenty-year low.

I recognize that I am in a small minority in embracing a negative market view. I am accustomed to being outside the herd (when justified) - it is not dissimilar to my pessimistic and non-consensus views expressed in the Summer of 2007 or in the early Winter of 2021.

That said and as previously noted (and until recently), I have done a poor job in forecasting the market. At the same time, I have been a good risk manager - as despite our positioning in 2024 (on average at about 15% net short), I have sidestepped losses in achieving modest but positive returns.

My investment approach is consistent and doesn't change with the weather. As always, a value-oriented investment process considers upside reward relative to downside risk with an eye towards achieving "a margin of safety."

There is nothing like price to change investor sentiment (h/t "The Divine Ms. M"). Both Warren Buffett (Berkshire Hathaway) and I (Seabreeze) question why investors today would prefer to buy high and sell low. Given the dominance of passive products and strategies we have seen even more price following and reverence.

I am dispassionate in the implementation of my strategy - viewing high stock prices as the enemy of the rational investor and low prices as our ally. I don't worship at the altar of price and chase equities (when climbing) for the sake of investment performance when the fundamentals do not justify ownership. Security analysis, when done properly, allows one to determine "intrinsic values" and gives one confidence in exploiting the sort of wild price swings that have become commonplace.

This approach, while it might be wrong during certain discrete periods of time, will likely prove quite correct through a market cycle. (At least that is my experience!)

"Rule No 1: never lose money. Rule No 2: never forget rule No 1."

- Warren Buffett

When I am wrong, as I have been this year, it is naturally reflected in weak relative performance. However, even when wrong I am always attentive to risk management. As a reflection of this, my hedge fund has not lost money in the face of a sharp market climb (and have actually made some money). But, when I am correct, as was the case in 2022, it is reflected in strong relative performance. (See The Oracle's quote above!)

***

Most notably and since last month's commentary, the domestic economy's outlook has eroded and the prospects for U.S. corporate profit growth have deteriorated.

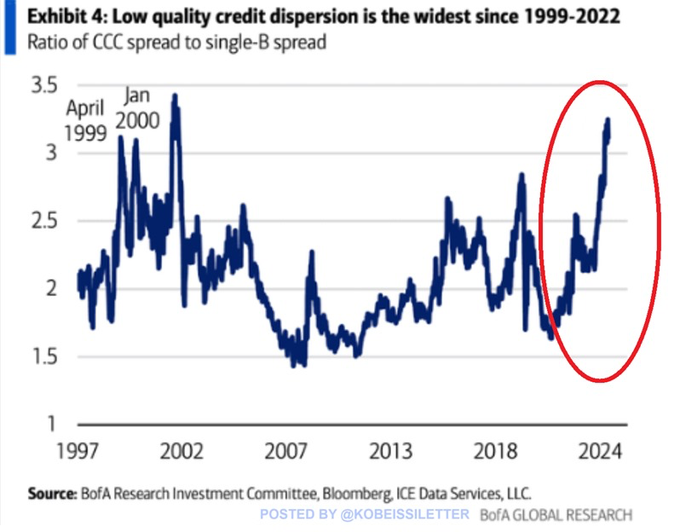

Corporate bond markets are flashing warning signs: Low-quality U.S. corporate bond credit spreads have spiked to the widest since 2001. In fact, the ratio of CCC-rated spread to B-rated spread has DOUBLED in the last 2 1/2 years. This difference is now even wider than the run up to the 2000 Dot.com bubble. Meanwhile, 346 large corporations have declared bankruptcy through June, 2024, the most since 2010:

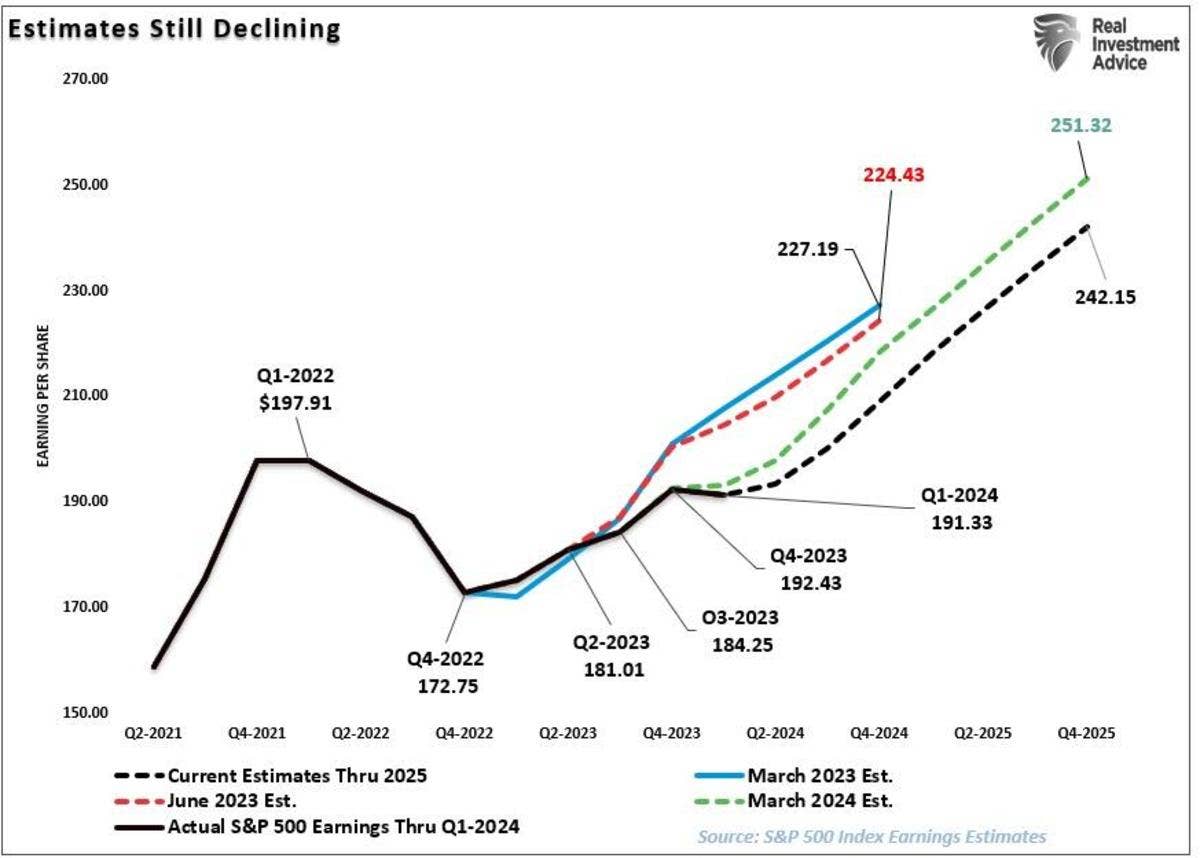

Optimism surrounding strong corporate profit growth in 2024-25 (used by many to rationalize today's high stock prices) seems unjustified.

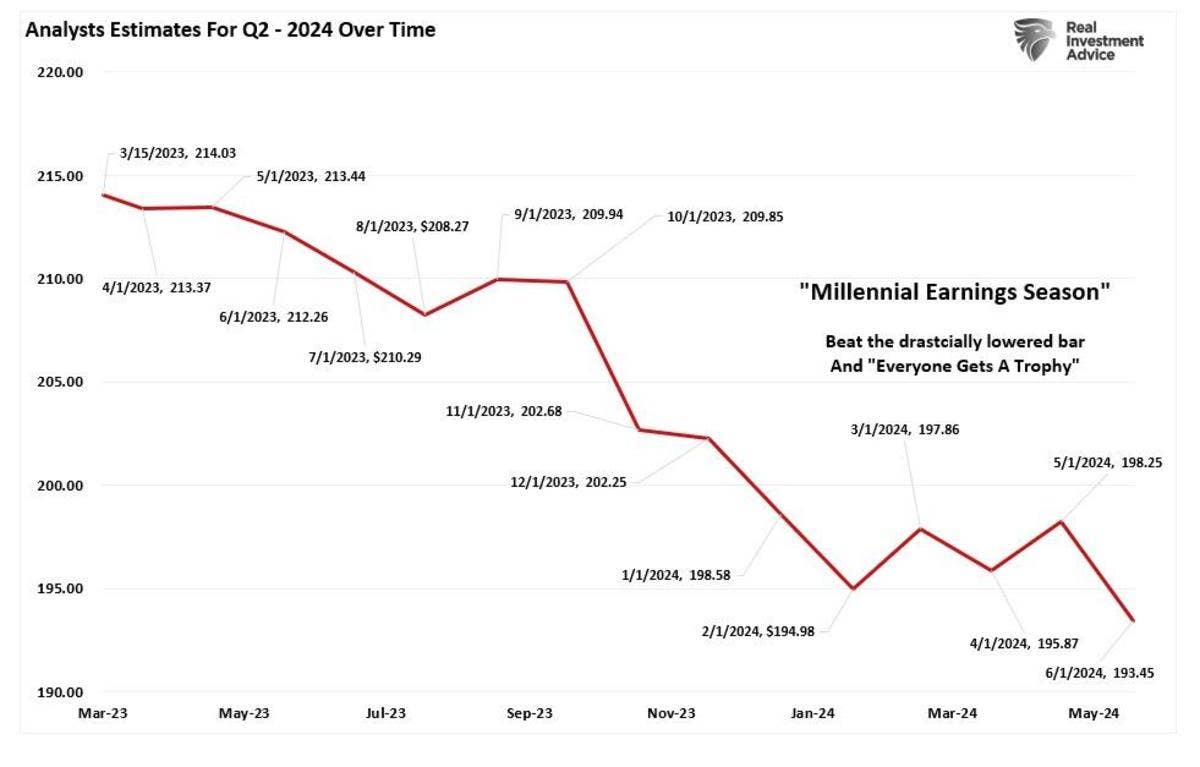

As a reflection of this view, expectations for 2024 have recently fallen by $5/share and for next year consensus profit projections have declined by $9/share:

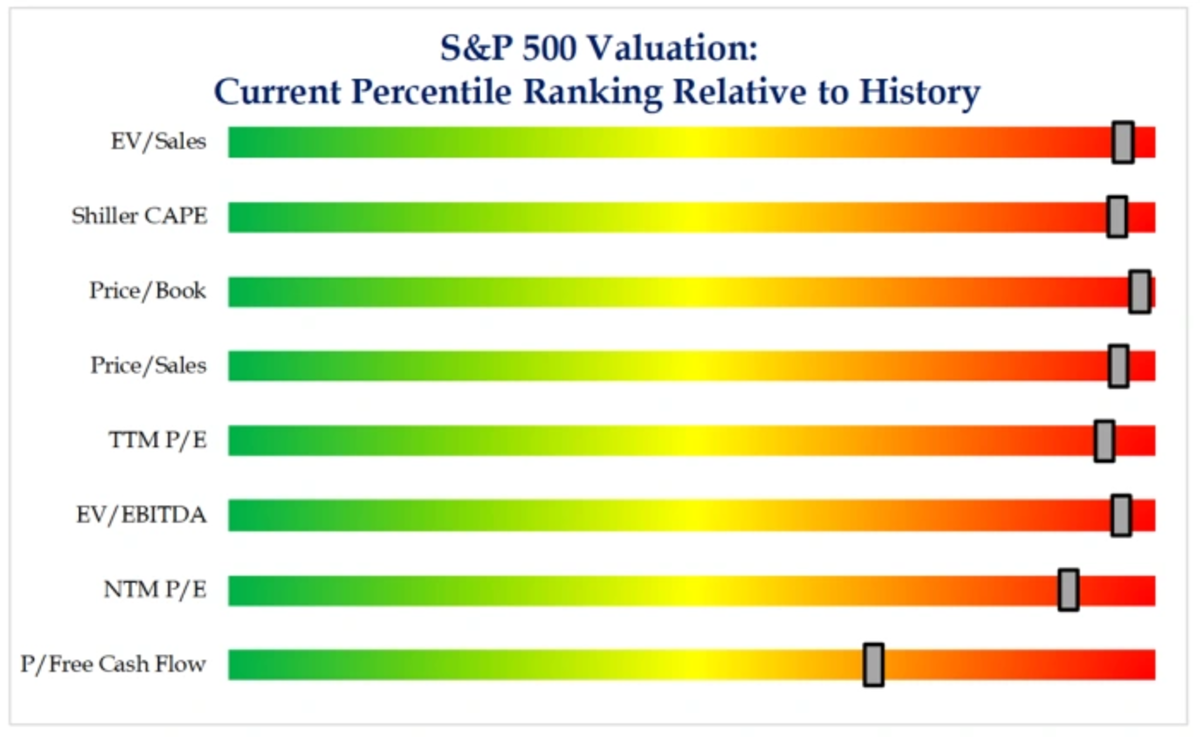

Importantly a too optimistic consensus profits outlook comes at a time in which stocks are overvalued. Most traditional valuation metrics are in the 90%+ tile:

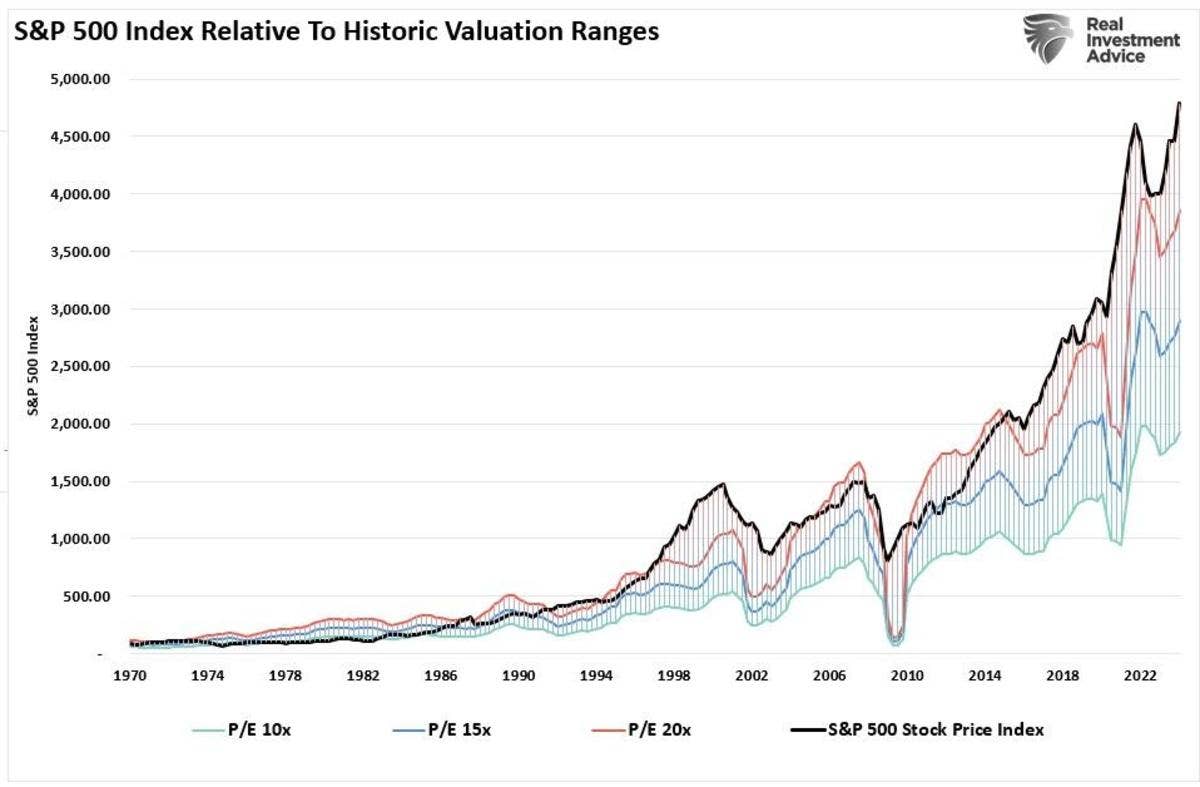

Equity prices generally (and over long period of time) tend to track economic growth and earnings. Over the last 7-8 decades the economy has expanded by a 6.4% growth rate, EPS have compounded by 7.7% annually and stock prices have risen by 9.3%/year.

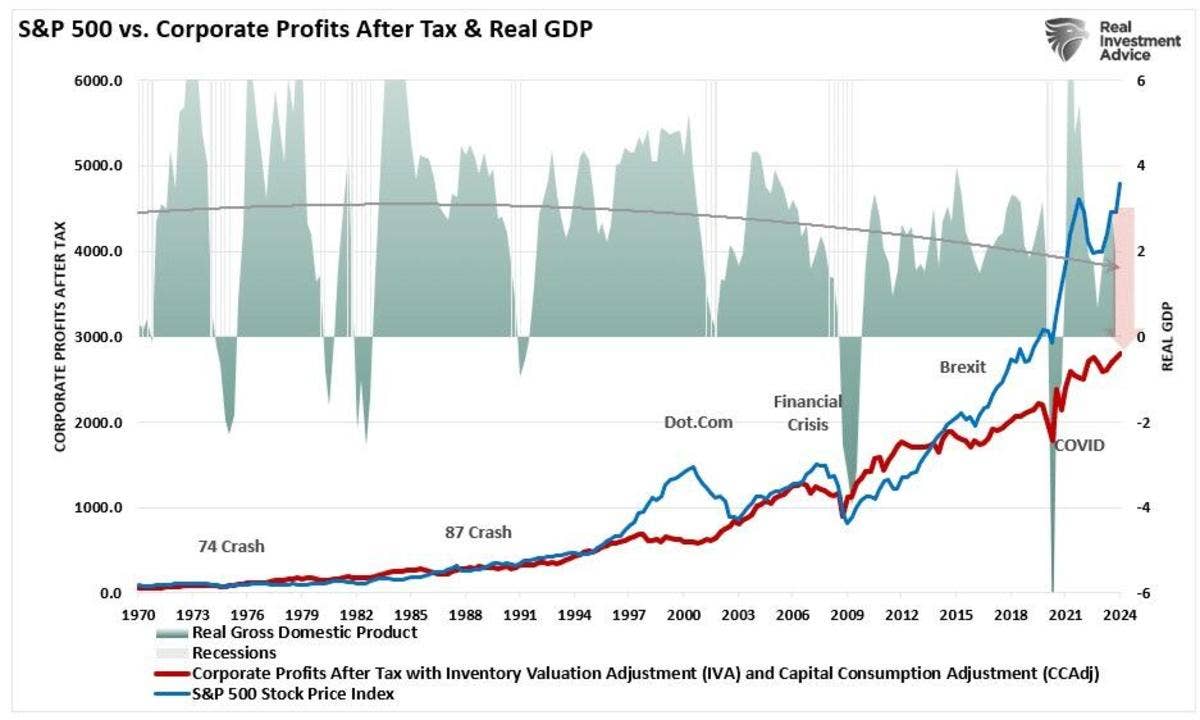

The chart below demonstrates how overvalued equities are relative to Real Domestic Product and after tax profits:

Most strategists are expecting about a 10% rise in S&P profits in 2024 and near 15% again next year.

How is this possible given the following backdrop?

* The economic bounce back from Covid is over. The rate of growth in U.S. GDP is likely moderating toward about +1.5% over the next few quarters.

* Inflation has dropped dramatically to around 2.5%-3.0%. With economic growth decelerating and inventories no longer scarce, companies have likely far less pricing power today than at any point in the last two to three years. The impact of "stacked" or cumulative inflation is already being felt on reported profits by a number of consumer-oriented companies like Home Depot, McDonalds, Starbucks, Winnebago and many others (some of which we are short!).

* Inflation remains prickly – which means the Fed will be less easy and stimulative. Expectations of six rate cuts (as recently as five months ago) has been reduced to one to two cuts for this year.

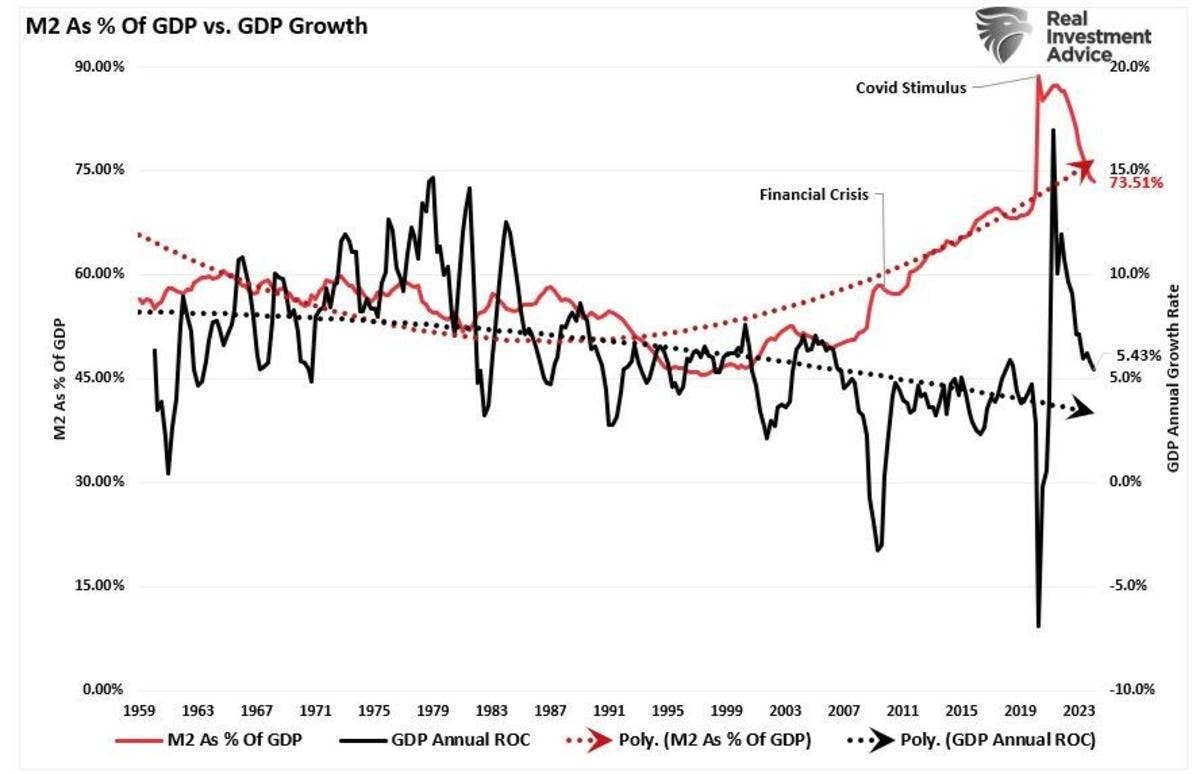

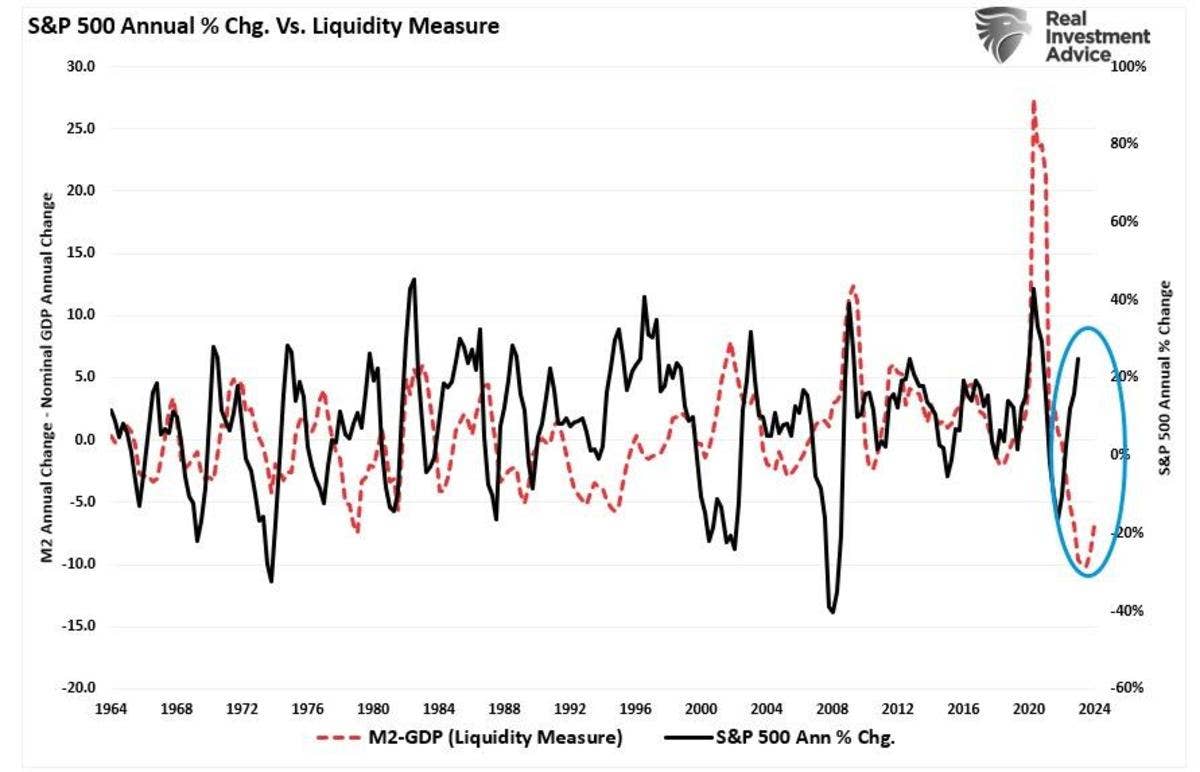

* The surge in liquidity/money supply is over:

While the media often states that “stocks are not the economy,” as noted, economic activity creates corporate revenues and earnings. As such, stocks cannot grow faster than the economy over long periods. A decent correlation exists between the expansion and contraction of M2 less GDP growth (a measure of liquidity excess) and the annual rate of change in the S&P 500 index.

Currently, the deviation seems unsustainable. More notably, the current percentage annual change in the S&P 500 is approaching levels that have preceded a reversal of that growth rate:

So, either the annualized rate of return from the S&P 500 will decline due to repricing the market for lower-than-expected earnings growth rates, or the liquidity measure is about to turn sharply higher.

Other issues:

* Not only won't monetary policy stimulate much growth, but with fiscal policy out of hand, there is a limit to further expansion in fiscal stimulation. It is almost certain that fiscal outlays will not be as stimulative over the next 18 months as in the past several years.

* Though currently ignored by authorities and investors, the U.S. deficit and debt load are out of hand and must be addressed. Former President Trump's tax cuts expire next year. More tax cuts will be inflationary, lowering growth. Should the incumbent prevail, tax increases are likely - this will also dampen economic growth.

* Following the pandemic, consumption has been pulled forward. The consumer has reduced/eliminated excess savings and has taken on loads of debt - the consumer is now spent up not pent up. And, as mentioned previously, cumulative inflation is now taking its toll.

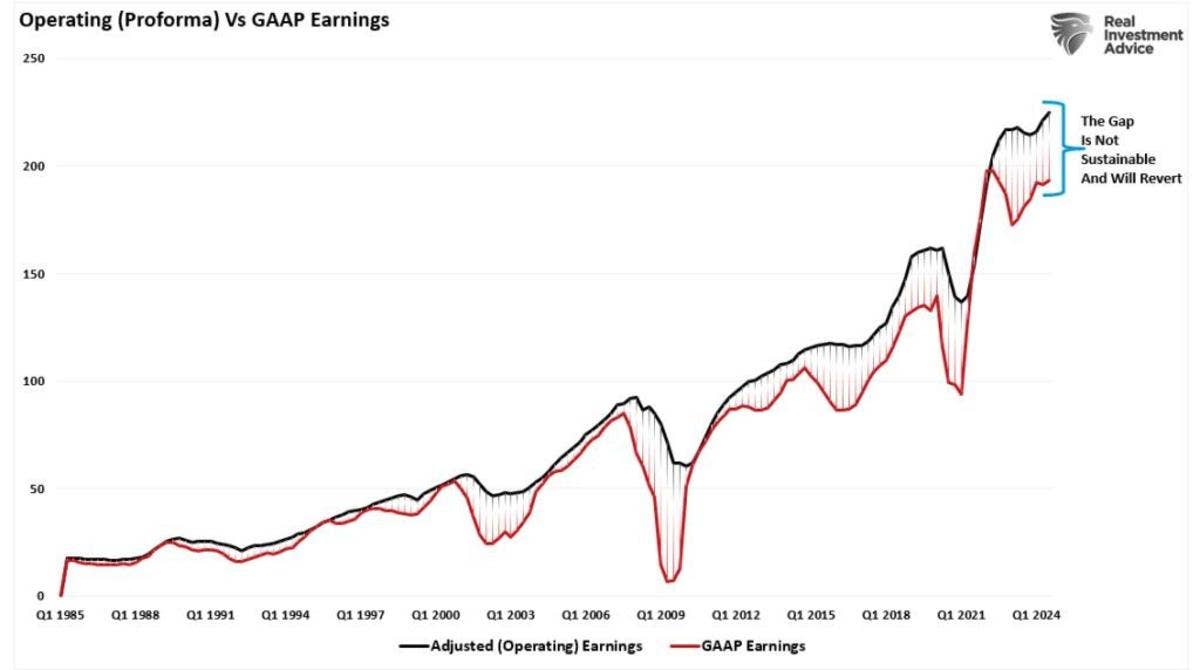

* The quality of earnings remains suspect. Most companies report “operating” earnings, which obfuscate profitability by excluding all the “bad stuff.” A significant divergence exists between operating (or adjusted) and GAAP earnings. When such a wide gap exists, investors should question the “quality” of those earnings:

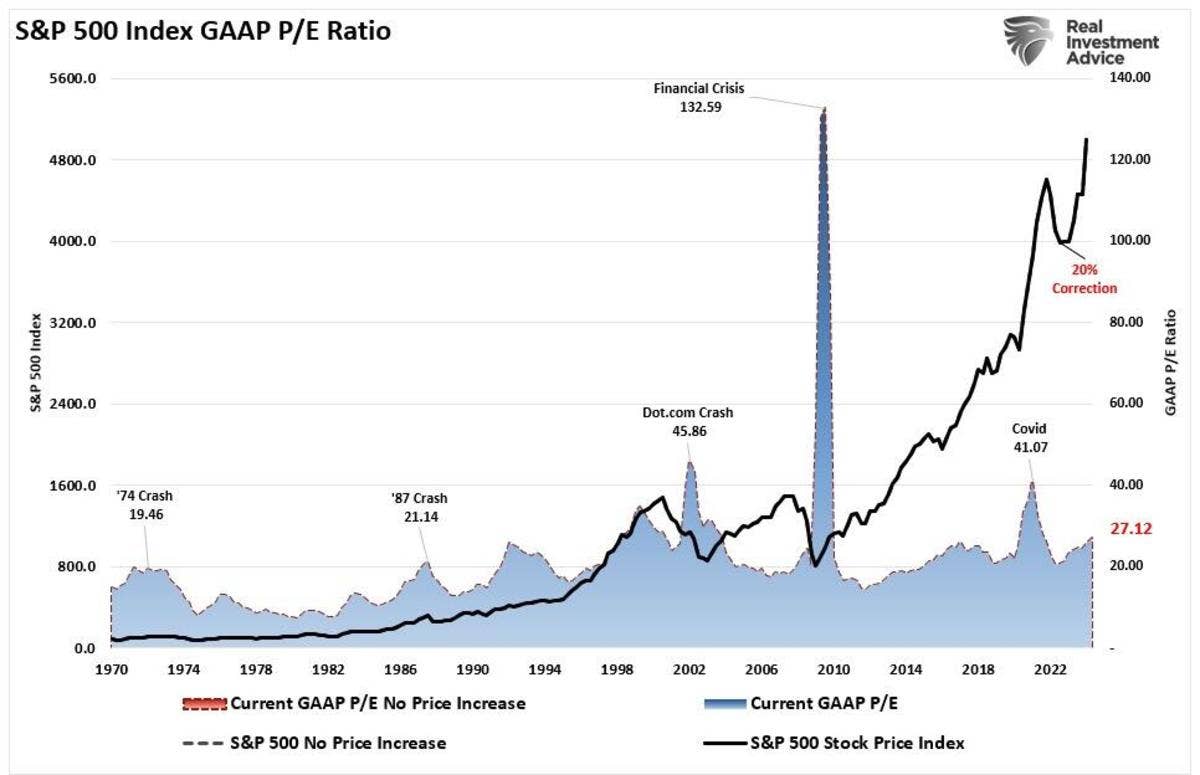

The chart below uses GAAP earnings. If we assume current earnings are correct, then such leaves the market trading above 27-times earnings. (That valuation level remains near previous bull market peak valuations.)

To conclude, I remain a disciplined investor, selecting equities (long and short) through hard-hitting analysis, with a calculator in hand. I refuse to chase equities, particularly when valuations based on historical metrics, are at or above the 90%-tile.I plan to continue to be patient in continuing to pursue a risk-averse strategy (concentrating on a conservative approach thru pairs investing) over the near term.Importantly I fully recognize that wealth is generated by being long equities - but there is a time and place to be defensive. Large cash positions and/or shorting stocks protect wealth as most learned just two years ago.

The bottom line is that we are growing more confident that equities will finally fall back to an area that represents value - perhaps sooner than later.

Representative longs include Trulieve, Green Thumb Industries, Glass House Brands, St. Joe Company, Draftkings, Valvoline, Freshpet, Elanco Animal Health, Walt Disney and Procter & Gamble.

Representative shorts include McDonald’s, Medical Properties Trust, Winnebago, Sleep Number, B. Riley Financial, Freedom Holding Corp, Petco Health and Wellness, Warner Bros. Discovery, Chegg, FIGS, Walgreens, Boot Barn and Blackstone Mortgage Trust.

BY Doug Kass · Jul 23, 2024, 10:17 AM EDT

I have converted my short common in SPY/QQQ to short calls.

BY Doug Kass · Jul 23, 2024, 10:04 AM EDT

From Peter Boockvar:

The smoke signals ahead of BoJ meeting next week/Some earnings comments

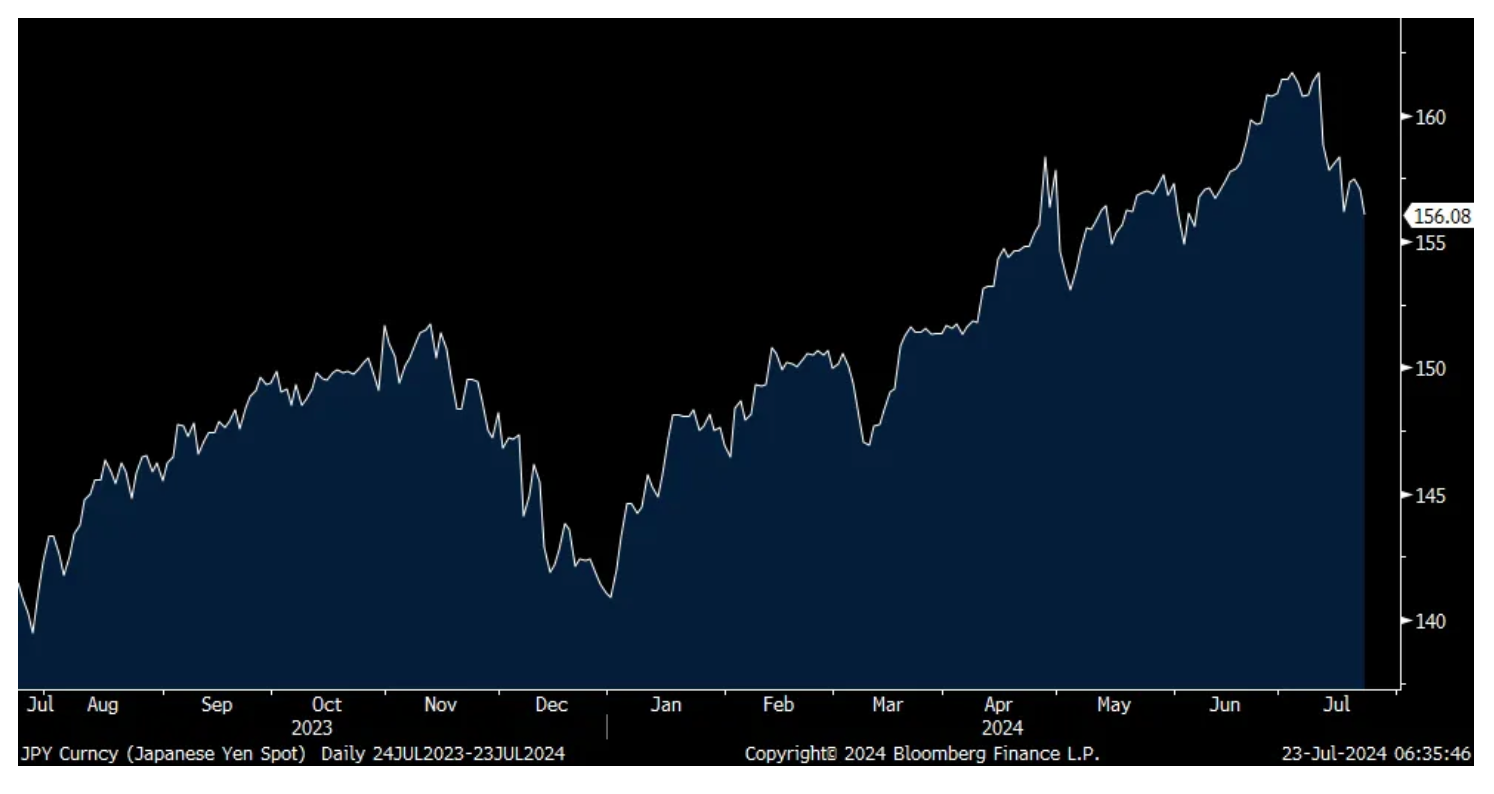

Ahead of the BoJ meeting next week, the leaked and political signals so far are mixed on what they will do. There was a Bloomberg story yesterday that said "Bank of Japan officials see weakness in consumer spending complicating their decision over whether to raise interest rates at a policy next week, according to people familiar with the matter." I'm not sure why they don't realize that it is falling REAL wages that helps to explain that and why they should raise rates to contain inflation that would lift REAL wages.

The article further said "Some officials take the view that skipping a rate hike in July is an option to provide more time to examine incoming data to confirm if consumer spending will pick up as expected, the people said. Some of them hold the position that the BoJ should avoid giving the impression of being overly hawkish, they said." As the BoJ has redefined the word 'patience', I don't think the BoJ would ever get accused of being 'hawkish.'

Regardless of how these BoJ officials feel though, the persistent weakness in the yen has the Japanese government not happy and the yen is rallying to the highest vs the US dollar since early June, notwithstanding the BoJ comments, because of what a ruling party member of the LDP said overnight "Excessive yen declines are clearly negative for Japan's economy." This official wants the BoJ to lay out a plan for a pullback in the easing and said the economy can handle it. "The BoJ needs to clearly communicate that it will firmly proceed with the normalization of monetary policy." The 10 yr JGB yield was up 1 bp to 1.07%.

Yen

NXP Semiconductor is reminding us that outside of selling chips into the AI ecosystem, the semi business remains tough as excessive inventory still is getting absorbed. They lowered guidance and in their earnings release (call is this morning) said "We continue to manage what is in our control enabling NXP to drive resilient profitability and earnings in a challenging demand environment."

Nucor said "While market conditions have softened compared to recent record-setting years, Nucor remains focused on its long term growth strategy." They said the main reason for the earnings drop q/o/q "was the decreased earnings of the steel mills segment, primarily due to lower average selling prices, and, to a lesser extent, decreased volumes."

With respect to all the banks we've heard from, both money center and regional, a consistent them is the lack of loan growth. Truist Financial reiterated that yesterday in their call:

"Average loans decreased .7% on a sequential basis, reflecting overall weaker client demand." And, "we expect client loan demand to remain relatively muted in the third quarter."

Stress in office continues and they did raise their reserve "on this portfolio from 9.3% to 9.7% during the quarter to reflect continued stress in the sector. Approximately 6.3% of our office portfolio is currently classified as non-performing compared with 5.5% at March 31st...We expect stress to remain in the office sector and believe that the size of our portfolio is manageable and well reserved, but our position is to be very proactive in identifying and resolving issues in this portfolio." Elsewhere, they said their asset quality remained stable, "reflecting our strong credit risk culture and proactive approach to quickly resolving problem loans."

Sherwin-Williams, whose paints go on a lot of things, beat eps estimates but missed top line forecasts. They said "Consumer Brands Group sales continued to be impacted by soft North American DIY paint demand. Performance Coatings Group sales were led by growth in Industrial Wood and Coil. Auto Refinish sales increased by low single digits in North America but were offset by softness in Latin America. Packaging sales were down less than expected, and General Industrial demand was soft in all regions." They referred to the overall demand environment as seeing "continued choppiness."

With respect to Coke and Kimberly Clark, a strong dollar clipped revenues by about 500 bps each.

Genuine Parts, a global distributor of automotive and industrial replacement parts, missed numbers and lowered guidance and said:

"Our quarterly results reflect softer than expected market conditions, which are tempering demand particularly in our Industrial and US and European Automotive businesses." They also mentioned the "challenging macro-environment."

GM's numbers look good but their earnings release didn't have any commentary and we await the call.

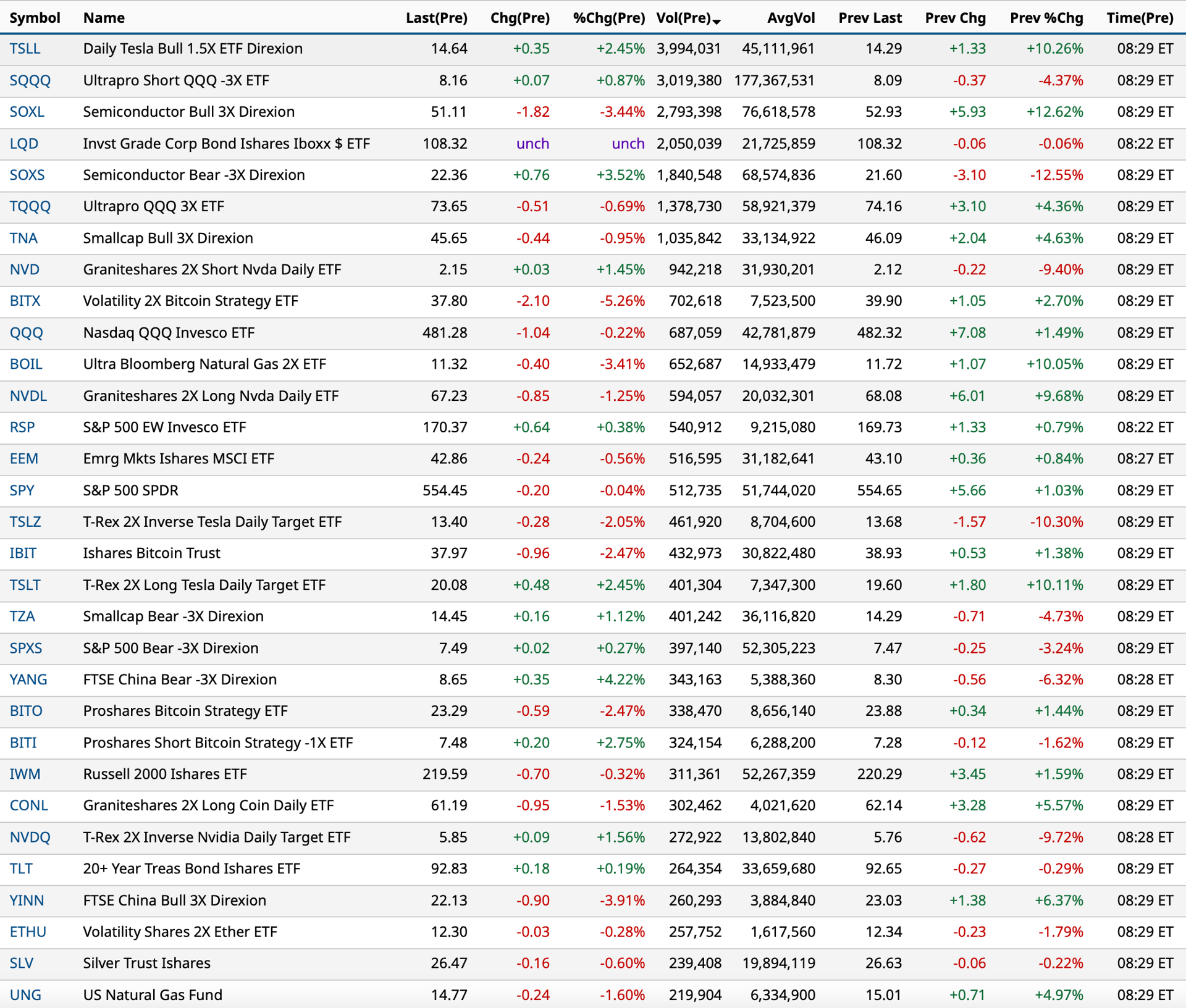

BY Doug Kass · Jul 23, 2024, 9:30 AM EDT

As of 8:29 a.m.:

BY Doug Kass · Jul 23, 2024, 9:12 AM EDT

Upside:

-ADIL +54% (advances to second cohort in Pharmacokinetics study of AD04 for treatment of Alcohol Use Disorder)

-BCAB +14% (granted FDA Fast Track Designation for Ozuriftamab Vedotin (CAB-ROR2-ADC) for Treatment of Patients with Recurrent or Metastatic Squamous Cell Carcinoma of the Head and Neck)

-SPOT +13% (earnings, guidance)

-CCK +7.2% (earnings, guidance)

-DHR +7.2% (earnings, guidance; Board approves additional 20M common share repurchase)

-ICU +6.3% (first pediatric patient treated in a commercial setting with FDA approved QUELIMMUNE Therapeutic Device)

-SAP +6.1% (earnings, guidance)

-SHW +5.8% (earnings, guidance)

-ZIMV +5.8% (announces FDA Clearance and U.S. Launch of GenTek Restorative Components)

-MMYT +5.7% (earnings)

-HCA +5.1% (earnings, guidance)

-WRB +4.6% (earnings)

-SOLV +4.4% (Nelson Peltz (Trian) said to have taken stake)

-ZION +4.1% (earnings, guidance)

-MDAI +4.0% (adds three new clinical trial sites To expedite Emergency Department Patient Enrollment; seeks FDA approval of DeepView System for burn indication in 2025)

-IRDM +3.4% (earnings, guidance)

-GE +3.3% (earnings, guidance)

-GM +2.5% (earnings, guidance)

-NNE +2.3% (files Provisional Patents to secure its Newly Acquired Annular Linear Induction Pump Technology)

-LMT +2.2% (earnings, guidance)

-PM +2.0% (earnings, guidance)

Downside:

-JAGX -67% (reports Phase 3 OnTarget Trial Results for its Cancer Supportive Care Drug Crofelemer)

-CLRB -16% (reports Iopofosine I 131 Waldenstrom’s Macroglobulinemia Pivotal Study results)

-MEDP -13% (earnings, guidance)

-PII -11% (earnings, guidance)

-UPS -10% (earnings, guidance)

-NXPI -8.4% (earnings, guidance)

-PCAR -6.5% (earnings, guidance)

-AROC -4.9% (issues Q2 guidance/prelim results; priced 11M shares at $21.00)

-GPC -3.3% (earnings, guidance)

-CMCSA -3.1% (earnings)

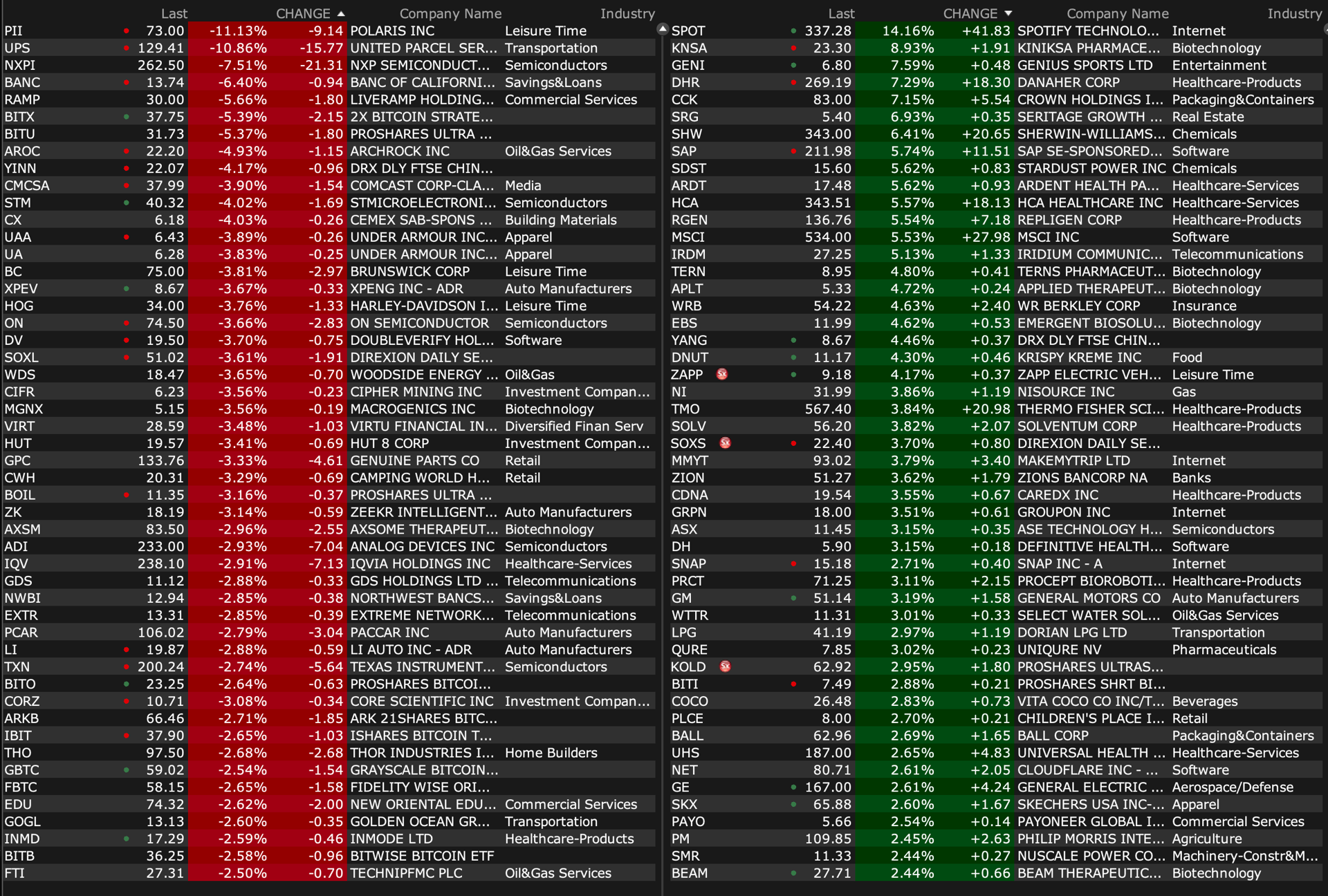

BY Doug Kass · Jul 23, 2024, 9:05 AM EDT

As of 8:29 a.m.:

BY Doug Kass · Jul 23, 2024, 8:58 AM EDT

I am back shorting common shares of the Indices:

* SPY $555.21

* QQQ $482.32

BY Doug Kass · Jul 23, 2024, 8:27 AM EDT

From JPMorgan:

Maintains neutral on D.R. Horton DHI (I have been shorting) with a price target of $180.

BY Doug Kass · Jul 23, 2024, 8:00 AM EDT

From Danielle DiMartino Booth:

Ways of brewing your morning cup of Joe have morphed over time, some with more of a jolt than others. As with every great story, there’s always a touch of irony. In this case, that manifested as Keurig being founded in 1992 as a company targeting the office coffee market. But it was the 1998 advent of the K-Cup pod that changed things forever in the home. Single-serve coffee brewing personalized caffeine consumption. Not every invention is perfect. Take it from QI’s Dr. Gates who was struck by an oddly iridescent green on display on the inside walls of his Keurig’s water reservoir. In the event you’re ever in the same situation, use the Vinegar Method following this five-step process. 1) Fill the reservoir halfway with distilled white vinegar, and the other half with hot water; 2) Stir the mixture and let the solution sit for 30 minutes; 3) Flush through the solution with the brew function; 4) Repeat these steps two-to-three times; 5) Run fresh water through the brew cycle.

To be sure, algae is not the sort of ‘green shoot’ that garner the attention of dismal scientists. The U.S. capital expenditure (capex) cycle has technically been in green shoot mode since the economy was reopened after being forcibly shut four years ago. Stepping back, inflation-adjusted business fixed investment has expanded with little interruption for 14 of the 15 quarters since 2020’s third quarter (yellow bars). The streak is likely to be extended when second-quarter gross domestic product (GDP) is released on Thursday.

This said, the long-established Philadelphia Federal Reserve’s manufacturing survey flagged a reversal in July. The headline slipped to 7.4 from the second quarter’s average of 17.4 (teal line). Relative to the long-run average of 18.4, July’s z-score of -1 was also below normal. Validation arrived via the Seventh Fed District. The Chicago Fed Survey of Economic Conditions (CFSEC) Future Capex index fell to -36.4 in July (lilac line). While this wasn’t a record monthly low since the series’ 2013 inception, it was a post-pandemic low, taking out May’s -36.2 reading. Should the weakness hold, it would take out 2020’s first-quarter average of -33.1.

The CFSEC also issued a warning of sorts on today’s S&P Global’s flash manufacturing and services sector surveys. From May’s green shoot of 3.1, June notably fell back to -22.8; July’s -21.9 did nothing to improve the data’s tone (red line). Given the re-weakening in the auto sector, forecasters’ expectation that June’s level of 51.6 will be maintained at 51.7 in July may prove to be overly optimistic (blue line). As for the broader services sector, there’s only been one month in the last 27 that CFSEC’s Non-manufacturing Activity index has poked into positive territory (yellow line). Notably, it once closely tracks S&P’s Global Services headline PMI. A break in the co-trend that occurred early last year, however, has remained in place (green line). While economists foresee expansion stretching into July, it’s critical to frame this series in the context of industries it doesn’t capture -- mining, construction, wholesale trade and retail trade.

A loosening labor picture would ratify the coolness in business activity. We see no coincidence in July CFSEC Current Hiring tumbling to a five-month low of -27.9. Moreover, Hiring Expectations remained negative at -13.6 for a 26th straight month while Current Labor Costs were below average, at -16.3, for the 14th month in the last 15.

The Chicago Fed National Activity Index (CFNAI) corroborated the CFSEC. The CFNAI’s Labor Indicators, which gauge the nationwide trend in employment, unemployment and hours have reached a critical juncture. Four straight subzero quarters (inverted green bars) qualify as a recession signal given streaks of such persistence were a feature of every pre-pandemic recession since 1970. As for how mildly underwater the readings have been, persistence matters more than the magnitude when determining labor cycle vulnerability.

Speaking of the labor cycle, last Friday’s June state employment and unemployment report via the Bureau of Labor Statistics (BLS) allowed for QI’s second quarterly analysis of the parallel McKelvey and Sahm Rules for the unemployment rate. June state unemployment figures did nothing to change the conclusion that both rules are at critical breadth levels in the second quarter – 61% for McKelvey and 38% for Sahm, both of which are recessionary.

The state of Illinois is playing its part. According to the Illinois Department of Employment Security, the Land of Lincoln’s unemployment rate ticked up to 5.0% last month from May’s 4.9%. In all, the state’s unemployed number 327,900, is up 18.7% year-over-year. You’ll note that this is appreciably higher than the 4.1% for the nation as a whole. That said, there are states that are worse off. Per the BLS, at 5.4%, the District of Columbia had the highest unemployment rate followed by California and Nevada, both of which sport a rate of 5.2%.

As for Keurig, since reinventing how coffee is consumed, it’s met with increased competition from others in the space including Nespresso, which has garnered its own cult-like following. Last week, the residents of Windsor, Virginia received news the Keurig Green Mountain facility would permanently close by the end of 2024, leaving 379 without jobs. In operation since 2012, it was the area’s third-largest machinery and tools taxpayer behind International Paper and Smithfield Foods, two other manufacturers that have recently made national news announcing their own downsizings. Powell is at increased risk of losing his race against time.

BY Doug Kass · Jul 23, 2024, 7:50 AM EDT

The S&P Short Range Oscillator remains ovebought at 5.86%.

The Oscillator reached "peak overbought" recently on July 15 at 8.28%.

BY Doug Kass · Jul 23, 2024, 7:30 AM EDT

BY Doug Kass · Jul 23, 2024, 6:45 AM EDT

Some observations from me:

* Not surprisingly as stocks have climbed, opinions (technical) have grown ever more optimistic and confident (even filled with hubris).

* Thus far this has been justified but the cheekiness should concern all.

* As I have written, ten cuidado!

“The one thing that never seems to change is human nature. Science changes, art changes, cities change, governments change, but human nature remains relatively constant."

- Richard Russell

Bonus — Here are some great links:

BY Doug Kass · Jul 23, 2024, 6:31 AM EDT

BY Doug Kass · Jul 23, 2024, 5:59 AM EDT